Not quite the fireworks of March, the Bank of Italy balance sheet in April nevertheless provides a puzzle for understanding the pace of ECB asset purchases and the support for BTPs throughout the month.

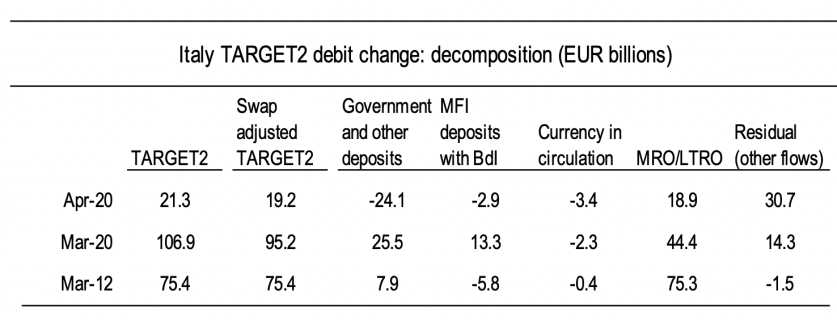

The table below updates a decomposition on the change in TARGET2 balance used last month. The only difference being the change in currency in circulation has been improved to fully reflect Italy’s share in total flows for the month. The March numbers have been adjusted also.

The monthly balance sheet reveals that Italy’s TARGET2 debit increased to an all-time high of EUR513bn but netting out the USD swap lines taken by Italian banks (which increased by EUR2bn during the month) the swap-adjusted TARGET2 position reached EUR499bn. Still a record high, it remains fractionally below the meaningless but nevertheless noteworthy EUR500bn threshold. The swap-adjusted T2 debit increased EUR19bn during the month—reflecting net capital outflows, but on a much smaller scale than last month.

Banks accessed an additional EUR19bn in LTROs in April, about a quarter of the total, while government (EUR24bn) and bank (3bn) deposits increased; also, currency in circulation withdrew an additional EUR3½bn in electronic high-powered money. By way of residual, this implies nearly EUR31bn in additional liquidity was created in Italy during April. Because Bank of Italy only provides the stock of securities held including valuation adjustment (which increased only EUR18bn), this residual is a reasonable proxy for total asset purchases in April. In turn, subtracting EUR11bn in PSPP purchases, this implies PEPP purchases around EUR19.8bn.

Since total PEPP was EUR103bn, this implies Italy’s PEPP purchases were about 19% of the total (or perhaps 25% of non-supranational govvies purchased). This compares to 41% of PSPP purchases during April. So PEPP purchases appear to be running proportionately lower than PSPP—though both still above capital key of 17%.

The below table also suggests March PEPP purchases in Italy were EUR2.5bn (18% of EUR14bn PEPP purchases, this is revised) such that cumulative purchases of BTPs under that program reached EUR22bn (of EUR119bn).

But this its only an estimate; ECB publication of PEPP flows next month will be very welcome indeed.

END.