The tenth anniversary of the Troika’s intervention in Greece passed barely noticed amidst the COVID-19 tragedy. It was May 2010 when the Greek program was agreed—initially for EUR110bn, including financing from the IMF and EU. The occasion ought not pass without comment, however. In fact, today’s Coronavirus challenge demands an honest reflection upon failings past. The international monetary system is creaking under the virus, and a thoughtful response by the international community is needed to avoid unnecessary damage. We cannot afford politically-influenced rather than analytically-driven responses. To this end, casting a critical eye on the work of the IMF is more important than ever before.

This blog recently lamented the myth of IMF macroeconomics—the systematic failings of the IMF, the lies and associated cover ups—and noted that the Fund produced a financial program for Greece that didn’t add up with consequences great. At the same time, the post did not explain precisely how the program did not add up, only to note that Polak’s “slow road of iteration” was not walked—that this was no traditional financial program. Several interlocutors have since suggested privately that more information on this might be useful—otherwise the Fund retains deniability. After all, how can we be sure this is true?

We walk here through some of the errors in the IMF programs in Greece, recalling those failings that drove a country on the Mediterranean into depression a decade ago, providing a practical example of how the IMF financial programming framework was abused—whereas, were it understood and applied, could have served to support rather than crucify the Greeks.

Stylized financial programming

So why exactly did the Greece program fail? We need a short technical digression.

While focus usually falls on the fiscal accounts, the IMF’s financial programming (FP) approach involves building a consistent set of accounts for all sectors of the economy. Let’s build a stylized set of accounts that illustrates the FP approach and then turn to the program documents.

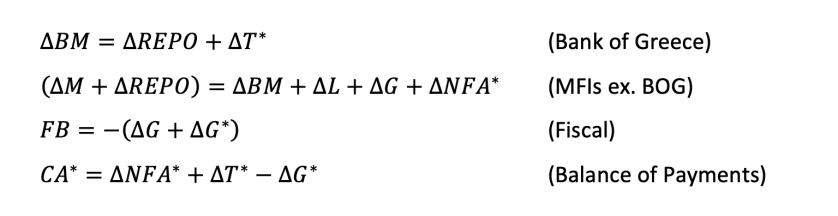

Consider four sectors with four flow constraints:

For the Bank of Greece (BOG) the change in base money (delta BM) is equal to the change in repos by banks (delta REPO) plus change in net TARGET2 (delta T*). Here the asterisk denotes variables against non-residents from the balance of payments. For banks excluding the BOG (MFIs) the change in broad money and repos (delta M plus delta REPO) on the liabilities side is equal to the change in base money plus change in loans to the private sector (delta L) plus change in lending to government (delta G) plus change in net foreign assets (delta NFA*). The fiscal balance (FB) is financed by increasing debt to banks or non-residents (delta G*). Finally, the balance of payments (BOP) summarizes the consolidated economy change in financial claims on rest of the world which must equal the current account (CA*).

For the Bank of Greece (BOG) the change in base money (delta BM) is equal to the change in repos by banks (delta REPO) plus change in net TARGET2 (delta T*). Here the asterisk denotes variables against non-residents from the balance of payments. For banks excluding the BOG (MFIs) the change in broad money and repos (delta M plus delta REPO) on the liabilities side is equal to the change in base money plus change in loans to the private sector (delta L) plus change in lending to government (delta G) plus change in net foreign assets (delta NFA*). The fiscal balance (FB) is financed by increasing debt to banks or non-residents (delta G*). Finally, the balance of payments (BOP) summarizes the consolidated economy change in financial claims on rest of the world which must equal the current account (CA*).

These are simply accounting constraints, so there’s nothing special going on here.

Add the first two constraints, you get what’s commonly regarded as the monetary survey, which Polak used as a cornerstone of his analysis:

Here, the claims between private banks and BOG cancel in the consolidation process but are important and revealed by projecting the BOG balance sheet separately. The change in broad money is equal to bank lending to the private sector plus credit to the government, plus the change in net foreign assets of private banks and BOG. Here is the idea that the broad measure of “money” in any economy is endogenous and can be of external or domestic origin.

