THE LAST meaningful monetary policy meeting overseen by outgoing European Central Bank (ECB) President Mario Draghi was not without controversy. Indeed, Draghi seldom disappoints. And once more he delivered an aggressive package of measures designed to achieve the ECB’s price stability target—including a number of fascinating policy innovations. Yet somehow this package is more than simply another set of innovations. This set of measures instead represents Draghi’s last stand—an attempt by the outgoing President to secure his legacy by casting a spell over monetary policy into the distant future, creating new policy tools while tying the hands of successor Governing Council members and his successor.

What was announced?

First, a reduction in deposit rate by 10bps to -50bps—alongside tiering of interest applied to bank deposits with the Eurosystem. As a result of the new two-tier system, up to six times the value of deposits in excess of require reserves will be exempted from the negative deposit rate—while any remaining surplus above this will be charged 50bps. Crucially, the 0% “remuneration rate of the exempt tier and the multiplier can be changed over time,” meaning the quantum and interest rate on this tier are subject to review. Crucially, this was not mechanically tied to the Main Repurchase Operations (MRO) rate—currently also 0%. Rather, it is a distinct—therefore new—Tiered Reserves Rate (TRR). In effect, the ECB created a new interest rate on a variable tier of banking system reserves—and therefore a new policy tool.

Second, recalibration of the third series of Targeted Long Term Repurchase Operations (TLTRO3)—due to be initiated this month—such that the 10bps premium over the main repo rate has been eliminated, the maturity extended from 2- to 3-years, while the interest rate charged could now fall as low as -50bps if bank lending targets are met.

Third, the reintroduction of the Asset Purchase Program (APP) at EUR20 billion per month for an open-ended period—that is, until stringent conditions on inflation are met. In particular, APP will “end shortly before we start raising the key ECB interest rates.” As for these rates they are expected “to remain at their present or lower levels until we have seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within our projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.” In other words, roughly speaking, APP will continue until core inflation reaches near 2% for a sustained period of time.

How can we assess this package of measures?

Let’s start by recalling the previous policy stance and liquidity constellation, before contemplating the impact of the lower deposit rate and the two-tier system. What follows is my understanding—I welcome corrections or clarifications.

Something of a caricature, until Thursday last, the Eurosystem operated roughly as follows. There were two key sources of liquidity—TLTRO2s and past APP purchases. TLTRO2s are negative yielding assets, in that banks would receive the deposit rate of minus 40bps on these if they met lending targets—and roughly 90% of banks reached their lending targets, so de facto these assets tax the system 36bps per year. Against this, excess liquidity across the system—created by both TLTROs and APP purchases—is charged the deposit rate, meaning above reserve requirements banks are essentially taxed to pay TLTROs and create income for the Eurosystem.

With the exception of the coupon on Public Sector Purchase Program (PSPP) holdings—which could soon generate negative income, if not already in some cases—the monetary income across the system is pooled. So whatever is made through the using TLTRO2s and excess liquidity is shared according to capital key.

The distribution of excess liquidity, TLTRO, and APP purchases is shown in Figure 1 below, using data on disaggregated National Central Bank (NCB) balance sheets as of early-August.

Given we can ignore PSPP coupons, which are returned to the local NCB, we can have a go at calculating the income and outgoings from the policy stance prior to Thursday, and how this will change.

An important caveat is necessary at this point. We cannot back out the sharing of coupons from the various other components of the APP—such as Covered Bond Purchase Program (CBPP), supranationals, etc., as well as outstanding coupons from prior programs such as the Securities Market Program (SMP) etc. So we ignore this flow, which could be important and will depend on the distribution of purchases, including by the ECB itself, on behalf of the Eurosystem. In addition, the precise country-level TLTRO interest cannot be known based on information available, so we assume the lending targets were met equally across countries at 91¼% (see March, 2019).

With this, we narrow in only on the monetary income from TLTROs and excess liquidity alone. In Figure 2 (left side), income due to the negative deposit rate by country or group of countries is shown. In the aggregate, on these monetary policy-related operations, the Eurosystem makes a profit of about EUR4.6 billion. Germany makes income of about EUR2 billion on behalf of the system, while Italy makes negative net income of about EUR0.4 billion. But German profit is only EUR1.2 billion, Italian is EUR0.8 billion.

While Germany, France and other Core countries make some income from what will become “tiered liquidity”—separated out here—Italy and Spain make all of their positive income from this classification of liabilities. Their excess liquidity is below the ceiling of six times required reserves.

However, due to the sharing of monetary income across the system, some of the income from excess liquidity in the core is de facto transferred from the Core to the Periphery. Recall, aggregate monetary income is shared by capital key. The income due to the sharing of monetary income is shown as “profit sharing” in the chart; de facto transfers are identified as “profit sharing.”

