All national central banks (NCBs) within the Eurosystem are equal. But one is substantially more equal than the rest.

Indeed, Deutsche Bundesbank (Buba) plays at least three unique roles in the structure and evolution of the Eurosystem: (i) in the creation of currency in circulation—that is, physical euro cash-in-hand; (ii) as reservoir for surplus claims of non-euroarea reserve managers—that is, as a substitute for Bunds when global safe assets run short; and (iii) as final destination, particularly in periods of stress, for excess liquidity created across the euroarea.

We discuss these unique roles before contemplating how they might impact upon the future of the Eurosystem. And in light of the German Constitutional Court (GCC) ruling last week, we briefly reflect on implications should Buba be forced to sell PSPP assets.

- The structure of the Eurosystem

Briefly, the Eurosystem refers to the consolidated balance sheets of the 19 euroarea NCBs plus the European Central Bank (ECB) proper—the latter executive body, based in Frankfurt, has its own balance sheet and staff. Each NCB enjoys a “capital key” share in the system calculated by the average of the weights of each in GDP and population. Together with a small contribution from other members of the European System of Central Banks (ESCBs) this “capital key” provides the ECB’s subscribed capital of EUR10.8bn (of which, EUR7.7bn is paid-up.)

Each NCB creates currency in circulation (CIC) in line with local demand. But total CIC is allocated similar to capital key—though with 8% attributed to the ECB—in proportion to economic size. A series of credit and debit adjustments to NCB balance sheets are therefore needed to translate “true” CIC by each country with their accounting share.

Moreover, NCBs are linked together through another system of credits and debits relating to the flow of electronic euros throughout the euroarea—that being the TARGET2 system.

The overall position of any NCB against the rest of the Eurosystem—ignoring paid in capital and international reserve transfers—is therefore the net position related to both the TARGET2 flows and the adjustment for note issuance.

Finally, NCB liabilities are linked outside the euroarea in two ways. First, five members of TARGET2 are not members of the Eurosystem but might have euro positions (NCBs of Bulgaria, Croatia, Demark, Poland, and Romania.) Second, other central banks are able to place euro deposits with NCBs as part of their reserve manager services—with Bundesbank being the most important recipient.

We will discuss examples of these accounting features as we go.

- Currency in circulation

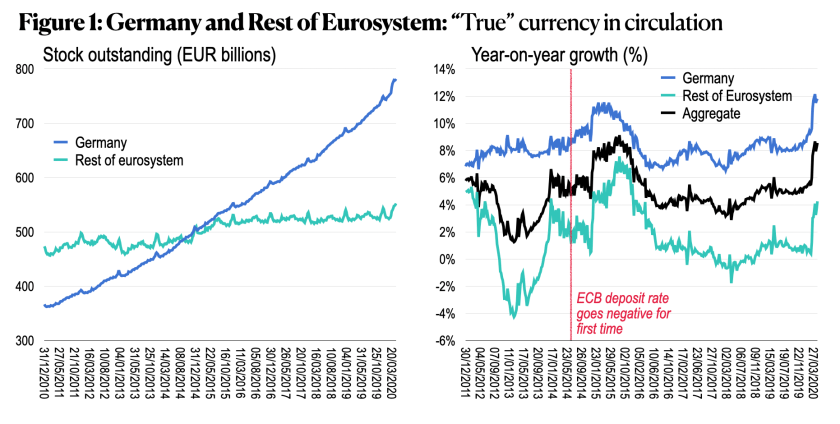

Figure 1 below shows CIC issued by both Germany and Rest of the Euroarea (ROEA) in levels terms (left) and as year-on-year growth (right.) The stock of CIC emitted by Buba has increased from below EUR400bn end-2010 to approach EUR800bn today; in contrast, ROEA has seen currency emitted increase less than EUR100bn over the same period. In terms of growth, except for a time in 2015 when ECB initiated a negative deposit rate policy and asset purchases, CIC growth across ROEA has been around 0%YoY. In Germany, CIC grows consistently around 8%YoY. Since the COVID-19 Crisis, of course, there has been another flight to currency.

More precisely, since end-2014, the Eurosystem in aggregate has created EUR310 billion in banknotes for circulation as “cash in hand”—carried in wallets, stashed under mattresses, hidden within sofas. Of these (net) new banknotes created, Buba has created EUR270 billion. That is, nine out of every ten new physicaleuros created over the past 5 years originate with the Bundesbank.