Add the fiscal accounts, rearrange and compare with the balance of payments, and we get three equalities:

These are the fundamental constraints on any program, which we need not repeat below but that ought to be kept in mind in what follows: the current account—external non-financial transactions such as exports minus imports plus net factor income and transfers, the capacity to earn foreign exchange—must equal the fiscal balance plus bank net claims on the private sector—meaning the change in broad money net of loans—which must in turn equal the change in net foreign assets of the banking system and government.

These are the fundamental constraints on any program, which we need not repeat below but that ought to be kept in mind in what follows: the current account—external non-financial transactions such as exports minus imports plus net factor income and transfers, the capacity to earn foreign exchange—must equal the fiscal balance plus bank net claims on the private sector—meaning the change in broad money net of loans—which must in turn equal the change in net foreign assets of the banking system and government.

Each sector of the economy is analysed in isolation, including those parts that fall out of the consolidation. But the FP iterative process brings sectors into alignment to ensure, say, fiscal policy is consistent with the tendencies of the banking system, the availability of external financial resources, the central bank’s net reserve position (here TARGET2) and the capacity to generate exports over imports. We can “see” how a fiscal deficit might be associated with current account deficit (if FB < 0 and CA < 0) in the famous “twin deficits” sense.

In order to understand macroeconomic outcomes—which always find expression in one form or other in the balance of payments—iterative consistency of the sector accounts is necessary if unspoken.

The evolution of the Greek program

Despite the myth of IMF macroeconomics, the Fund was ill-prepared for the euroarea crisis when it emerged in 2010. Consider the Greece Article IV document from mid-2009, which postulated the Greek current account deficit would cumulate to about 46% of GDP through 2014, did not include a monetary survey or Bank of Greece balance sheet, and which provided only superficial analysis of the financing of the general government or current account. The IMF’s intellectual tradition was not on show!

On the other hand, the document does confess that the Greek real effective exchange rate was thought 20-30% overvalued. Despite this, real GDP growth would hardly contract before increasing towards 1.8% per year by 2014, and HICP inflation reach 2% once more by 2013. Nominal GDP growth would march ever upwards—not to be compromised despite the external imbalances and lack of monetary analysis.

This is, of course, nothing more than boilerplate nonsense of limited value. Staff were no longer literate in their financial programming heritage.

Less than a year later, the crisis had begun. And in May the IMF program was passed by the Board as a basis for the Troika agreement. Consider then the three crucial assumptions that underpinned this so-called “program,” bearing in mind the fundamental constraints above, as designed in 2010.

First, the Greeks were expected to undertake fiscal consolidation of 11½ percent of GDP—delivered at great domestic cost.

Second, offsetting most of this homegrown contraction, an improvement in net exports of nearly 10 percent of GDP was assumed—requiring Greek exports of goods and services to increase from 18 percent of GDP to 28 percent in only six years. How was this achieved? Nominal exports would expand 65 percent through 2015, imports only 5 percent—all without the “expenditure switching” exchange rate channel.

To put this in context, against a far more precipitous external environment, Germany’s peak expansion of nominal exports in the mid-2000s was 56 percent; their goods and service balance improved by 5 percentage points of GDP. At this time China, the rising export-led star in Asia, enjoyed an improvement in goods and service balance of about 6½ percentage points of GDP—facilitated by what was commonly regarded as an undervalued real exchange rate. In 2010, Greece was thought to have a real exchange rate that was about 25 percent overvalued. And from this difficult starting point—absent recourse to exchange rate depreciation—Greece was expected under the program to achieve a 10 percentage points of GDP improvement in goods and service balance without compressing imports. So the program required Greece to outperform the German and Chinese export “miracles” of the 2000s!

