Argentina’s reliance on persistent monetary financing of the fiscal deficit continues despite obvious deleterious consequences, reminiscent of the Einstein’s notion that “the definition of insanity is doing the same thing over and over and expecting different results.”

Reflecting upon the plan initiated by the incoming Macri administration in 2015, former BCRA Governor Federico Sturzenegger recently explained how the “speed of disinflation … was constrained by the fact that it was agreed that part of the fiscal deficit would be monetized in order to diminish the need of debt financing during the transition to a healthier fiscal result…” And this could not be sterilized owing to the “weakness” of the BCRA balance sheet.

When the IMF’s rescue program was agreed in 2018, monetary financing of the deficit became strictly prohibited—but “profit transfers” from the bankrupt central bank were allowed. With the breakdown of the program following the PASO result, money printing resumed.

More recently, incoming Finance Minister Martín Guzmán has committed in communication with creditors to finance primary deficits over the first three years of the Fernandez administration through “seigniorage,” a repeat of the effort by Macri to avoid debt financing. The primary deficit in 2020 was pencilled in at 3.1%, followed by 1.0% in 2021 and 0.5% in 2022 before balancing in 2023. That’s nearly 5% of GDP in money printing between now and 2023. Yet these figures don’t count the impact of COVID-19 against which the authorities have rightly committed to act.

The IMF’s technical analysis of Argentina’s debt sustainability postulates that the ratio of base money-to-GDP will stay constant at 7.7% through 2030. Since base money today is perhaps 8% of GDP, if this indeed a true measure of money demand, there isn’t much scope for such monetization without either considerable sterilization or further ARS weakness and inflation to drive up nominal GDP and money demand.

Yet BCRA continues to function without any meaningful interest-earning assets, so any sterilization now is only an act of greater monetization in the future. And this doesn’t begin to factor in the continuing interest burden of currently outstanding BCRA sterilization instruments.

So, while the world focusses this week on the renegotiation of Federal Government debt, the real guide to future sustainability continues to be reflected in the changing financial structure of Argentina’s central bank. To this end, how might BCRA balance sheet evolve in the period ahead?

***

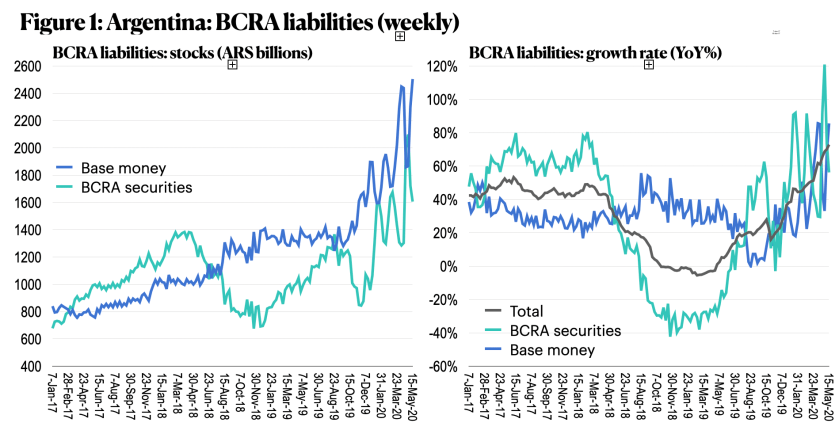

Key BCRA liabilities—the sum of base money and near-monetary liabilities, meaning recently LELIQs at 7- or 14-days—are currently expanding at the fastest pace since 2004.

Weekly data below (Figure 1) shows base money and BCRA securities—LELIQs or equivalent—since 2017 (left chart) and year-on-year growth (right.) The recent experience of base money targeting—0% growth of high-powered money—indeed drove down base money growth in 2019. But this only served in increase near-money liabilities of BCRA, which grew at close to 60% in 2019 and which were offered a handsome return, but this was ultimately only a Ponzi scheme. More recently, especially since the re-imposition of capital controls, growth of these combined liabilities of BCRA is closing in on 80% year-on-year; base money and LELIQ growth zig zag as periods of sterilization and monetary slippage intersect, but the direction of travel in terms of overall growth is clear.

