To give President Lagarde substantial credit, since her “close the spreads” gaff on March 12th she has acted aggressively and proactively to support euroarea asset prices while working to persuade fiscal policymakers of the urgent need to find a unified response to a common shock. The Franco-German Recovery Fund proposal initiated the hopes for an ambitious EU budget, including a borrowing instrument, reflected in the Commission’s proposal last week. And today Lagarde hit the monetary sweet spot with a policy announcement that both supported peripheral assets and—in a nod to improved euro area prospects more generally—helped push the euro higher.

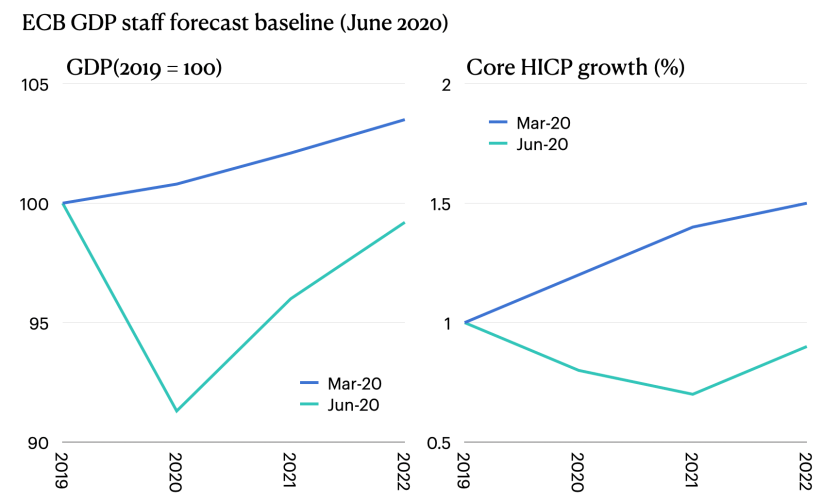

The central message from today’s meeting can be found in ECB staff revised forecasts. To be precise, these were joint forecast by the Eurosystem and ECB staff, who now predict a post-COVID recovery which leaves the level of real GDP by 2022 substantially below that expected in March and still below the 2019 level. There will be a recovery, but this will be far from v shaped.

Today’s forecast implies GDP in 2022 will be 4.2% below the March baseline. If you thought the output gap was closed by 2022 previously (a dubious hope) then the ECB today is telling us there will be a 4.2% output gap still by 2022—a chunky under-utilization of resources. This will mechanically feed into lower inflation under most reasonable macro models, which indeed feeds into lower headline and core inflation in the ECB’s revised staff forecasts. In fact, Core HICP inflation (i.e., ex. food and energy) is revised down by more than headline alone, to print at 0.9% in 2022. At less than 1%, clearly the ECB’s price stability mandate is compromised.

Setting aside discussion of what inflation dynamics might look like given the structural changes that might result in a post-COVID world, and the impact on the capital stock and potential of lower investment, this is straight out a standard Phillips Curve playbook—a higher output gap equals lower price pressure.

This is all rather convenient, of course, when under the spotlight for deviating from proportionality in the pursuit of price stability.

These forecasts therefore provided the pre-text for a renewed policy response to COVID-19. The ECB’s Pandemic Emergency Purchase Program (PEPP) was expanded by EUR600bn (to EUR1,350bn total) through at least mid-2021 with principal reinvestment through end-2022. Temporary principal reinvestment is smart. It keeps the program “temporary” in light of COVID, while preventing NCBs from gaming the program by purchasing in excess short-term maturities to see them roll off ASAP. (See Bundesbank’s weighted average maturity of purchases so far.)

Beyond this, the press conference delivered little new information. Lagarde has resorted to reading from prepared scripts when tricky questions arrive—meaning you get the question she wants to answer, not the question you ask.

However, regarding the German Constitutional Court ruling, we might have broken some new ground. Lagarde explained that the ECB is subject to ECJ jurisdiction. PSPP has been judged by ECJ as in line with their policy mandate. The GCC judgment is directed at German institutions, not the ECB. In any case, the Governing Council regularly assess effectiveness, efficiency, and cost-benefit of policy measures; this has been reflected in ECB monetary policy minutes in the past and will be today and again in the future.

What’s new here is the fact that Lagarde is strongly suggesting that “proportionality” has been routinely and systematically dealt with through the published minutes—the monetary policy accounts. And, by way of convenient coincident or remarkable foresight, these minutes were first published in February 2015—at the exact meeting that APP/PSPP was initiated.

