Amongst several others, Bolivia recently requested and received 100% of quota purchase—that is, “loan”—from the IMF’s Rapid Financing Instrument* (RFI) to provide budget support in the aftermath of the COVID-19 Crisis. This is about SDR240 million—USD327 million (0.8% of GDP)—due to be repurchased between 2023 and 2025. With interest payments of about USD3½ million per year (around 1% rate) this is an important source of financial support at an exceptional time.

Glancing through the Staff Report, a number of observations stand out.

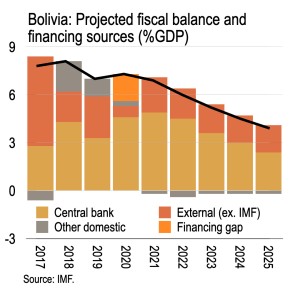

First, Bolivia’s fiscal situation was already stretched prior to COVID-19, with the government’s overall balance averaging 7½% of GDP between 2017 and 2019. Not only is this a high structural deficit entering the Crisis, but the financing was dangerous. While nearly ¾ of the deficit was financed externally in 2017 and ¼ by the central bank, in 2018 and 2019 about half the deficit was financed by the central bank (BCB). Moreover, this is not only backward looking. Over the forecast horizon provided by the IMF, nearly 70% of the deficits over the next 6 years (including 2020) will be financed by BCB. This is USD11bn in financing over 6 years out of an economy of about USD42bn—say 25% of GDP.

Second, related to this, BCB’s balance sheet bears witness to this financing largesse. Net credit to the government is set to increase from BOP20.2bn end-2019 through BOP96.2bn at end-2025—or, from 7% to 24% of (projected) GDP in 6 years, or from 26% to 85% of base money. While central bank claims increase BOP76bn, base money only expands BOP37bn—meaning there is BOP39bn in central bank credit created over-and-above growing demand for base money, or about USD6bn.

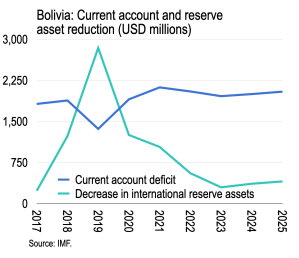

Third, this leads us naturally to the balance of payments. The current account deficit is projected to remain around USD2bn per year, while the central bank is expected to draw down international reserves cumulating to USD3.9bn over the period—de facto financing roughly one-third of the deficit over the period.

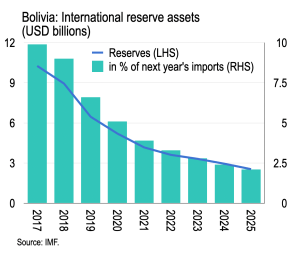

Fourth, as a result BCB gross international reserves are set to decrease from USD9½bn end-2017 to 2½bn end-2025—or from nearly 10 months of imports to only 2.1 months. It is difficult to see how Bolivia can be considered to have adequate capacity to repay the Fund in 2023-25 (¶15) when reserves are so slender and the exchange rate is fixed.

Now, the Staff Report notes that while “temporary recourse to central bank funding to cover a portion of the deficit is warranted by the immediate medical, humanitarian, and economic needs prompted by the crisis… Over the medium term, the authorities intend to ensure convergence to a sustainable fiscal position, without central bank financing of the fiscal deficit.” However, while arguing against central bank financing and in favour of fiscal adjustment, the detail of the report reveals continued central bank financing, loss of gross international reserves, and an unsustainable fiscal-financial program.

It is understandable that the imperative to engage with and support members at a time of COVID-19 involves IMF support with few strings attached. But the Bolivia case seems to reveal the danger of unconditional IMF lending—as countries with an initially unsustainable policy mix take advantage of the RFI. Clearly Bolivia will have to engage with a full Fund program in the next few years regardless of COVID-19. This raises numerous questions about the RFI. Is it better to provide 100% of quota with no strings attached now—to build bridges—and then engage in a full program later? Maybe, but there is a danger in this case that necessary adjustment outside the challenge of COVID-19 is delayed. Moreover, the RFI rubric claims that “Prior actions may be required where warranted.” It’s difficult to understand why some prior actions were not required in this case—perhaps re-iterating central bank independence or initiating some review of fiscal expenditure as a stronger commitment to future adjustment.

While Brad Setser has persuasively argued in favour of expanding the available financing under RFI, one argument against expanding these funds seems to be the danger of abuse in previously unsustainable cases such as this—absent some higher bar for unconditional access. That said, the RFI is still preferable to authorities’ under-the-radar use of an SDR allocation, since at least there is a Fund document involved and available for study.

END.

* The IMF’s RFI “provides rapid and low-access financial assistance to member countries facing an urgent balance of payments need, without the need to have a full-fledged program in place.” It “is designed for situations where a full-fledged economic program is either not necessary nor feasible… Financial assistance … [is provided] without the need for a full-fledged program or reviews. A member … is required to cooperate with the IMF to make efforts to solve its balance of payments difficulties and to describe the general economic policies that it proposes to follow. Prior actions may be required where warranted.” RFI access limits were recently doubled to 100% of quota per year, with 150% cumulative limit.

There is no shortage of unsustainable policy combinations in the recent RFI/RCF exercises. The language on Ghana, for example, is quite frank. It is not obvious that it is a big problem for countries to be running big fiscal deficits faced with the COVID shock, finance it through money creation, and sterilize through reserve drawdown. Window-dressing the projections to show everything works out in the end would be possible, but not a help to anyone. So I don’t have much of a problem with the Bolivia exercise.

Where I have a problem is in the $3 billion Nigeria loan. The Staff Report shows the fiscal gap much reduced by “bank financing”. One only learns in the appended tables that this is CENTRAL bank financing, that base money is set to rise by 70% in 2020 DESPITE sterilization through international reserve drawdown…but this has no impact on broad money, or inflation, whatsoever. The money multiplier is just assumed to plummet. Meanwhile, “Staff supports the central bank’s caution in easing monetary policy”. Excuse me?

LikeLike

Agree Nigeria is a problem, I was looking at that also. The central bank balance sheet reveals major challenges ahead. However, I don’t see a huge difference between Nigeria and Bolivia in that they both rely on central bank financing which artificially improves debt sustainability — both look like devaluation candidates and full program countries.

LikeLike