“We are not here to close spreads.” How expensive were these seven words? It’s impossible to know, of course. But we can put down a marker based on some reasonable assumptions. And they probably cost Italy EUR14 billion in interest payments over the next decade, though it could be even more. That’s EUR2 billion per word.

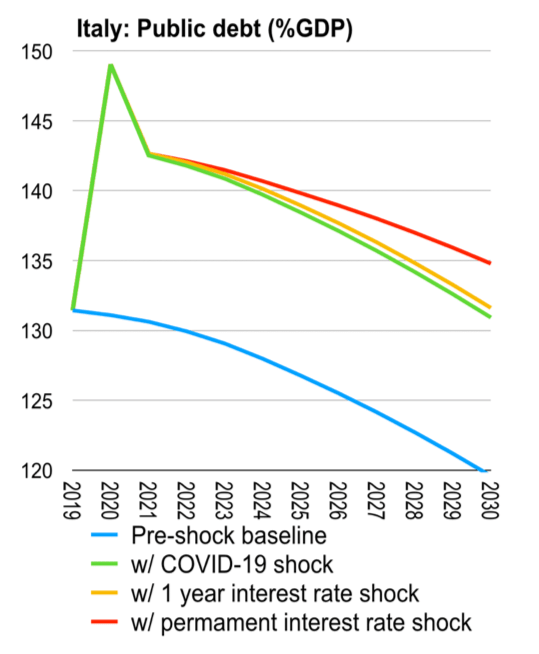

Prior to the COVID-19 Crisis, Italy was running a primary surplus of approximately 1% of GDP, yields on new debt had fallen to historic lows, and debt-to-GDP was on course to touch below 120% by end-2030. See chart.

Then, along came the COVID-19.

It’s very difficult to know at this point the impact on growth and the budget, but there is every reason to believe growth will be substantially negative and a temporary large primary fiscal deficit will be necessary. Here we assume real growth for Italy at -4% in 2020, then +4% in 2021 to offset this. Meanwhile, a primary fiscal balance of -6% for 2021 is assumed before returning to +1.1% surplus in 2021. This could be an understatement of the temporary fiscal hole, however.

The revised debt-to-GDP path is shown below; it jumps to about 150% of GDP in 2020, then comes down sharply as growth resumes in 2021, before continuing to adjust down over the remainder of the decade. Debt-to-GDP ends up about 10 percentage points higher than the baseline.

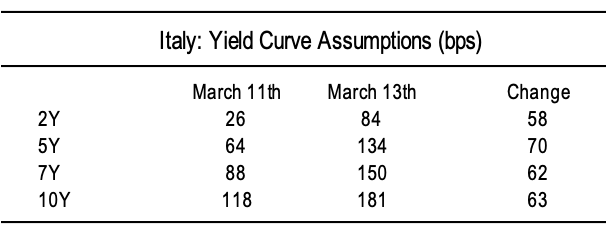

This assumes the yields on new debt are the same as on March 11th last week, however. See table. In fact, yields jumped sharply higher as a result of the ECB press conference on Thursday. Introducing these yields just for 2020, we get a new path for debt as shown. Debt-to-GDP ends 2030 at 131.6 instead of 130.9 without the interest rate shock; this compared with 119.6 in the baseline.

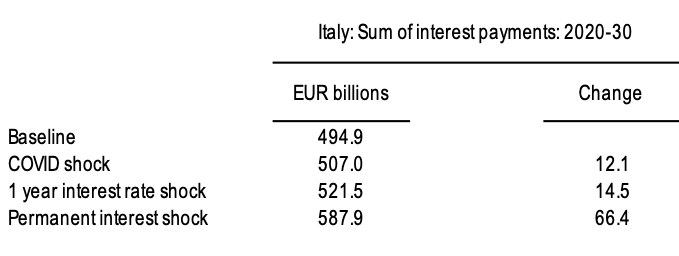

But what does this do to Italy’s interest bill over the 11 years through 2030? In the baseline, the interest will would have been EUR495 billion, an average of EUR45 billion per year. Because of the COVID-19 shock, the interest bill would increase about EUR12 billion to EUR507 billion. Meanwhile, once the higher yields for one year are factored in, the interest bill increases to EUR 521½ billion; that’s EUR14½ billion higher than dealing with the COVID-19 without the interest rate shock.

But imagine instead the interest rate shock is permanent. Then debt-to-GDP reaches 135% in 2030, about 4 percentage points above the COVID-19 shock alone. The interest bill through 2030 increases to EUR588 billion, EUR81 billion more than just dealing with the COVID-19 shock alone.

The problem is, the COVID-19 shock will have a large impact on the need for debt issuance this year. For example, the Italian government will have to refinance at least EUR70 billion in maturing debt this year. Add to this a primary deficit of about EUR100 billion in this scenario, and that’s about 10% of GDP of debt that will needs to be issued at a higher coupon.

A new aircraft carrier probably costs about EUR7 billion. So even if the shock is only for one year, that at least two new aircraft carriers.

Alternatively, each new hospital ventilator costs EUR17,000, so that’s about 850,000 new hospital ventilators.

What a world!

END.

54 thoughts on “Loose lips cost ships: Lagarde’s language and Italy’s EUR14 billion bill”