The third assumption through which Greek external adjustment was further ameliorated in the original program was in terms of interest paid to non-residents. That is, general government interest expenditure was set to increase from 5% of GDP in 2009 to 8.1% in 2015 (IMF, SM/10/110, p.13) due to more expensive program loans replacing private debt. This more than 3% of GDP deterioration in the interest costs should have shown up in the income account on the current account projection, as most public and all official debt was to non-residents. But the programmed external balance on factor income was instead forecast to only deteriorate ½ percent of GDP. In this way, onerous interest costs imposed under the program were simply assumed away in the external accounts.

Taken together, the export and interest assumptions upon program initiation postulated, without justification, that Greece was able to generate substantial external income—of more than €30 billion per year by 2015, or roughly 13% of initial GDP—to replace fiscal compression and shoulder the burden of growing burden of external debt.

This is crucial because normally a fiscal withdrawal of such magnitude would show up through a compression of imports (see the above fundamental relations), which would in basic macro-accounting imply lower nominal GDP and worsening debt dynamics. This sleight-of-hand, suggesting exports could replace private income due to austerity, side-stepped the challenge of meaningful debt sustainability analysis.

However, in contrast to the fiscal consolidation at home, the people of Greece had little control over demand conditions elsewhere that were crucial for the program to succeed.

Was there any effort to ensure consistent global demand with these program assumptions? By 2011 the ECB undertook to tighten monetary conditions and—with full support of the Troika institutions—it was agreed across Europe to undertake a coordinated fiscal consolidation. This in itself was a violation of the assumptions implied in the Greek program. The net result was a contraction in domestic demand across the Eurozone—exactly the opposite of what was needed for the Greece program to succeed. And so, while the Greeks kept their side of the bargain—an unprecedented fiscal consolidation—the Europeans fell short of theirs—failing to deliver the symmetric adjustment on which the program hinged. No surprise was it when export growth assumptions for Greece were slashed in half within 2 years!

In short, was the original Greece program built on a reasonable macro-financial framework? Or was it, as Michael Mussa once described the IMF’s involvement in Argentina, “advocacy analysis that endeavors to support a precooked conclusion favored by a country’s authorities and Fund management?” The answer, surprisingly, is even implicitly contained in the original Greece program document (10/110, ¶11): “Given the relatively closed economy, fiscal multipliers are bound to be large and the foreign sector too small to bring about a quick export-led growth response.” While in one breath the IMF was projecting small fiscal multipliers and rapid export-led recovery, in the next the Fund was warning of deep flaws in the very projections on which the future of the Greek people—and indeed Europe—hinged.

***

Although the original program was doomed to fail, the international community spent the next 12 months and more doubling down on this gamble. But things began relatively well. At the time of the First Review the authorities were offered strong support: “The [Greek] program … made a strong start.” Public debt-to-GDP in 2015 was even revised down from 139 percent to 134 percent—though only thanks to a transposition error in the nominal GDP path (see IMF, SM/10/286).

But beneath the spin, the reality of fiscal consolidation was taking hold in Greece. The private sector scrambled to replace income lost from fiscal consolidation. Throughout late-2010 and early-2011, households and businesses engaged overdrafts from the banking system, turning the credit impulse—the change in the flow of credit—as well as credit growth itself positive. Broad money meanwhile contracted—partly to convert into cash or transfer abroad, but also to sustain current spending. This meant the real economy weathered the initial stages of fiscal contraction. But with private financing of the banking system unavailable, it meant the Greek banking system was becoming ever more reliant on European Central Bank (ECB) funding through the Bank of Greece. Over the first full year of the program, Greek liabilities to the Eurosystem (the so-called TARGET2 balance) increased an additional €20 billion—from €84 billion end-May 2010 to reach €104 billion.