Indeed, income generated through the implicit tax on the banking systems of France (EUR0.7 billion) and Germany (EUR0.8 billion) and other Core countries such as Luxembourg is in effect transferred to the banks of other Periphery members such as Spain (EUR0.8 billion) and Italy (EUR1.4 billion) and others.

Take the Banca d’Italia (BdI). While they would make a loss on monetary income due to transactions with domestic banks for monetary policy purposes, in fact they will still make a profit of about EUR0.8 billion. This is possible because they receive about EUR1.4 billion in transfers from the rest of the Eurosystem. This covers their “profit” from system-wide monetary policy as well as funding necessary transfers to the Italian banking system of EUR0.6 billion on roughly 36bps TLTRO2 outstanding net of excess liquidity taxed at 40bps.

In other words, until Thursday Core banks were making transfers to those in the Periphery. But NCBs were making positive monetary income, notwithstanding these concealed transfers.

What is the impact of Thursday’s policy announcement? Let’s assume TLTRO2s are rolled over in full into TLTRO3s, and that bank lending targets are met 100%. And let’s assume the current distribution of liquidity is unchanged (i.e., don’t contemplate additional APP purchases for now, or capital flows within the system.) Then the impact on income and transfers across the Eurosystem is shown on the right side of Figure 2. With tiering of six times required reserves—set at 0%–there is no longer any income from this source. Moreover, the cost of TLTROs has increased as the deposit rate has been reduced to minus 50bps.

Crucially, the main impact if that the overall profit in the system is reduced EUR2.7 billion, from EUR4.6 billion to EUR1.9 billion. As such, the resources available for NCB profits, other things equal, is reduced.

Moreover, curiously, the size of the transfers from creditor to debtor within the Eurosystem actually increases. Why? Because Spain and Italy now don’t generate any income on excess liquidity, in fact they need to receive larger transfers from the system in the context of sharing monetary income to fund the payments to their banks from TLTRO3 as well as zero income on excess reserves.

Indeed, Figure 3 shows how Thursday’s announcement, other things equal, benefits banks by country and impacts intra-system transfers relative to the baseline. Banks in Germany benefit about EUR650 million (per year) while Bundesbank profits decrease about EUR700 million. The difference is larger transfers to the system as a whole as additional transfers, mainly from France, are needed to Italy and Spain.

Perhaps the most important point to note here is that the new policy measures mainly act to reduce NCB monetary income. Given many NCBs will soon—if not already—face negative income on holdings and rollover of PSPP portfolios, which will be a drag on profits, this further threatens income and capital in the future.

Perhaps the most important point to note here is that the new policy measures mainly act to reduce NCB monetary income. Given many NCBs will soon—if not already—face negative income on holdings and rollover of PSPP portfolios, which will be a drag on profits, this further threatens income and capital in the future.

In other words, the policy change has served to transfer income from Eurosystem income to the banking system.

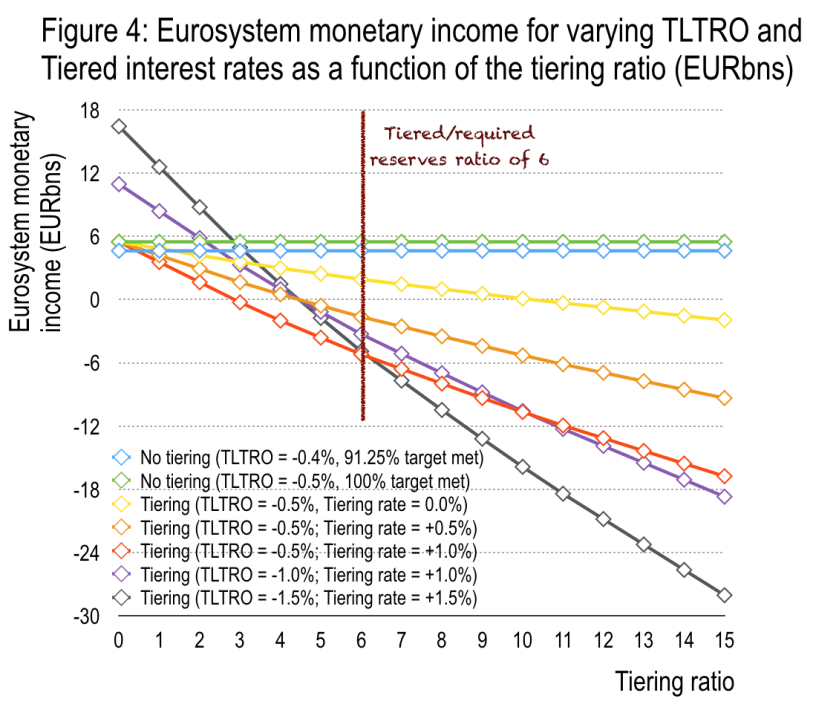

And most important, since the interest rate on tiering is distinct from the MRO rate, this can be increased in the future to create additional income for banks at the expense of NCB capital—to improve profitability and, hopefully, increase net lending in pursuit of the inflation target. To this end, Figure 4 below provides a number of scenarios, calculating the monetary income for the aggregate Eurosystem as a function of the tiering ratio—starting from 0, i.e., no tiering, to 15, though chosen at 6 last Thursday.

