ITS USEFUL to be reminded once again of the flaws that underpin the IMF’s World Economic Outlook (WEO) publication—as well as the fact that the Fund continues to fail to pursue her global multilateral surveillance responsibilities. Indeed, last week’s WEO provides yet more ammunition for those who claim the Fund peddles style and not substance, lacks an analytical basis for meeting her obligations.

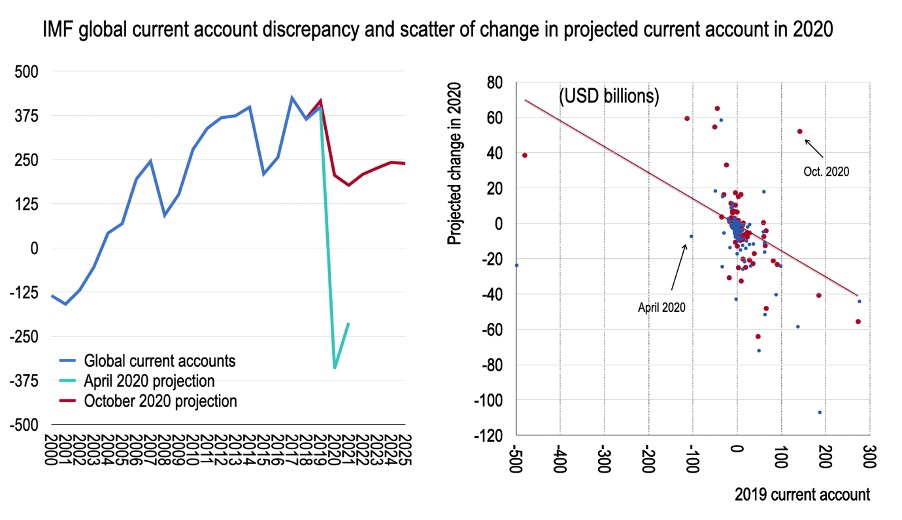

But first the good news. This blog noted in a belligerent style how the April WEO assumed the global current account moved from a surplus “discrepancy” of USD375BN in 2019 to deficit of nearly USD375BN. The discrepancy itself is a puzzle that we need not solve here. But that doesn’t mean it can be assumed away.

The assumption that the global current account discrepancy would swing from surplus to deficit, a change of nearly 1% of global GDP, was a superb illustration of the fact that the WEO is a useless document.

It is politically convenient for each team to independently produce a forecast convenient for country authorities or in order to generate headlines about the financing needs of the emerging and developing world. For example, in early April Managing Director Georgieva captured headlines with the following: “We estimate the gross external financing needs for emerging market and developing countries to be in the trillions of dollars, and they can cover only a portion of that on their own, leaving residual gaps in the hundreds of billions of dollars. They urgently need help.”

What has instead emerged is limited external current account adjustments, and domestic saving being readily available in many—though not all—emerging and developing economies. Something of the Feldstein and Horioka puzzle remains—domestic private saving moves in line with government deficits.

But what this naïve forecast in April revealed is simply that the IMF fails to track in a consistent way global saving-investment movements—and does not have an analytical approach to take a multilateral view.

And so this week, contra April, the WEO data dump has corrected this global discrepancy. A scatter of the change in 2020 current account versus 2019 shows that the April projections (above right, in blue) have been tempered (red) with a larger number of countries witnessing an improvement in their external current account and fewer large negative deltas. The global discrepancy, therefore, falls only to about USD150BN before increasing close to USD250BN in 2025—closer to recent experience. Given uncertainty as to what constitutes this discrepancy, this is indeed more reasonable.

So, there’s the good news. The IMF does not flunk the basic adding up “smell check” that would otherwise be a fail for any undergraduate studying international macro.

But this doesn’t mean the WEO is close to a useful document. In fact, on many dimensions it is worse than in April. The overall macro impact of the virus has become clearer in the meantime, including the relative current account response. Yet the IMF’s numbers unveil a systematic failure to track incoming data across the world and build an in-house view of the global conjuncture as reflected in the external accounts.

