Greece has been a clear winner in the painful game of watching the COVID-19 health emergency unfold.

Learning quickly from Italy, Greece locked down early and effectively to contain the virus. When the ECB unveiled the Pandemic Emergency Purchase Program (PEPP) on March 18, restrictions on the purchase of Greek assets by the ECB were lifted for the first time, making the small universe of GGBs available for Bank of Greece (BOG) purchases at last. And now the European Union’s (EU’s) EU Budget and Recovery fund (Next Generation EU, NGEU) looks set to make Greece one of the biggest winners in terms of access to grants and loans over the recovery period ahead.

For once the Greeks have not been hung out to dry.

However, for all these recent innovations, it’s important not to forget that the euroarea remains an imperfect currency union. And for precisely this reason there is an important role still for fiscal-cum-debt management policy in planning for the period when this exceptional external support runs off. Indeed, it is arguable that debt management is the only macro policy tool left for managing the economy when fiscal policy is constrained and monetary policy non-existent—and “structural reforms” mere dreaming of a better future.

To think things through, it’s useful to split the policy support to be received by Greece into various component parts and time periods. The question we are seeking to answer is: what is the most favourable use of these policy instruments for the Greek balance of payments?

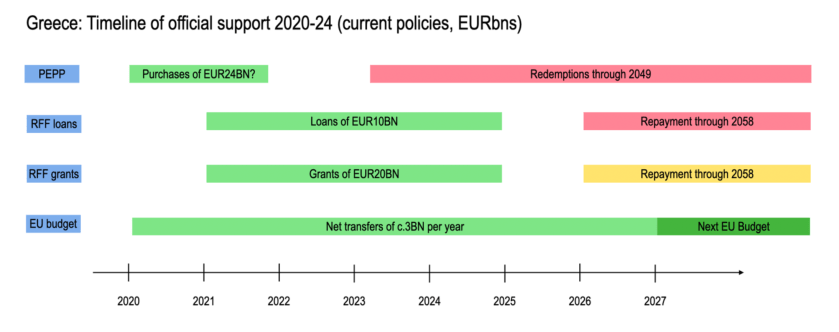

- On financial account, Greece has received substantial support from PEPP. Of total purchases public sector asset purchases excluding supranationals pencilled in at say EUR975BN (of total EUR1,350BN) if Greece enjoys her capital key share of 2.5% then by next June the Bank of Greece could have scooped up EUR24BN in Greek government securities. Considering the stock of long-term debt securities was EUR48BN as of 2020Q1, that’s half the current tradeable stock. Clearly PEPP purchases would run into issue and/or issuer limits at some point without the government issuing more bonded debt. So, there is an incentive to issue more soon to take full advantage of the PEPP flows; note, PEPP purchases absorb maturities from 70-days to end-2049.

- Also, loans available through Recovery and Resilience Facility (RRF) accruing to Greece will provide additional cheap funding on financial account from roughly 2021-24. It’s not clear what Greece’s share of the EUR386BN in loans (in current prices) will be, but EUR10BN has been suggested.

- In terms of transfers on current account, Greece will receive a favourable showing from the RRF grants of perhaps EUR20BN in grants, or about 10% of GDP over, say, 3-4 years from 2021.

- In addition, Greece will receive a steady flow of net transfers from the EU Budget of perhaps 2% of GDP over the period. These transfers have in recent years made Greek net primary flows vis-à-vis the EU roughly balanced—Greece makes interest payments of about EUR2-3BN per year but receives about EUR3BN in net transfers from the EU Budget. So, although Greece never attained a goods and service surplus, the cost of servicing debt—mainly to EU institutions and bilateral loans—has been reciprocated by net transfers from the EU. Debt service need not rely on the goods and service balance or external borrowing, but from EU budget transfers.

In other words, Greece can expect to receive considerable balance of payments support over the next 4 years, summarized in the timeline below.

On the other hand, the PEPP program is currently expected to end mid-2021 while rollovers of maturing bonds will only occur until end-2022. RFF loans are expected to be serviced and repaid from 2026, while Greece will also have to contribute a (relatively small) share to the repayment of grants under RFF. So near-term benefits come with a long-term balance of payments challenge—and Greece was already facing an increase in external debt redemptions from 2022.