(As an aside, it seems clear why the initial tiering ratio of 6 was chosen. In my model, this generates savings to banks of EUR3.6 billion, which is almost exactly the same as the rollover of EUR693 billion of TLTROs at -50bps.)

While the current system, without tiering, generates income for the Eurosystem, tiering creates the possibility that the system as a whole receives negative income from monetary policy actions. For example, with a deposit rate of -50bps and tiering rate of +50bps, then a tiering ratio above 10, there would be negative income for the Eurosystem as a whole. In other words, monetary policy would require NCBs to run down capital to transfer to the banking system to encourage lending and meet the inflation target.

(We ought note there are other, non-monetary sources of income—as well as possible coupons on APP purchases. But the trend towards running down NCB capital in pursuit of monetary stability is clear.)

More realistically, at the existing tiering ratio of 6, a TRR of +100bps with deposit rate unchanged would generate negative income for the Eurosystem of about EUR5 billion per year.

For this case, Figure 5 illustrates the impact on income and transfers across the Eurosystem given the existing distribution of liquidity. Since the system as a whole makes a loss, it is this loss which is now shared across the Eurosystem. However, peripheral banks are still in receipt of income due to both TLTRO3s and that due to tiered reserves. As a result, some of the income on non-tiered reserves from the Core is transferred to the Periphery still—Core banks are still subsidizing their Periphery counterparts.

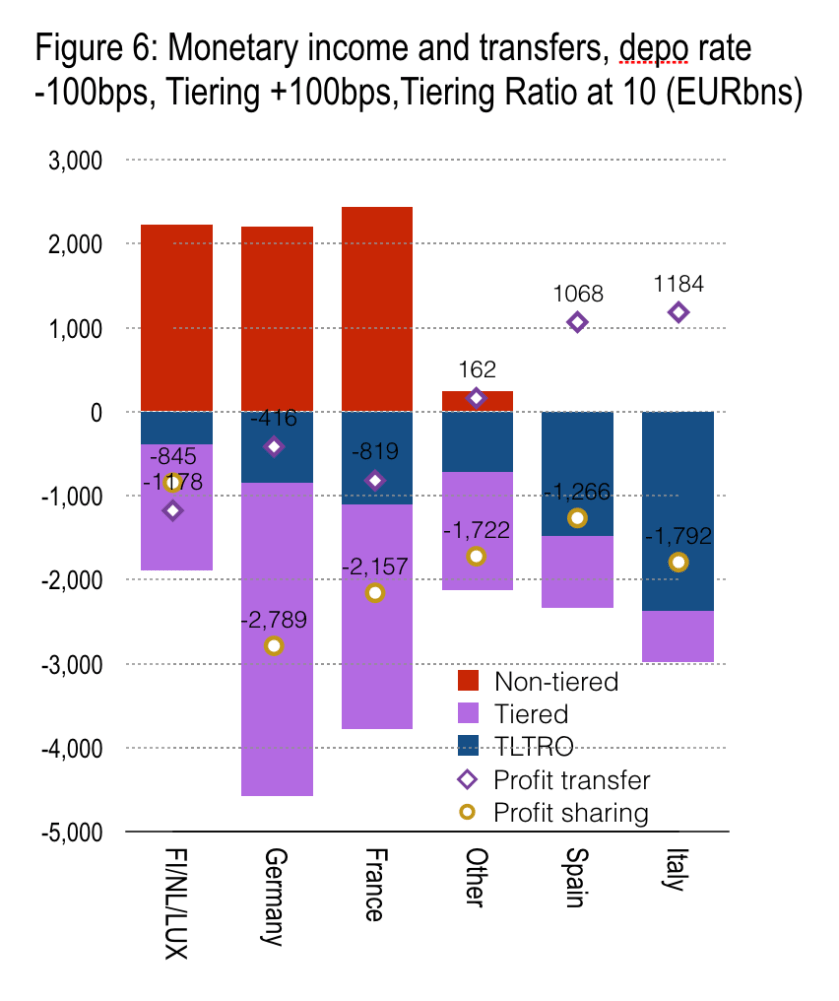

Meanwhile, there are more extreme outcomes, of course. See Figure 6. Imagine the deposit rate at -100bps with TRR at +100bps. And suppose the Tiering Ratio is increased to 10 times required reserves, with existing liquidity distribution. Then we are again in a world where NCBs make losses on monetary income. But here, for Core central banks, this negative income goes to pay domestic banks for their use of the Tiered Reserves as well as transfer to Peripheral banks for the same purposes. Thus, NCBs are running down their capital to provide income for the domestic banking system—and in the case of the Bundesbank subsidize peripheral central banks’ income and banking systems.