Incidentally, this is not simply an analytical imperative—though this ought to be enough for developing such a view. Rather, the Fund was instituted to take the balance of payments seriously. And there is no other institution in a position to do so.

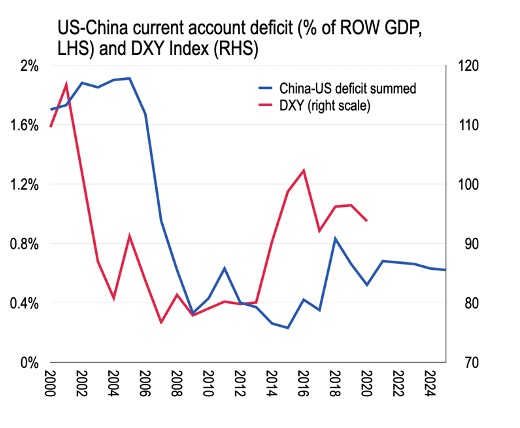

Let’s start with the US-China juxtaposition. On this, Brad Setser has stolen a march this time by pointing to the poverty of the US-China current account projections. On the far left of the above scatter plot, the US can be seen with a current account deficit of about USD500BN. In April the US deficit was projected to widen marginally, by USD20BN or so, in 2020 relative to 2019. But last week the IMF’s latest forecast suggests the US current account will “improve” by USD40BN. The US being particularly important, of course, as an engine of global demand and provider of dollars—for better or worse, the world’s reserve currency.

What’s particularly egregious about this updated forecast, therefore, is the fact that one of the key characteristics of external balances over the past 6 months has been ignored—that being the extent to which the US external deficit has widened, probably a reflection of the relative fiscal response and structure of trade. For example, the US monthly goods and service balance (BOP consistent data) provided by the US Census Bureau has shown a deterioration over the first 8 months of this year on the same period in 2019 of USD22.6BN, meaning a widening deficit. Although there may have been some exceptional gold imports during the period, the direction is travel—reflecting the substantial US fiscal response—has been a widening US external deficit.

Against this, the Fund expects China’s current account surplus to widen by USD52BN in 2020 on 2019. Yet China’s trade balance over the first 8 months has already improved USD27.2BN, and Q3 alone is already USD39BN up on 2019 (though admittedly the September data has only just been published.) Meanwhile, China’s substantial service imports (tourism) have collapsed, which had until recently been a major contributor to holding down China’s current account as the trade balance surplus grew. All the signals are pointing to a stronger 2020 current account surplus in China.

As Setser summarizes the issue: “The US Q2 current account deficit topped 3.5% (highest since the crisis). The IMF forecast for the US deficit this year is 2.1%. China’s Q2 surplus topped 3% of its GDP. The IMF’s full year forecast for China is 1.3% of its GDP.”

Why does this matter? Well, the US-China current account nexus is increasingly important for the global supply of dollars, which in turn helps determine the dollar exchange rate. For example, in recent years China’s bilateral position has taken an ever-larger share in the US current account flows, meaning they absorb and then recycle dollars to the rest of the world. Summing the US-China current account relative to rest of the world GDP gives a proxy sense of the availability of dollars through current account, therefore, as in the chart above. Periods where the combined current accounts are in large deficit, such as in the 2000s, meant dollars were plentiful following the strong USD in the early 2000s. But with such an ample supply, the dollar index (DXY) fell associated with a fall in the overall deficit here. By 2014 the dollar was in short supply to the rest of the world, therefore, at a time where the monetary cycles globally called for a relative tightening of US policy. The stars were aligned for a period of dollar strength which might precede a widening of the combined deficit once more—but the results haven’t been huge.

In any case, the IMF’s latest bilateral current accounts suggest a further reduction in this balance relative to rest of world GDP in 2020, reducing this organic flow of dollars, and hardly increasing through 2025. Thus, the global dollar shortage is not resolved, suggestive of continued USD strength as countries seek out the reserve currency. A wider combined deficit could occur both through the US deficit widening alone, but also through China’s surplus falling as a result of a stronger RMB.

