It’s now roughly 4 months since we last lamented here the continuing monetary madness in Argentina and the failure of the authorities to address the sustainability of monetary policy as part of the debt restructuring negotiation. The restructuring is over, but the monetary mayhem continues.

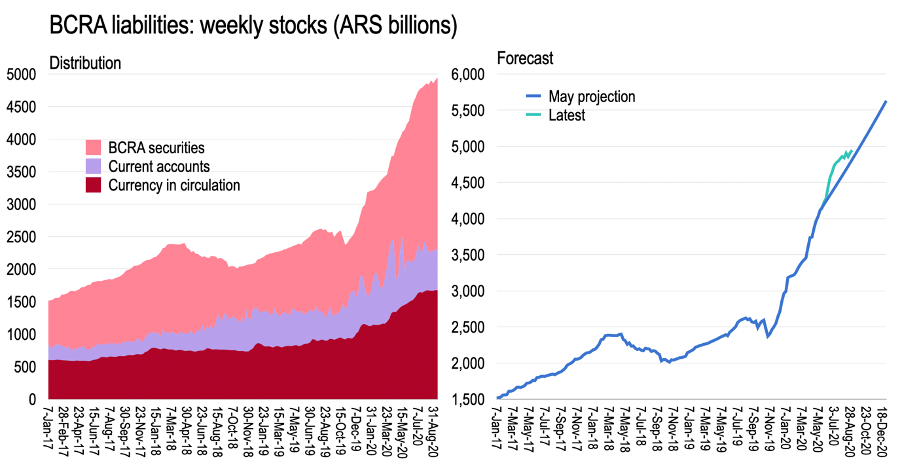

In May we constructed a forecast of BCRA balance sheet liabilities through end-2020. At that time BCRA liabilities were expected to reach ARS5 trillion in the first week of October, with YoY growth in liabilities reaching 100% shortly thereafter.

Where are we today compared to the forecast then?

Well, BCRA liabilities—defined as the sum of cash in hand, current accounts, and BCRA liabilities—reached ARS4.9 trillion on 7th September, which is a 91.8%YoY growth. We are closing in on the May forecast but have actually exceeded the expected stock so far (see chart at end).

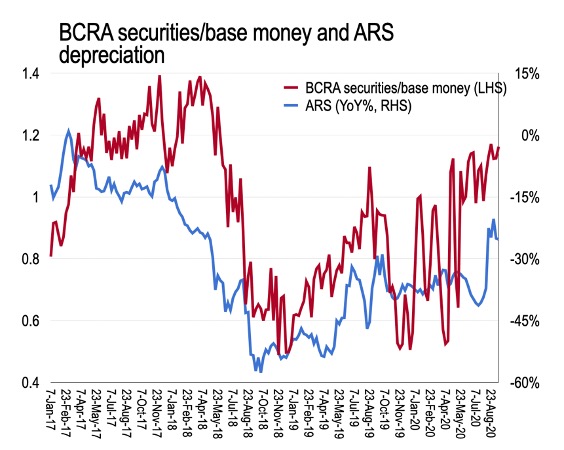

The outstanding value of LELIQs is now ARS2.7 trillion, which is now 16% larger than outstanding base money. Historically, periods where BCRA securities have out-sized base money liabilities has been associated with nominal exchange rate weakness. Crudely put, in order to change the composition of BCRA liabilities from interest paying liabilities at about 40% to non-interest-bearing cash, a bout of inflation is needed to raise demand for currency. This can be achieved through a weaker nominal exchange rate and inflation, changing the composition of liabilities from LELIQs toward base money as residents need more cash to engage in everyday activities–reducing the ratio of LELIQs to base money, allowing the exchange rate to temporarily stabilize. This happily also raises the local currency value of BCRA foreign assets. If they can’t accumulate reserves, they can revalue them.

However, this raises the local currency value of government debt which is denominated largely in USD, converting central bank liabilities into a greater government debt burden. And so we are looking at another period of exchange rate weakness in Argentina ahead which will weigh on debt sustainability just as the IMF is in town.

And the Finance Minister is providing more evidence that while Argentina produces great footballers, they produce terrible macroeconomists.

What ought to be clear by now is that Argentina’s debt restructuring has been a failure. Together with the IMF, they didn’t deal up front with the consolidated monetary-fiscal-financial structure. This is a failure of the new government and the international monetary system.

END.