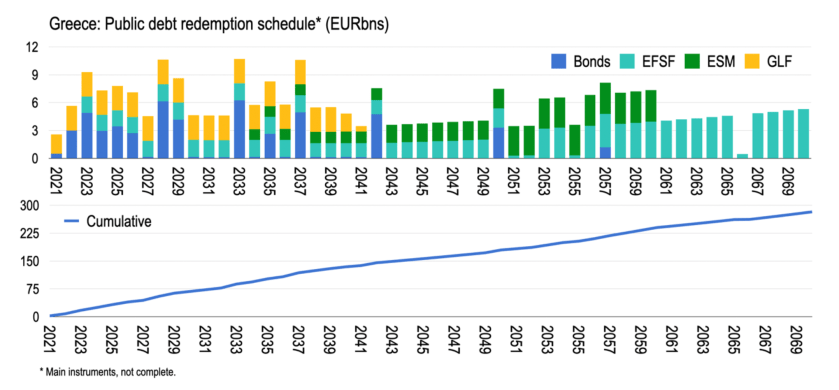

The chart above picks out the main items from the Greek debt redemption profile from 2021. Greece faces cumulative redemptions of EUR40BN through 2026, which is relatively low for an economy of, say, EUR200BN. But redemptions accelerate after years of limited pressure.

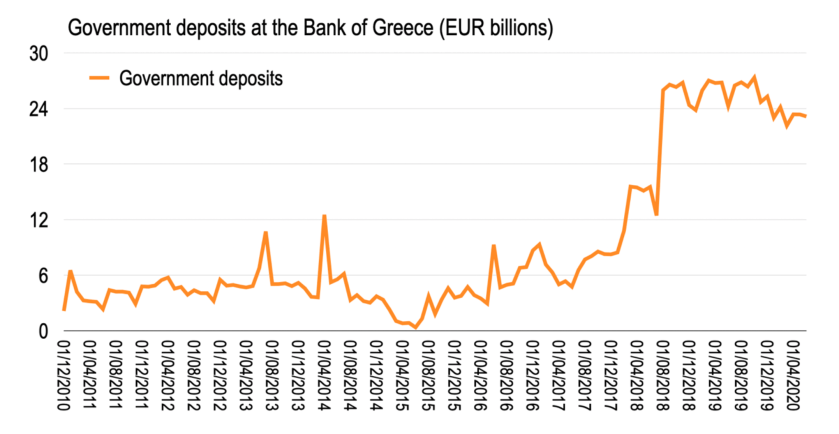

Indeed, one of the reasons Greek debt has traded so well in recent years, in my opinion, is because the government accumulated substantial deposits with the Bank of Greece as the official program ended. Together with a primary surplus, the Greek government built a “buffer” stock of euros which could be used to service debt and prevented external financing challenges. The Greek government has been holding in excess of 10% of GDP in such deposits since late-2018, for example. These deposits were until recently more than enough to repay in full medium- and long-term debt over a 5-years rolling horizon, making default highly unlikely absent fiscal slippage—arguing for a collapse in the yield curve through at least the 5Y point. (The last time I looked at Greece was in 2018 when it was difficult not to conclude Greek assets were set to continue to rally—presentations GR vs PT_18 July 2018 and August 1_2018_Greece.)

This underlines how, in an imperfect currency union, government deposits are the equivalent to foreign exchange reserves for managing the balance of payments—meaning debt and government cash management are a substitute for international reserves inside the euroarea given uncertain market access.

Which brings us to today. What are the prospects for the Greek balance of payments and fiscal policy, and how will these deficits be financed?

Beginning with fiscal policy, the EU Commission (May Spring Forecast) had the Greek deficit in 2020 at 11% and in 2021 about 4%. The IMF (April WEO) rather pencilled in 9% and 8% deficit respectively. Let’s split the difference and say the deficit will be 10% in 2020 and 6% in 2021, with large uncertainty. Assume GDP is EUR180BN throughout, then that’s a fiscal deficit of nearly EUR30BN over the next two years—let’s say EUR20BN this year and EUR10BN next.

As to the Greek current account, again difficult to predict, a number of markers help us narrow in on possible outcomes. To begin with, while the 2019 current account was nearly balanced (EUR2.6BN deficit) this was supported by a considerable service balance surplus (EUR21.1BN) of which travel was about ¾ the total (EUR15.4BN). Now, Greek travel receipts have—as with many others—suffered incredibly since COVID-19. The latest data is from May, when both credit and debit items on travel were down 99%YoY. Finger in the air, suppose the travel credit and debits are both down 50%YoY for the rest of this year, then the current account deficit would increase EUR8.4BN other things equal to reach EUR11BN.

Other things won’t be equal, of course. There will be gains on the oil balance, which improved about EUR2BN over the first 5 months of the year compared to 2019. Meanwhile, transportation and other services credit lost about EUR½BN over the same period. Let’s call this a EUR3BN “gain” over the full year, meaning the Greek current account deficit could touch EUR8BN in 2020, about 4.5% of GDP. With some recovery, let’s pencil in EUR4BN in 2021.

