European Central Bank (ECB) non-monetary policy meetings are understandably less interesting than their monetary policy counterparts—there’s seldom much to whet the appetite amongst the various technical Decisions on swap lines, audit results, and feasibility reports. And there’s no press conference.

Glancing through the output from these non-monetary meetings is like rubbing sandpaper into one’s eyes.

Not so in today’s summary of non-monetary Decisions taken in August and September, which indeed offers something a little different.

The fourth item reported on there is as follows:

Guideline amending the Eurosystem reserve management services (ERMS) framework. On 7 September 2020 the Governing Council adopted Guideline (EU) 2020/1284 amending Guideline (EU) 2018/797 on the Eurosystem’s provision of reserve management services in euro to central banks and countries located outside the euro area and to international organisations (ECB/2020/34). The amendments are aimed at further increasing transparency in reporting and information sharing within the Eurosystem and improving analysis of the functioning of the ERMS. The Eurosystem central banks are to comply with the amending Guideline from 1 April 2021.The amending Guideline is available in EUR-Lex.

Now, this reads like some dystopian Doublespeak. So, let’s unpick it. Reserve managers at central banks with large international claims resulting from “balance of payments” management, such as accelerated sharply during the 2000s, typically hold claims on government securities of reserve currency issuers—not least because such securities offer a coupon. Dollar claims are held as US Treasuries or Agencies, euro claims as Bunds or OATs, for example. And typically at short tenors.

However, in recent years reserve managers moved into deposit claims at various central banks instead of holding securities. There were various reasons for this. In the US, the Fed encouraged a liquid deposit buffer (via “reverse repos”) to forestall a run on securities by emerging markets, say, during times of dollar stress. Alternatively, as a result of the safe asset shortage and the negative yield available across many jurisdictions, as well as the negative dollar basis, national central banks (NCBs) across the Eurosystem as well as the BOJ have seen an increase in non-resident local currency deposits.

Now, since these central banks don’t provide deposit services for any old random who rocks up with a bag of folding money, these are fairly limited services to a select clientele. These are typically reserve managers of other central banks seeking to deploy part of their portfolio within that particular jurisdiction but without taking on the risk associated with the private banking system. Hence the Eurosystem Reserve Management Services (ERMS) referred to in our Doublespeak above.

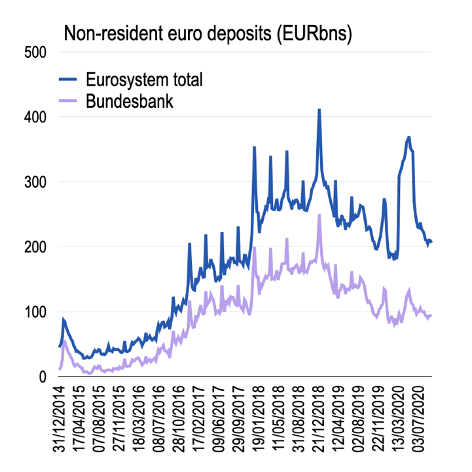

For context, the chart below shows the total non-resident deposits with the Eurosystem (without netting out the Fed swap lines, which have been prominent this year) as well as the Bundesbank reporting of the same item (where Fed swaps don’t matter since they net out through the TARGET2 system.) What is fairly obvious is that from being rather slight in about 2015, these deposits increased sharply to nearly EUR300BN in 2018. (For more discussion of the quarter-end noise in these deposits and the overall trend, see here.)

So the ECB Governing Council earlier this month revised the guidelines “on the Eurosystem’s provision of reserve management services in euro to central banks and countries located outside the euro area and to international organisations … aimed at further increasing transparency in reporting and information sharing within the Eurosystem and improving analysis of the functioning of the ERMS.”

So far so good. But what were these revisions? For this, we need to consult Decision 2020/1284. And there we learn that the revisions relate to information sharing within the Eurosystem about “new and existing customers and [to] inform the ECB when a potential customer approaches them.” In particular, NCBs within the Eurosystem should obtain the consent of clients making use of the ERMS to share their identity within the ECB and thence others within the system. However:

3. If a customer’s consent to the disclosure of its identity is not obtained, the national central bank concerned shall provide to the ECB the relevant information without revealing the identity of that customer. In that case, that customer’s limit for the Tier 1 investment facility balances shall be set to zero by each national central bank which does not obtain that customer’s consent to the disclosure of its identity to the Eurosystem central banks.’

And what does this mean exactly? Well, clients using the ERMS have a series of investment tiers available to them from NCBs of the Eurosystem. And as Bundesbank explains here, the Tier 1 investment offers the best terms they offer as such deposits will be remunerated at 0bps when the deposit rate is negative. However, there is an unspecified “customer-specific maximum investment amount (tier 1 limit)” available at this top rate. In contrast, roughly speaking, Tier 2 investments are available at the market rate (currently negative) after which “excess balances” are remunerated at -15bps below the deposit rate.

Putting this together, what do we get? The Eurosystem decided that they wanted to share information on reserve managers making use of Tier 1 deposits (at 0bps) across the system. And each NCB should obtain consent from clients for such sharing of information. But if the client refuses, then their Tier 1 deposit privileges will be revoked by each NCB.

This seems to be saying that the ECB is concerned that reserve managers might have been approaching NCBs separately to enjoy the benefits of Tier 1 deposits at 0bps without this information being known across the system. Hence, some reserve managers could be making multiple use of the Tier 1 bonus rate.

Now it is possible that this has not been happening—and this is a pre-emptive measure to ensure this loophole cannot be exploited in the future.

Alternatively, it might be that some reserve managers have been gaming the Eurosystem! Hence my excitement. Perhaps I should go to bed.

END.