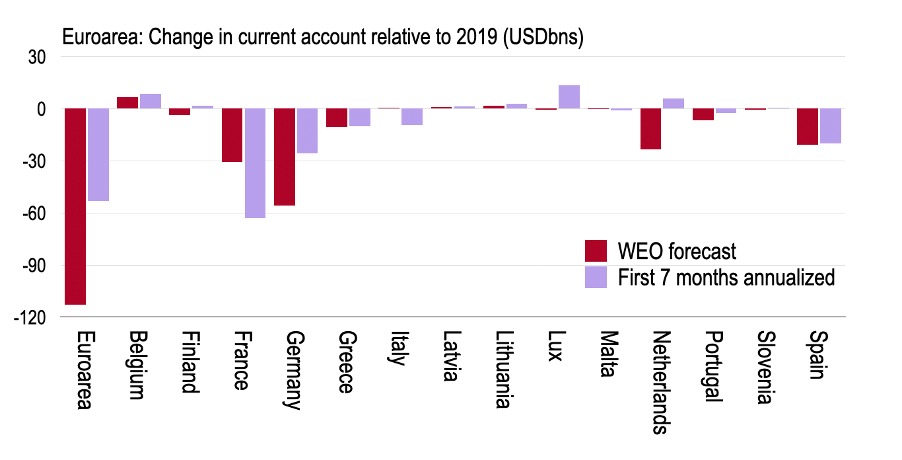

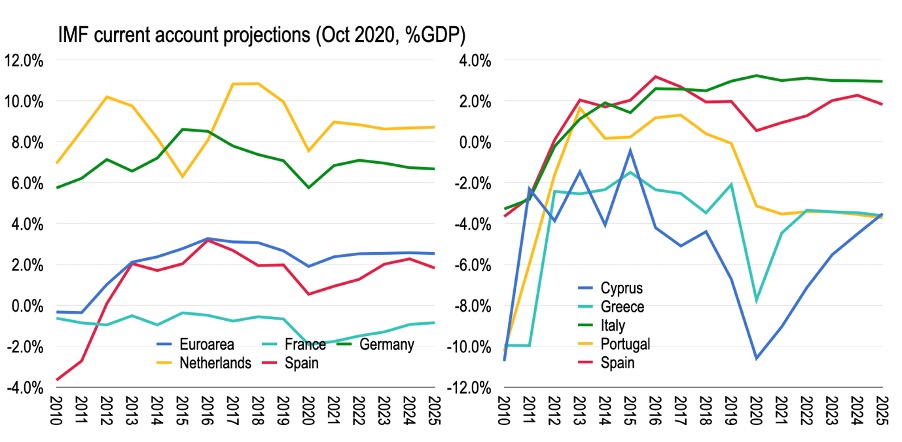

Consider next the current account projections of individual euroarea economies shown above. The latest monthly data from Eurostat and the ECB is through July, which became available in September, and provides a snapshot of the change in current accounts for most of the euroarea countries as well as in the aggregate. Crudely annualizing the change in these monthly readings, converted to USD, on the same period in 2019 and comparing with the IMF’s full year change provides a sense of the forecasts in the WEO. The full year change in the euroarea surplus in the WEO is USD113BN compared with a USD53BN naïve annualized change in the data. Within countries, Italy’s current account balance is expected to improve marginally by the IMF, despite the tourism hit, whereas it her surplus has fallen somewhat. The French deficit has weakened most and is set to be double the WEO forecast when annualised. The German surplus in the WEO is expected to suffer the most, but in reality, will be less than half this. Only Belgium, Greece and Spain are ballpark reasonable compared to the real world. As above, while there are some seasonality issues that might not be fully accounted for by extrapolating on non-seasonally adjusted data, the errors are unlikely to be as large as those built into the WEO.