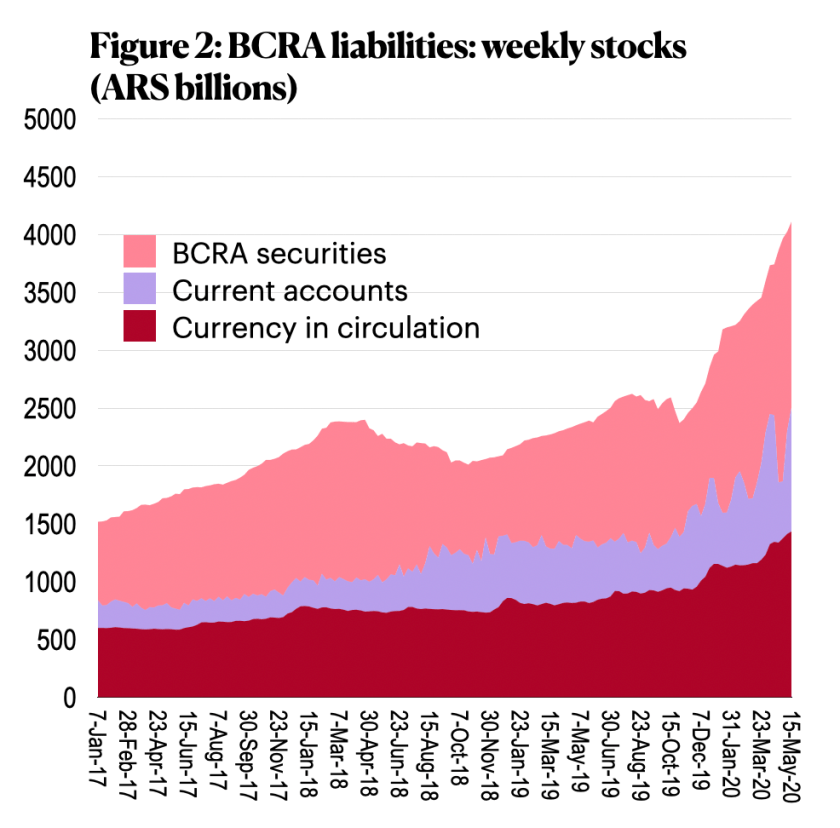

Figure 2 decomposes these BCRA liabilities further into currency in circulation (cash in hand), current accounts of banks with BCRA, and near-monetary securities. While demand for “cash in hand” for transactions drifts upwards, the electronic intersection of current accounts and LELIQs comes across as quite psychedelic to suggest money base expansion at an unhealthy clip.

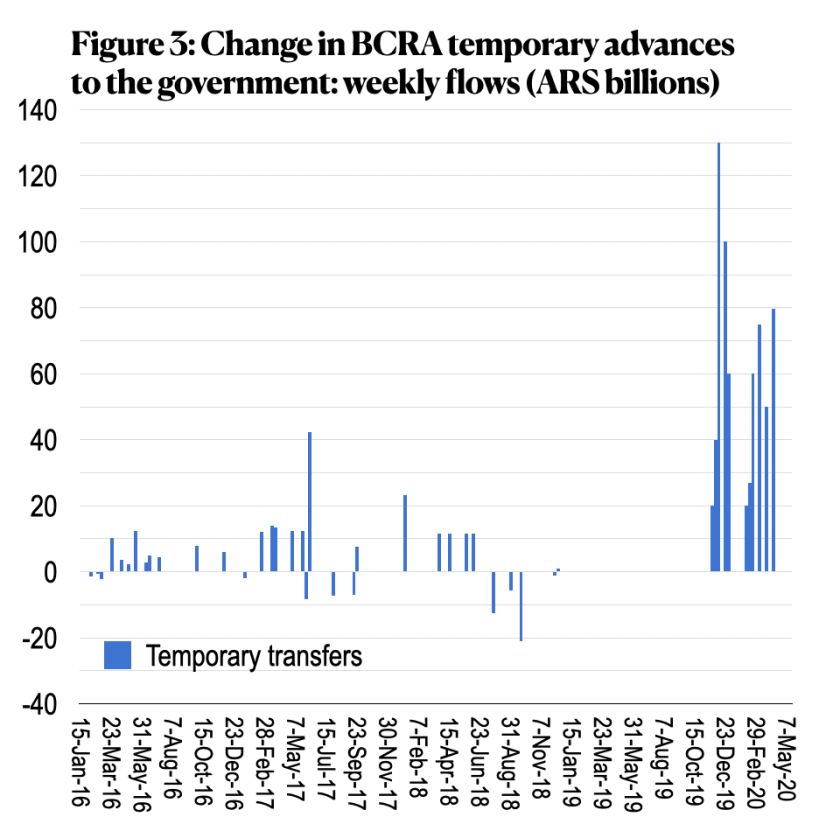

What is driving this expansion? As noted above, even before the IMF program became derailed, profit transfers were acceptable, transfers not. In late May 2019, ARS77bn in transfers of profits from BCRA to government opened the floodgates. After PASO, in August, a further ARS127bn. Then “temporary advances,” disallowed under the IMF program, were re-instituted in November, before the Fernandez administration took office. These increased in frequency around the turn of the year (Figure 3). Since November there has been ARS662bn temporary advanced to the government. If 2019 GDP was about ARS22 trillion, that’s financing of about 3% of this base over 6 months.