Taking a longer perspective, on January 1st, 1999 there were EUR342bn euros in cash on the Eurosystem balance sheet as then constituted—of which EUR131bn (38%) were due to Buba. As of May 1st, CIC was EUR1,334bn with EUR782bn (59%) from Germany. Thus, more than half new euro banknotes since inception originated with the Bundesbank, which contrasts with her capital key of about ¼.

This is not to say that currency circulating across ROEA has not increased since, say, 2010. In fact, it could have increased at a faster pace per capita than in Germany, only the local NCB has not been the originator of this cash. As discussed shortly, German-originated notes—through tourism and the like—can wash up elsewhere.

Why is this? Well, no one can be entirely sure. But in 2018 the Bundesbank provided a summary of the uses of euro cash created in Germany, which served as a reminder that euro cash can be sought for domestic transactions, or for hoarding by residents or non-residents. Overall, Buba concluded that “since 2010, foreign demand for banknotes has played the largest part in the increase in the value of German-issued banknotes in circulation.”

What exactly is this foreign demand? The same document suggests “channels of international banknote migration are deliveries of euro banknotes to countries outside the euro area by international wholesale currency shippers, euro banknotes taken abroad by travellers as well as by foreign workers and migrants, and cross-border payment transactions settled in cash.”

Based on various surveys, Buba was able to conclude that at end-2016 about 70% of all euro notes printed by Bundesbank were in circulation outside Germany—and of these the majority (or 50 percentage points, nearly ¾) were circulating outside the rest of the euroarea. In other words, the Bundesbank is crucial in providing euro cash not only for transactions between, and savings of, German residents, but also for the rest of the world—mainly beyond the euroarea.

Seen from the other side of these transactions—as recipient of steady inflow of cash from abroad—authors at Oesterreichische Nationalbank (ONB, that’s Austria’s NCB don’t you know?) have provided a complementary view on “the physical shipment of cash and the cashless transfer of central bank funds via TARGET2.”

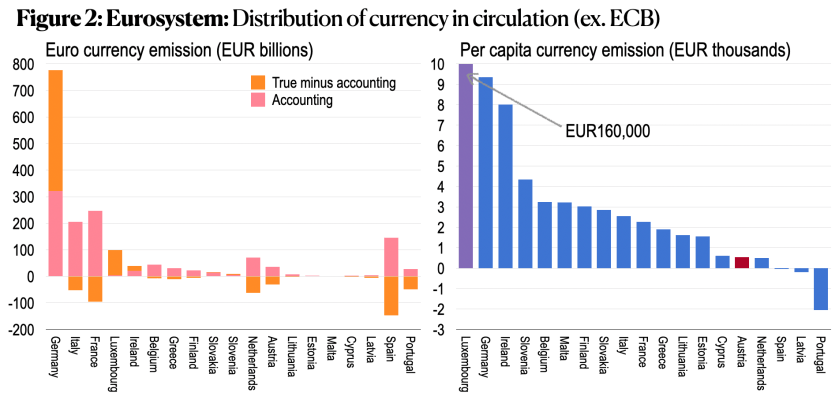

Being both a tourist destination and a gateway to Eastern Europe—the latter, perhaps, a conduit for suitcases full of cash of dubious progeny—Austria finds herself mopping up physical cash almost as fast as local demand itself grows. As a result, the net per capita emission of euro cash by residents of Austria (EUR550) is substantially lower than near-neighbour Germany (EUR9,350)—though both lag considerably behind Luxembourg (EUR161,350).

Figure 2 shows both the accounting and true emission of CIC (left) as well as the per capita distribution of genuine net issuance (right) as of April. The accounting for CIC is (approximately) the capital key share of total cash created as recorded by each NCB. The true (minus accounting) measure is the amount that each NCB actually originates which can be more than the accounting convention (Germany and Luxembourg), less than but still-in-total positive (Italy and France) or net negative (Spain and Portugal.) Popular holiday destinations obviously enjoy their flow of euro notes from elsewhere; their accounting share overstates their net issuance.

When converted into per capita terms (right side) we witness three countries with negative per capita issuance. Spain and Portugal, obviously sunny, and Latvia—sometime stag night destination, but oft suspectedof gorging on cash from, say, Russia. Thus, all are likely ultimate recipients of euro cash printed elsewhere. Whatever the reason, there has been a migration of euro banknotes within the Eurosystem from (roughly) North to South.