By early 2011, against the backdrop of this growing Eurosystem exposure, a plan was hatched to wean the banking system off this exceptional support—eliminating the only remaining safety valve for the Greek economy. And so, though not a feature of the original program, it was decided BOG liquidity to the banking system would only be provided in exchange for “the adoption by banks of credible medium-term funding plans and subsequent satisfactory implementation” (IMF, SM/11/68, ¶22). The Bank of Greece “asked banks to devise and implement [such] plans…” and the IMF prepared “a top-down program forecast for the banking system…” to program the return liquidity to the ECB (IMF, SM/11/68, ¶23 see also Box 2, p.25).

Now, let’s recall how the IMF had stopped many years before undertaking standard monetary analysis for Greece as elsewhere—the typical Monetary Survey approach that Polak borrowed from Robert Triffin. This didn’t change once the Troika was initiated. Consider how the May 2010 program document which included (p.34) a farcical monetary survey and no Bank of Greece balance sheet. The “monetary survey” was not even divided into Polak’s analytical device of building broad money into the sum of net foreign and domestic assets (balance of payments concept). The closest we get to the concept of money is “total deposits” with no distinction between sight, time, or non-resident contributions. And in any case, the projection was only through end-2010.

Back to early-2011, and the 3rd Review. There had been evolution—of sorts. What was the Monetary Survey had become the “Aggregated Balance Sheet of Monetary Financial Institutions excluding the Bank of Greece” (p.54.) The problem is, this new-fangled monetary analysis completely overturned the IMF’s traditional approach of dividing broad money into domestic and external origins. There was no corresponding Bank of Greece balance sheet, and there was no way of cross-checking this with the balance of payments.

The iterative process is dead. Long live the pretence of the iterative process! Upon this ramshackle monetary structure was the rationale for the withdrawal of credit to the Greek private sector built—just so the ECB could get repaid!

According to the plans drawn up at that time, banks’ aggregate liabilities to the Bank of Greece—and therefore Greek “TARGET2 liabilities” to the Eurosystem—were set to fall €82 billion, or nearly 40% of GDP, by end-2015. How exactly was this repayment to be achieved? The IMF’s new-but-irregular monetary accounts posited an offsetting increase in deposits by the Greek non-financial private sector of €85 billion over the period (see line “Deposits and repos of non-MFIs” and note that “other countries” make a negative contribution to this increase.)

Now, let’s return to our fundamental accounting constraints. There are roughly two ways the Greek private sector could increase their net claims on the banking sector under such circumstances to be consistent with other sectors: first, though highly unlikely, through substantial capital inflows or borrowing from aboard to fund deposits; second, by increasing net exports and depositing the proceeds with the banking system. But a massive increase in net exports already formed the backbone of the original program adjustment! Implicitly, the private sector in Greece was now being asked to find a further €16 billion per year from abroad to repay the ECB—on top of the original €30 billion per year by 2015 under the initial program needed to sustain spending in the economy.

And so, in 2011 targets for bank deleveraging were folded upon the largest fiscal consolidation in history. A credit crunch folded upon to fiscal nightmare. And although the people of Greece could not possibly deliver on these targets, they had no means of drawing upon such euros from abroad, the international community continued to pretend the Troika institutions were engaged in the meaningful construction and implementation of a structural adjustment program—all the while extending the window during which Greece’s private creditors were being unnecessarily repaid.

From day one, the Greece “program” was no such thing—it was not a program in the traditional IMF sense of a consistent set of macro-financial flows, based on reasonable assumptions, and subject to rigorous crosschecks on sector balances and adding-up constraints. It was just a series of political compromises hidden beneath the veneer of sophistication offered by the glossy program documents served up by Troika institutions. To paraphrase Keynes, the “program” might as well have assumed the people of Greece could call upon euros from the moon!

***

The Greek adjustment “designed” in May 2010 was absolutely impossible to achieve. Whatever the failings of Greek society until that point, imposing such an impossible adjustment could only cause untold misery and havoc. The so-called program did not pass even the most basic smell checks of internal or global consistency.