But there’s more. Profit transfers continued, reaching ARS600bn in total this year, of which there has been ARS290bn this month alone. Combined profit transfers and temporary advances of ARS1,262bn since early-November, nearly 6% of 2019 GDP, is keeping the government afloat while negotiations with creditors continues. But these are nominal liabilities with “real” macro-financial consequences, including on the exchange rate and inflation.

As well as these transfers, we also have to factor in the net interest payments the BCRA has made and will have to pay throughout the rest of this year. On the asset side, in December, the previous accounting effort by BCRA to write-down the value of assets in line with asset pricing was overturned. These essentially “stale” financial claims were revalued to create some illusion of central bank solvency as net equity of the central bank went from -ARS163bn to +ARS1,985bn in the final week of 2019. But these are “stale” because they don’t offer any income flow to a central bank in desperate need of resources to cover the cost of monetary policy. While Federal Government amortization and interest projections continue to report a string of coupons on Letra Intransferible through 2028 of USD2.1bn, these coupons are immediately handed back to the Federal Government as profit, and written out of the fiscal interest balance, so they are entirely stale from the perspective of contributing to monetary stability. The only meaningful resource at the disposal of BCRA for financing the cost of monetary policy is the printing press.

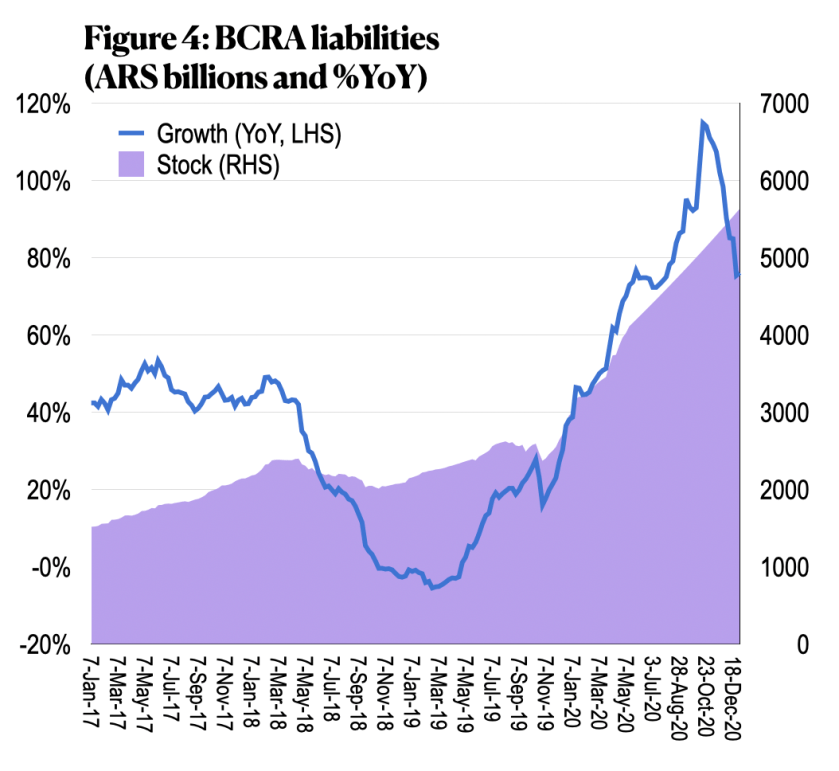

So BCRA can only expand liabilities by printing money to finance itself. If the existing stock of LELIQs pays 40% interest (annualized), which is capitalized through end-2020, then that’s an additional expansion of near-money liabilities of ARS462bn.

Moreover, suppose the government deficit for the rest of the year is an additional ARS990bn (making the full year primary deficit 6.8% of GDP, from 3.1% projected pre-COVIS.) That’s ARS30bn per week for 33 weeks, distributed evenly, through year-end. If half is sterilized by being added to LELIQs (at 40% interest), and half added to base money, we get a forecast for our measure of total BCRA liabilities. Year-on-year growth tops out at over 100% while total liabilities drift above ARS5,500 by year-end compared to ARS2,960bn end- 2019 (Figure 4.)