This back of the envelope approach implies the Greek fiscal deficit will be about EUR30BN over the next 2 years, and the current account deficit EUR12BN. The good news is, the government has about EUR22BN in the bank, nearly enough to fund the fiscal deficit and more than enough to cover the current account deficit. So with some additional debt issuance, financing is no concern. The decrease in government deposits with BOG will fund transfers to the domestic private sector, whose spending on goods imports results in a drawdown in bank liquidity and increase in Greece’s TARGET2 debit. The excess of the fiscal deficit over the current account deficit, the private sector saving-investment surplus, is available for portfolio transactions inside or outside Greece.

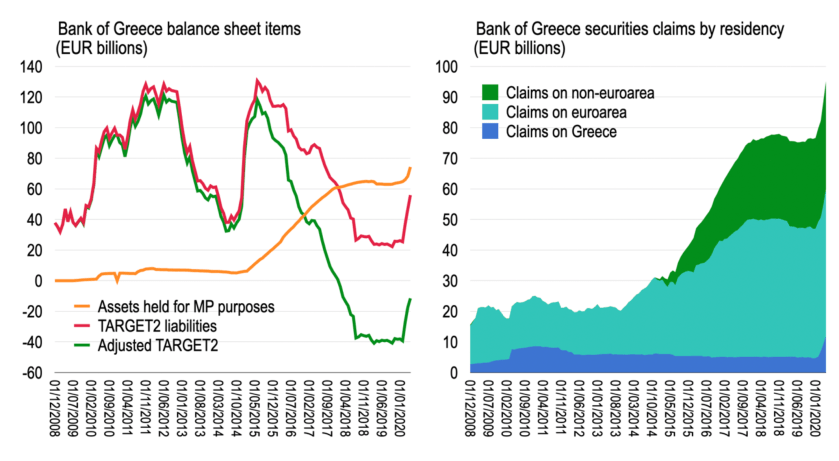

But what’s going on with Greek TARGET2 more generally? That’s a fun one. For the first time the Bank of Greece has been able to buy domestic government debt as part of PEPP. However, as under previous APP purchases, Greece is also buying non-Greek assets. To be sure, this meant that from 2015, BOG assets held for monetary policy purposes increased to over EUR60BN without buying any domestic Greek securities. These purchases mechanically increase the Greek TARGET2 debit as counterpart to these asset purchases. This was while the Greek TARGET2 debit was mechanically falling on capital inflows and resident repatriation of funds stashed abroad. We can produce an “adjusted” TARGET2 debit for Greece, and this turned negative on capital inflows in late-2017—meaning Greece has been running a “shadow” TARGET2 credit for the last 4 years.

The distribution of BOG assets by geography is shown below. There was an increase in non-Greece euroarea and non-euroarea non-resident securities. The non-euroarea securities looks like a puzzle, but EU entities like EIB, ESM, etc. are non-euroarea by domicile (I think.)

Most importantly, in the past 4 months BOG has been buying domestic securities. Indeed, between February and end-May Greek securities increased EUR6.9BN according to BOG accounting. The PEPP purchase data last week, meanwhile, reveals that purchases of Greek debt securities of EUR9.9BN happened through end-July.

There is something interesting to note on the change in Greek TARGET2 debit through end-May. Whereas the assets held for monetary policy purposes increased EUR9.6BN, the TARGET2 debit increased EUR30.5BN. How is this possible? Because Greek banks accessed EUR20.5BN in LTROs over this period, meaning all of the liquidity created through these two sources were associated with the accumulation of (net) foreign claims in the first 3 months of the Crisis. It might be that banks were repaying external finding lines or buying GGBs from non-residents.

In any case, this brings us back to debt management and the balance of payments. Government deposits have not been drawn down substantially since the Crisis began, so they still have a buffer for financing the fiscal deficit and de facto the current account deficit. But should they run down these deposits for this purpose? Or should they increase issuance at long maturities to provide room for PEPP to be used in full? Moreover, should they make full use of the loans available under RRF? This depends on the maturity structure of these facilities, which remains unclear. But keeping a large buffer of government deposits by using these facilities would seem to make a lot of sense, including because it helps sustain market access.

This then raises concerns about the fiscal rules, of course. Such asset-liability management exercises have no place in the EU fiscal rules, which focus on gross debt and ignore financial assets. And since Greece needs a stock of financial assets to support the balance of payments, any criticism for growing debt for this reason should be resisted.

Finally, there is a dilemma in the use of the RFF in terms of both grants and loans. 3-4 years of net transfers and loans of, say, 4% of GDP is important balance of payments support on top of the steady drip from the EU Budget. But this will become a challenge if this again displaces Greek resources towards non-traded production such that, once withdrawn, there is an external transfer problem once more. So managing net transfers on this scale, which will be withdrawn quite quickly, argues for careful spending but not necessarily absorption of these funds.

All of which, I think, argues for continued accumulation of government deposits at the Bank of Greece in lieu of reserve assets and monetary policy in an incomplete monetary union. Debt management is macroeconomic management in Greece.

END.