Of course, it is important that this was a Greek failure and not of the international financial architecture. And in 2013 the International Monetary Fund’s (IMF) so-called Mea Culpa on the Greek program ensured that creditors could point the finger of blame at Athens: “The high adjustment cost [under the program] reflects in important part the delayed, hesitant and piecemeal implementation of structural reforms” (IMF, SM/13/241, ¶3).

In other words: it had nothing to do with our macroeconomic incompetence. Such scapegoating is not only disingenuous, but serves to prevent meaningful lessons being drawn for future programs.

Subsequent lies and cover up

There are only two pathways forward from the production of such flawed analysis. The first is to double down, to deny any responsibility and blame others—especially the Greeks. The second would be to acknowledge the IMF was asleep at the wheel and failed to deliver on the promise to bring “program expertise” to Greece and the rest of the euroarea crisis with a view to preventing it happening again. The latter, akin to some “truth and reconciliation” within the Fund, would help prevent a repeat of such mistakes in the future. The former would be a better career move for those involved. And so, the cover up.

Mission Chief Poul Thomsen has since spun the Greece intervention on numerous occasions to deny personal or institutional responsibility. Here are three examples; there are no doubt many, many more:

First, in a press conference at the IMF Spring Meetings in April 2012 Thomsen claimed that “The Fund obviously has program expertise and an expertise of dealing with crises, an expertise in seeing how those things add up and fit together…” If he had read the documents he was defending, and understood the basics of IMF macroeconomics, he would have understood this to be a lie. There was no “adding up,” just the illusion that the IMF delivered this technology to serve political goals of those in Europe.

Second, Thomsen was challenged (46 min onwards) at the London School of Economics in October 2019 by Kevin Featherstone, Professor of Hellenic Studies, about the fact that the IMF was setting arbitrary program targets without any rationalisation. Featherstone referenced the need to shed 150,000 public sector posts in a short period (from a total population of about 11 million) and suggests this is something Thomsen himself insisted upon. Featherstone is rightly stoic about this serious point, how this was not arrived at on the basis of analytical work and delegitimises structural reforms. Thomsen’s response ran as follows: “I will dispute the facts…. [when pressed on what happened rather than intention] … the numbers were dramatically less, 15,000 or less. I don’t agree with the number of 150[,000], it was much less than that and it did not happen.]” But Featherstone was hardly riffing it. He had done his homework and was right to challenge the point. One only needs to consult the January 2013 IMF Review Document to uncover the commitment by the authorities to “reduce the public sector workforce by 150,000 by 2015, relative to the end-2010 level” (p.185). Whether this is implemented or not, and whether it made sense or not, is not the point. It was a genuine requirement of the IMF.

Third, when presenting at St. Anthony’s College Oxford Thomsen claimed that the fiscal multipliers for Greece were taken from the OECD. (See from 17:40, note the sip of water after this claim as a “tell.”) Indeed, “Yes, I think we under-estimated the fiscal multipliers, we took the OECD multipliers and I think they are too small [sip of water] no doubt about that…” So, suddenly it’s the OECD’s fault. But there was no prior reference to the OECD. Where did this come from? Blatant and psychopathic lies!

How is any of this acceptable? In what world do we live where the IMF can engage in an Enron-style accounting fraud, but the world turns a blind eye and instead agrees to blame the recipients of what Varoufakis has rightly described as fiscal waterboarding? Of course, there were accounting irregularities committed by the authorities in Greece. But the accounting irregularities and fraud committed by the IMF in the course of the crucifixion of the Greeks were arguably worse—after all, the Greeks only put private investors’ money at risk, the IMF has been blissfully and incompetently playing with public money.

The most frightening thought of all runs as follows. The European institutions were supposedly learning from the IMF during the Crisis in Europe so that they might take on this role without Fund support in the future. But the Fund was engaged in fraud, and one suspects the penny hasn’t dropped. So in the event the ESM is called to action any time soon, we will have to face another set of analytically inconsistent and economically incompetent documents—with zero concern for the commitments at Bretton Woods.

END.

2 thoughts on “The IMF and the crucifixion of the Greeks”