Beyond this, Guzmán has indicated to creditors a desire to increase gross international reserves over the course of this year by around USD6bn, which would be another ARS400bn added to BCRA liabilities to match these assets—sterilized or otherwise. This is not factored into Figure 4 as it seems so fanciful. We already have what we need.

Now, I don’t want to be seen to be constantly picking on Ivy League Professors. But really? Why not fix the glaring hole in the BCRA balance sheet through unimpeachable capitalization—then factor that into the debt sustainability assessment when discussing with international creditors the necessary debt relief? That’s what I did.

Of course, creditor’s superficial insistence that debt held by BCRA, along with social security funds, should be consolidated in the sustainability assessment is convenient for them as a means of squeezing debt-to-GDP into negotiations. But the response ought to be that the flow cost of monetary-fiscal sustainability—including the interest paid on central bank liabilities—is more important than naïve stock accounting. And if they want to consolidate the public sector analytically, then it should be done properly by factoring in the interest cost borne by monetary policy.

So, to repeat what I’ve argued before, the Argentine authorities ought to have factored in the cost of monetary sustainability into the need to create fiscal space in their negotiations. The IMF failed—once again—to address this in their “technical note.” But that’s no reason that it should not be fixed.

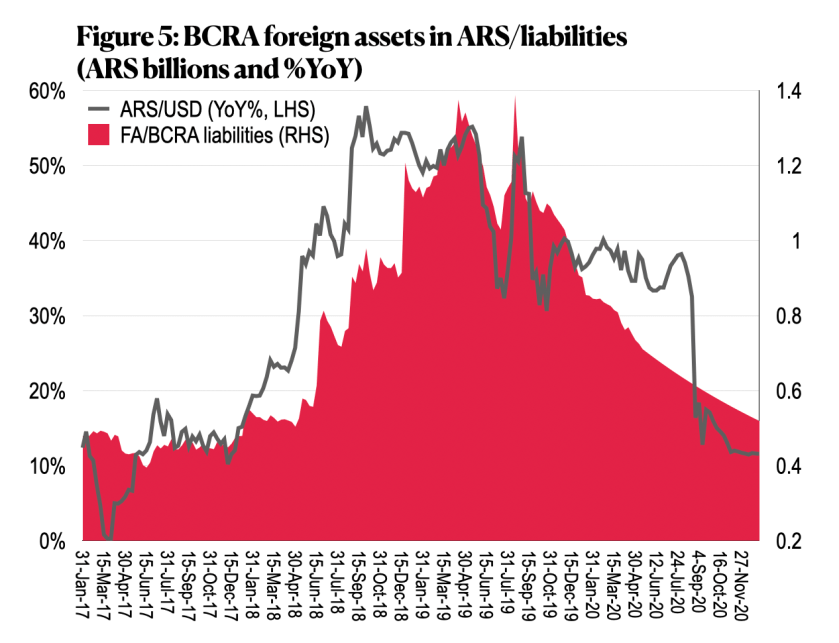

Why does this matter. It’s difficult to get the weekly BCRA balance sheet data to speak to this precisely, but Figure 5 is an attempt to do so. It shows the ratio of BCRA (gross) foreign assets measured at the prevailing exchange rate to our wider measure of BCRA liabilities—base plus near-monetary—as well as the depreciation of ARS through time. We assume ARS does not move from the May level in projections.

Hopefully Figure 5 suggests, of not clearly, that historically what happens is this. As BCRA liabilities expand due to monetisation, this creates pressure on the currency—so BCRA intervention ensues. But this can’t continue as reserves are scarce, so liabilities expand, causing the ratio to drift lower. After a while the liabilities are so much greater than assets that the exchange rate jumps higher—revaluing foreign assets in local currency terms to be sufficiently great to halt depreciation pressure, at last for a while.

Now, this chart has much missing that would be useful but can’t be removed from the weekly balance sheet—such as foreign liabilities (on balance sheet) and program money (off balance sheet). But is does speak to the fact that the expansion of BCRA liabilities over the next 9 months will be huge when compared to the exiting stock of foreign assets. Even with capital controls it will be difficult to keep a lid on this. Hence the black market and blue-chip swap rates imply ARS closer to 120 than the current 67. So even if an agreement is possible with creditors, the exchange rate will quickly destroy the assumptions upon which the negotiation hinged. And monetary madness in the Pampas will once again ensue.

END.

2 thoughts on “Monetary madness in the Pampas”