This raises the question: can any meaningful assessment of proportionality be found in the minutes from that time?

The discussion in early-2015 revolved around a sluggish recovery from the Crisis, a neutral fiscal stance looking ahead, weak but improving credit dynamics, and the danger of low inflation settling in through “second round effects” in light of the sharp fall in oil prices in 2014. Indeed, “the time had now come to reassess … whether an expanded asset purchase programme had become necessary to fulfil the ECB’s price stability mandate.”

The discussion of program design involved the following:

- Credit quality. Whether to buy only highest quality credit, or a broader range of investment grade issuers (AAA to BBB) in proportion to capital key. However, “on the basis of ECB staff analysis and the work carried out by Eurosystem committees, the first option was considered to be less effective in the current environment.” At the Governing Council discussion, “limit[ing] the purchases to … the highest credit ratings, was generally regarded as being insufficiently effective.” Absent access to background work, no cost-benefit analysis can be discerned. While “effectiveness” does not preclude overstepping proportionality the ESM was up and running by then, so where is the line in the sand?

- Risk sharing. Whether to share risk in full or only on part of the portfolio. It was noted without elaboration there were trade-offs involved, but “taking into account the unique institutional structure of the euro area with a single currency co-existing with 19 national fiscal and economic policies,” only partial risk sharing might be agreed. This indeed acknowledges institutional constraints, but not proportionality in the context of EU responsibilities, but national prerogatives. In any case, in the deliberation between policymakers, it was agreed that “a regime of partial loss sharing would be more commensurate with the current architecture of Economic and Monetary Union and the Treaties under which the ECB operates.”

- Primary market purchases. A blackout period on purchasing new issues was introduced “to preserve the distinction between the primary and the secondary markets… [also] applied for the neighbouring securities along the yield curve… in line with earlier practice to ensure compliance with the monetary financing prohibition laid down in the Treaty.”

- Market functioning. For purchases “an issue share limit… [at 25%] would be to preclude the possibility of the Eurosystem obtaining a blocking minority in a debt restructuring involving collective action.” Meanwhile the Eurosystem would “accept the same treatment as private creditors, which was a ‘pari passu’ treatment… [so as not to] disrupt the normal functioning of the market by obtaining seniority vis-à-vis private investors.”

- Price formation. In addition, there would be a limit of “33% of an issuer’s outstanding securities… to safeguard the normal price formation mechanism in the market, as the Eurosystem did not want to crowd out private investors.”

- Moral hazard. Concern that monetary policy action could slow policy action elsewhere, including “weaken[ing] their incentives for structural reforms and fiscal consolidation.” Thus, other policymakers were called upon to act appropriately. “These were strong messages to be conveyed to euro area governments and the European Commission.”

This is only a partial review of the ECB’s policy deliberations from 2015 at PSPP inception. In any case, it is not for me to judge. But can the above be considered a complete proportionality review, taking account of the full range of actors across the EU? Somewhat, but not completely.

What stands out most, however, is the tension between the limits on credit quality and agreement on partial risk sharing. The decision to extend purchases across the whole spectrum of risk assets rated investment grade was brushed over quickly in discussion as being “more effective” than purchasing highest-quality assets alone. This allowed all government bonds to be included in the PSPP (except, of course, Greece) providing crucial support for peripheral assets despite ESM. Meanwhile, by way of trade-off, risk sharing was rejected for some assets given the “institutional structure” and “architecture” of EMU and “the Treaties.” What are those constraints? Presumably the fiscal primacy of the Bundestag in particular.

So there was a trade-off. The periphery would be included in asset purchases, but there would be no risk sharing on these assets. The alternative was presumably only purchasing AA to AAA credits but full risk sharing. But this would have meant the whole Eurosystem sharing the risk on, say, German and French assets while hoping that portfolio rebalancing would eventually benefit the periphery. A “trickle down” approach to monetary policy.

The whole discussion is ridiculous, of course. Each member state should have been required to agree to share the fiscal costs of monetary policy at euro inception. This would allow complete risk sharing of asset purchases. So the problem here is not with monetary policy, but the incomplete delegation of quasi-fiscal risk sharing due to shared monetary policy. It is not the proportionality of monetary policy that should be under consideration, but the disproportionate delimiting of fiscal policy.

In any case, the ECB’s deliberations contribute to, but do not appear to clear up, the issue of proportionality. Were it so simple!

END.