Turning to other variables, the Euroarea fiscal projections are worse—with read-across to current accounts. The EU Council in July agreed to a new EU Budget for the 2021-27 period alongside a Recovery and Resilience Facility (RRF, the Next Generation EU innovation.) This RRF is EUR390BN in grants and EUR360BN in loans tagged onto the EU Budget proper through 2025. While this is only about 6% of GDP spread over several years, the funds available to some countries could turn out to be substantial. And while the loan part does not improve the current account of EU member states—only assuring cheap financing—the grants component could be an important offset to the external shock of COVID across the periphery. Indeed, understanding the impact on current accounts within the euroarea is an important task for anyone understanding regional and global macro prospects.

How does the WEO evaluate the RRF? The text in Chapter 1 notes that “Beyond their sheer scale, the novelty of the policy actions has also supported sentiment. Prominent examples of new initiatives include the €750 billion European Union pandemic recovery package–fund (more than half of it grant-based) and a wide range of temporary lifeline policies worldwide.” The statistical annex references it only once in the context of Spain: “Fiscal projections… Disbursements under the EU Recovery and Resilience Facility are reflected in the projections for 2021–24.”

But the real reason the RRF is so important is that it represents balance of payments support within the euroarea—in terms of transfers or loans at generous funding rates by leaning on the Franco-German balance sheet. Of these, the EUR390BN in grants are most important in providing net transfers to budgets and therefore reflected in current accounts to offset damage from COVID-19, particularly in the periphery.

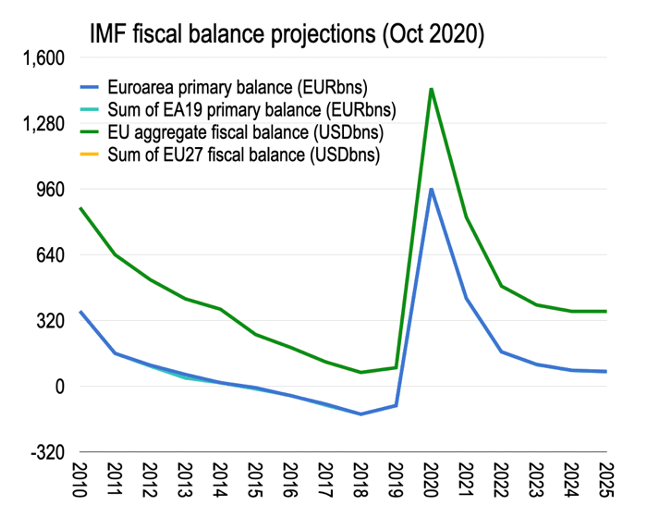

How can we judge how this package has been reflected in the IMF’s analysis? One way is by comparing the aggregate euroarea budget balance with the sum of individual countries, as above. In fact, it’s a bit more complicated since the RRF is an EU innovation, and sits on the balance sheet of the EU in Brussels and counts as non-resident transfers to the euroarea as a whole. Anyway, just to check either way the above chart tracks the EU and euroarea aggregate budgets compared to the sum of individual countries. (The EU27 here being with Croatia and without the UK.) But it’s rather a stale exercise. To a very small margin—such that it can hardly be seen—the aggregate fiscal balance is simply the sum of individual country fiscal balances. What should show up is EUR390BN larger EU fiscal position than the sum of individual countries as Brussels raises these funds to transfer to individual countries cannot be found. In other words, there has been no effort to fold this policy innovation into the fiscal forecasts. This is despite the fact that the statistical annex claims it has been included in the data for Spain—and should therefore be included for all countries for consistency and to allow some cross-country analytical comparisons.

One argument for not including the RRF here is that the WEO only includes in projections “current policies”—or, at least, as the statistical annex describes “National authorities’ established policies are assumed to be maintained.” The question becomes whether the EU Council agreement established in July, even though the NGEU and EU Budget have not yet passed into EU and national laws, can be considered an “established policy.” It seems close enough to be included in the WEO forecasts in my view, as reflected in the fact that the Spain team has itself chosen to do so. But this could be argued.