A curious feature of this system is that the imbalances due to the emission and absorption of CIC feeds into electronic “imbalances” of the TARGET2 system. This is an important point insisted upon by ONB. For example, consider a euro withdrawn from a cashpoint in Berlin to be spent in Vienna on a cup of coffee and cheap opera ticket. In the first instant, this physical euro is deposited by recipient at a bank in Vienna, whence it is converted to an electronic liability of local banks against ONB.

Suppose Austrian banks then wish to convert this into a claim on the German government for safekeeping. Doing so, ONB converts a liability to the Austrian banking system into one against the Eurosystem through TARGET2—while Buba receives a TARGET2 credit and the German government a debit to said Austrian banks. In this way, Buba’s original cash liability has been met by a TARGET2 asset mirroring ONB TARGET2 liability.

If seen only through the eyes of the electronic TARGET2 system, one might think that Austria had been profligate and giddy taker from the system—whereas in fact Germany has been the enthusiastic provider of physical cash, washing up elsewhere to create a claim on the German government. More correctly, part of Buba’s currency and TARGET2 position net to zero. And should this “liquidity” in Germany be sterilized through a subsequent OMO operation all that would meaningfully remain is a liability between the German government and Austrian private sector! NCBs represent an accounting device—let them net to zero and pretend they don’t exist.

- Non-euroarea euro deposits

An additional link is due to the shortage of euroarea (and global) reserve assets—particularly, government securities—which creates a demand for euro deposits at NCBs by non-euroarea reserve managers. To be sure, such deposits include those due to: (i) swap lines (e.g., the Fed); (ii) non-euroarea TARGET2 members (e.g., DNB); and (iii) other non-resident central bank reserve managers looking for a store of value (e.g., SNB; discussed here). All three can be important, but the latter is crucial. (Non-euroarea TARGET2 balances have been, to date, small; as collateral, Fed swap lines don’t impact system-wide euro liquidity.)

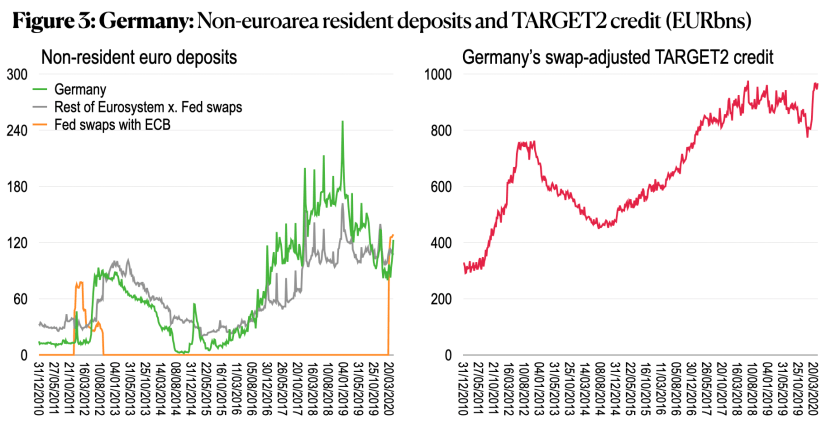

The left side of Figure 3 provides a reasonable decomposition of the removal from liquidity of euros due to non-resident deposits with the euroarea. Fed swap lines can be large, but do not contribute to euro liquidity conditions—rather aid in dollar funding by European entities. During the euroarea crisis—as it was in 2011/12—use of deposits by outside central banks emerged (Switzerland?) including those within the TARGET2 system.

More recently, given asset purchases and negative rates since 2014/15, there was a steady accumulation of non-resident euro deposits, particularly from end-2016-18. Since NCBs offer reserve management services offering (occasionally) a yield greater than that available on safe assets in the euroarea, these become an outlet for overall liquidity that would otherwise remain within the system. Buba became the main channel for this liquidity through late-2018, though other NCBs also matter (Banque du France, for example—though their data reporting, like their canteen, is overrated.)