Of course, none of the above reflects on the possibility of a growing balance sheet of the Eurosystem as a whole, or indeed the future distribution of reserves—and TARGET2 balances. Even with TLTRO rollover and repayment on schedule, and with currency in circulation growing at nearly 5% per year, APP purchases of EUR20 billion per month would drive excess liquidity near EUR2.8 trillion by end-2030 (that is, EUR1 trillion above today’s levels.) The distribution of this liquidity, and associated TARGET2 balances, will become increasingly important in determining the relative transfers between NCBs and the overall income of the system.

Should core inflation continue to fall short of target, this raises the concern that open-ended APP with possible increases in the TRR will create losses for NCBs—eroding capital in pursuit of price stability.

Thus the creation of a new interest rate—the TRR—alongside potentially open-ended APP generates many more possibilities for sharing of income or the erosion of NCB capital.

That Draghi laid down such stringent conditions for the withdrawal of exceptional monetary policy measures last week suggests he is tying the hands of his successors—to make sure they cannot back down from the pursuit of price stability. Doing so, he is not only suggesting to fiscal policymakers it’s time to take up the burden of macroeconomic management—but without this there will be quasi-fiscal losses through NCBs, as well as growing quasi-fiscal transfers across the system. Better to make these fiscal measures explicit and generous than feeble and hidden.

And central bank governors hate making losses. They are political beasts, many with political ambitions. To be reporting losses year-in-year out, and to be seem as part of a hidden transfer union will be uncomfortable for many—or most.

The fact that, by re-weighted capital key, at least 55.8% of central bank Governors were in some way opposed to the announcement last week (Germany, France, Austria, Netherlands, and Estonia) is suggestive. Add to this two members of the Executive Board, and there is a considerable faction against Draghi’s latest policy wheeze. Is it the open-endedness of proposed APP that matters? Or the new TRR that could generate losses for NCBs in the future? Or the combination of the two? Not clear.

In summary, understanding the quasi-fiscal flows throughout the Eurosystem and the available future policy tools just got much more difficult—and interesting. Bring it on.

END.

This is very helpful, GT.

Sorry if I am overlooking something obvious, but I noticed the estimated cost to the ECB and the estimated benefit to the banks is not identical. In opportunity cost terms, at least, they ought to be, I think? Or is there some passthrough issue I missed?

Whatever the case, the figures you calculate sure are small. I see one of your peers claiming that this innovation bursts the constraints on monetary policy. I doubt that.

As you point out, the source of the transfer is system profits, not “money.” And if this were to become large enough to have macroeconomic significance on the basis of the *scale* of the transfer, then it would presumably run into great political resistance.

So this deals with an adverse side effect of negative rates. It is not transmogrifying.

But that quibble is not with yourself. And, FWIW, I share your view that this was an impressive package. It’s just that Draghi was mostly clearly, rather than obfuscatory, on how.

Great piece!

LikeLike

Thanks GM. In fact, perhaps not clear from the charts, but the total “cost” to the banks is equal to the total “monetary income” to the Eurosystem. For example, in the baseline, the total monetary income for the Eurosystem is EUR4.6bn (i.e., cost to the banks) and this is exactly the profit that is shared across the system. Perhaps the charts don’t reveal this.

The numbers in terms of monetary income are small, i agree. However, the impact on the balance of payments from the combination of negative cost of funding and portfolio adjustment for the periphery can be important. For example, while Italian banks are now subsidised to “lend” to the private sector, so have cheap access to euros, this together with APP has created cheap funding for the Italian private sector to improve the primary income balance on currency account. Indeed, since July 2015 Italy’s primary income balance moved from -EUR0.4bn to +EUR1.4bn. This improvement has come about both because of PSPP purchases of BTPs from non-residents as well as purchases from residents that facilitated a portfolio outflow and income from abroad. And this is all being funded at a negative interest rate. So the actual impact on the balance of payments (about 1/4 of Italy’s current account surplus is now due to a positive primary income balance) is greater than these numbers imply.

Of course, if the “scale” of any quasi-fiscal transfers grew large, this would indeed become a political issue. But it’s now a game of chicken between the ECB and fiscal authorities. “If you don’t spend, we will. And it will come back to haunt you by eroding the profitability of NCBs.” We are a long way off, but we are slowly moving in this direction.

Get back on twitter.

LikeLiked by 1 person