Still, even if not included in the fiscal figures, could these transfers in particular be included in the current account projections? Have these been updated for Spain or others? The chart below summarises the latest forecasts. For the euroarea aggregate, there will be a large share of EUR390BN in transfers between 2021 and 2025—let’s say ½% of GDP on average, but since this will be lumpy and likely to be grouped around 2021 and 2023. But it cannot be seen. Is this counted in the current accounts of the periphery—where in percent of GDP the net transfers will be even larger? It doesn’t look like it. If the Spain team included this in the fiscal accounts, it should have been reflected in the current account.

The impact on external accounts is a crucial questioning for evaluating this new program, including whether it is sufficient to offset the negative impact of COVID-19 on tourism-reliant peripheral economies. It deserves careful thought.

I could go on. But I think I’ve made my point. It’s fair to say that the WEO is not simply about naïve adding up exercises—that taking a global view of the conjuncture is difficult but necessary, and that’s the IMF’s core mandate.

Why might this gibberish be happening? Well, for one thing IMF staff don’t continually update their forecasts. Perhaps there was an IMF Article IV surveillance mission in June, say, and the team updated their forecasts on the basis of the April data, which has now been superseded. But teams also don’t operate in real time, like financial markets, meaning there is inertia. Incorporating new information requires overcoming bureaucratic hurdles—what will management and the Board say? So forecasts can be as much as 6 months old despite the WEO cut-off being, say, 6 weeks. Hence the fact that IMF publications are seldom—if ever—market moving. There is nothing in there that financial markets haven’t already absorbed months ago.

Yet for some reason financial journalism treats the WEO as if some kind of holy script.

But there is also a lack of management oversight and vision. This comes from the Managing Director and her senior team, of course. But it also comes from Department Directors. The European Department—to name but one—has been dysfunctional for decades, with a string of incompetent Department Directors, including during the euroarea crisis. A new Department Head was appointed in August and could have taken charge with a view to reshaping the limp analysis that has characterised the IMF’s contribution to Europe, but the latest WEO shows he’s either not interested or another stale appointment. The EU Council meeting on the RRF was in July, providing plenty of time for the European Department to work this into a consistent set of forecasts to understand the scale and meaning of this innovation. Alas.

Why should we care? Well, unfortunately, this stuff matters. Whether there are enough dollars provided by the international monetary system over the period ahead will impact exchange rates and prospects for growth globally. The US current account deficit impacts global demand and domestic politics. Whether the RRF provides sufficient transfers to provide current account support for the periphery will likewise prop up their economies and keep down yields—contributing to debt sustainability.

What can be done about this? There are a number of reasonable steps to improve the IMF’s multilateral surveillance. Paradoxically, one is to take the job of macro forecasting away from individual country teams—and make the Research Department the true guardian of IMF forecasting work. Instead of adding up and spitting out country-level forecasts with little concern for how they fit together, they could produce the forecasts for individual country teams—or, at least, for the largest 30-or-so economies. This would mean the Research Department is no longer be an annex of US academia, but more like role of the CBO to US fiscal policy—dedicated to tracking in real time the prospects for the global economy through current accounts, fiscal balances, monetary and portfolio flows. In addition, it would remove the political influence on country teams of authorities—that which makes IMF forecasts little more than the aggregate wish-list of country authorities. Instead, the IMF’s country teams would be able to claim their forecasts are given to them and should be taken up at the Board—instead of manipulating their Article IV interlocutors.

Other steps would be to open up the WEO press conferences to more scrutiny. The WEO document and database could be published 48 hours ahead of the press conference, allowing questions to reflect a considered reading of the document. Questions should be taken from financial markets as well as the press—perhaps in separate sessions.

Finally, IMF management needs to be held accountable for the nonsense that staff produce. In the end, as long as management turn a blind eye—they appear indifferent or ignorant of what is happening—there is no incentive for staff to even try and produce quality analysis.

PS. Don’t mention to me Argentina.

END.

One thought on “Don’t believe the WEO”