- Eurosystem excess liquidity

Finally, we are all aware of the TARGET2 balances—per Dylan, “like a mattress balances on a bottle of wine.” An estimate of Germany’s weekly balance is shown on the right side of Figure 3. There is a debit equivalent representing other NCB claims on the Eurosystem. Together, they sit as bookends propping up the cumulative current and (mainly) financial account transactions amongst TARGET2 members—largely the euroarea. During periods of stress, or simply when risk taking falls short of reallocating safe claims from Germany to ROEA, Bundesbank absorbs a larger share of total system-wide liquidity—and banks resident in Germany hold such claims at potentially negative interest.

- Reflections and implications

There are numerous reasons this matters. Before contemplating the recent GCC suggestion that Buba might sell PSPP assets, note the following. The first two special roles note above are liquidity withdrawing for German banks (e.g., CIC and reserve manager accounts), the third is liquidity creating (when TARGET2 credit is increasing). In a sense, Germany withdraws liquidity from ROEA due to capital flows from the system while also distributing some of this liquidity elsewhere (through CIC and as quasi-reserve assets.) The overall impact on the size and distribution of Euroarea liquidity is a tug of war between these various forces.

As such, the following three remarks are non-exhaustive:

First, the secular increase in CIC (largely due to Germany) withdraws liquidity in a way that “organically” erodes the Bundesbank’s TARGET2 credit. In the early years of the euroarea, German banks still provided physical currency, but would do so by posting collateral through standard repo operations—such that, roughly speaking, Bundesbank assets (repos) and liabilities (CIC) would increase in lockstep. More recently, German TARGET2 liabilities have in absolutely size increased nearly in line with CIC. To be precise, from end-2014 to end-2019 the Bundesbank’s TARGET2 credit increased EUR380bn, while true CIC increased EUR240bn. In a sense, 60% of Germany’s increase in CIC since end-2014 has been facilitated by the absorption of liquidity from the rest of the Eurosystem.

Meanwhile, Germany will likely produce about EUR86bn in CIC this year, assuming the leap in cash-in-hand since COVID-19 is not reversed. This is more than the liquidity that would be created by Bundesbank in the course of the “traditional” EUR20bn-per-month in asset purchases set late last year. In other words, Buba’s role as originator of euros for the world as a whole makes her withdraw liquidity from the Eurosystem as a whole. This is “good news” for German banks, if facilitating such “wholesale currency shipping,” as it’s better than -50bps on the marginal euro.

Of course, liquidity would be drawn from the system in general—even if not originated in Frankfurt. But this sheds new light on Germany’s TARGET2 credit.

Second, non-resident depositors also withdraw liquidity when the front-end interest rate is low. But this can also be put back into the system, as was the case in October in advance of the imposition of tiering. And insofar as Buba is considered a safe haven, the TARGET2 credit in Germany once more is an overstatement of a more meaningful position once consolidated.

Finally, while Germany’s (swap-adjusted) T2 credit is at a new record high, it could increase further to touch EUR1.3 trillion by end-2020. But this is simply a reflection of the overall risk profile of euroarea assets outside Germany—alongside Buba’s role as originator of physical currency and custodian of reserve manager claims on the Eurosystem. If the COVID-19 Crisis is mismanaged, a sharply increasing TARGET2 credit will be a reflection of institutional weaknesses. Against this, more secular moves will reflect the historical role of Buba within the system as a whole.

What if Buba withdraws from PSPP?

If this happens without replacement, liquidity in Germany will dip below the required plus tiering ratio, and German banks will look to source liquidity elsewhere. This will cause an increase in front end yields and liquidity will flow into Germany. Some will come from reserve managers, without impacting the rest of the system, but the rest will come from elsewhere within the Eurosystem, causing Buba’s TARGET2 credit to fall, all else equal.

If it happens with replacement Bund purchases by ECB, this will keep liquidity in Germany unchanged while losses from negative yielding German securities will be shared across the system. Germany will have an even larger T2 credit (i.e., liquidity in Germany will be unchanged, claims on the local sovereign replaced by claims on the Eurosystem.) This will reasonably generate legal challenges elsewhere against sharing of losses from negative German yields.

But if replacement instead diverts purchases to other government bonds, this will definitively destroy the capital key while still resulting in a larger T2 credit in Germany. In this case, the Bundesbank arguably gains from having to make fewer losses on assets purchased locally—but will be taking on risk in the form of larger claims on the Eurosystem. And if the system falls apart under the weight of its own internal inconsistencies, the losses facing Buba will likely be greater still than simply sticking to the existing rules.

There are no free lunches.

END.

Thanks for this post

LikeLike

Accurate and useful

LikeLike