Euroarea monetary control pdf version.

It’s remarkable how the euroarea crisis elevated arcane relations between central banks within the Eurosystem to dinner table talk for households across Europe. After decades of disregard, central bank balance sheets and liquidity management are fashionable once more.

Largely unnoticed, however, a more recent set of connections between central banks of potentially greater significance has emerged. This time, the links are not withinthe Eurosytem but external—between euroarea national central banks (NCBs) and non-euroarea central banks (NEACBs) and their reserve asset managers. That is, growing deposits by NEACBs with NCBs since the European Central Bank’s (ECB) asset purchase program (APP) have the potential to distort future liquidity control—indeed, they are now crucial for projecting Eurosystem liquidity, the yield on euroarea safe assets, and the euro itself.

Let’s take a step back. Since June-2015, the share of “currency and deposits” in total reserve assets held by NEACBs, as reported to the IMF, increased from roughly 3% to 8% (Figure 1). That is, reserve managers rotated assets from global coupon-bearing securities towards deposits with other central banks. Of a stock of reserve assets of near €9½ trillion, the increase was about €400 billion.

What does this have to do with the Eurosystem? Well, over the course of APP roughly €600bn of euros that would otherwise sit as excess liquidity at domestic banks were “sterilized” due to: larger cash buffers held by resident governments on increased bond issuance (€150bn); financial intermediaries not subject to reserve requirements selling into APP and deposited with NCBs (€100bn); and, most importantly, growing non-euroarea resident deposits (largely NEACBs, €350bn).

Indeed, as of December, non-resident euro deposits at NCBs exceeded €400bn. Two forces appear to have driven these growing claims. First, as reserve managers sold bonds into APP, or saw claims mature, they recycled into euro cash at NCBs rather than securities. This accounts for the secular increase (perhaps €300bn). Second, quarter-end shortages of dollars amongst private banks in core countries, subject to new regulatory requirements, evolved a reliance on NEACBs providing dollar securities to pad their balance sheets. Euros posted as collateral in these repo operations wash from banks into reserve manager accounts, mainly at the Bundesbank—imprinted also in quarterly TARGET2 moves.

Why does this matter? Five reasons:

First, Eurosystem excess liquidity is now closely linked to official reserve manager portfolio allocation, not fully within the ECB’s control (something not factored into Praet’s projections). Indeed, if NEACB claims on NCBs remained unchanged since 2014, excess liquidity today would be above €2.1trn instead of €1.8trn. And these reserves—larger than total APP purchases in 2018—are waiting to be redeployed as yields normalize. Alternatively, should yields remain compressed, growing NEACB claims couldsqueeze excess liquidity further.

Second, it challenges the narrative that an important part of the global impact on the ECB’s APP has been through the recycling of non-resident portfolio claims to the outside world (see Coeure). Not so. Rather, given asset prices, perhaps half net non-resident portfolio sales during APP instead rotated into euro deposits. Isolating portfolio flows in the balance of payments without looking at other investment is distorting. And perhaps the biggest global impact of APP, therefore, has been on reserve manager portfolio allocations.

Third, the yield on euroarea safe assets is now determined by the marginal interest rate available to NEACBs (Figure 2). The Bundesbankreveals an interest on the unspecified excess float held by reserve managers at the deposit rate minus15bps—thus currently -55bps. As a result, absent alternate safe assets, NEACB claims on the Eurosystem increased most when the yield on short-end bunds fell below -55bps. This provides a cap on short-end yields, therefore.

Fourth, quarter-end shortages increase the links between NEACBs and the Eurosystem, providing for the former an opportunity to offset some of the cost of negative yielding euro assets. However, these flows challenge any interpretation of quarterly changes in IMF reserve asset allocation data: how should these repo operations between NEACBs and euroarea banks be unpacked? For example, using the IMF’s CPIS and allocation of international reserves data, as well as ECB NCB balance sheet data, it is apparent a growing share of reserve manager claims on the euroarea is now in the form of deposits with NCBs (Figure 3 provides an estimate for end-2017). The increasing dollar-liquidity provision needs to be factored in when estimating quarter-end euro allocations.

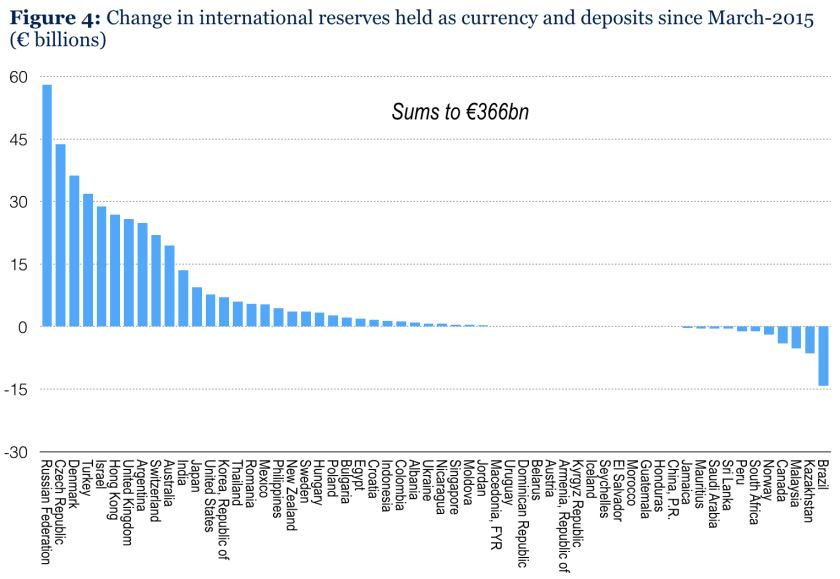

Fifth, interlocking global central bank balance sheets are now of greater interest than intra-system TARGET2 balances. Indeed, the fact that numerous central banks today likely hold more than one-third of their reserve assets in the form of negative yielding deposits at the Eurosystem (e.g., perhaps Australia, Czech Republic, Denmark, Turkey) is remarkable (Figures 4 and 5). This is a tax on non-euroarea residents.

In summary, the legacy of the ECB’s APP is more nuanced than often supposed. Growing links between the Eurosystem and national central banks outside the Eurosystem have the potential to challenge liquidity management in the future. This also represents postponed APP purchases, since these deposits can be recycled back into euroarea assets raising liquidity once more. For example, over the past 4 weeks, non-euroarea euro deposits have declined €27 billion, defying the seasonal pattern of accumulating deposits in 2017 and 2018 (Figure 6). This suggests anticipation of today’s dovish ECB meeting caused reserve managers were rotating into euroarea fixed income assets to benefit from the rally in asset prices. This is as large a flow as APP purchases each month during 2018H1.

But all this is just another way of underlining the flaws in euroarea fiscal policy—and the shortage of global safe assets. Should euroarea fiscal failings, alongside reserve manager portfolio choices, eventually hinder euroarea liquidity management, then flaws in euroarea macro-financial design will once more be laid bare for all to see.

[End.]

I am glad I ve come across your work today! More than self reinforcement you explain my practitioner feelings very interestingly and give me a lot of angles to dwell upon.

LikeLike