YOU CAN change the mission chief, but you can’t stop the bullshit. That ought to be the IMF’s motto.

While numerous crucial macro variables of concern for international investors have been purposefully suppressed in the IMF’s WEO database relating to Argentina, presumably to spare various blushes, there is enough there for us to smell the nonsense that the international monetary system—whatever that is—will be expected to swallow in the next 3 months as a new program is negotiated.

And so, as The Who put some time ago it: Meet the new boss, the same as the old boss.

First, what’s missing? Well, there is no data related to public finances—in particular the debt stock and primary balance. So, the Fund remains coy on the fiscal path or other crucial variables. But the remaining information is enough to reveal the poverty of their analysis.

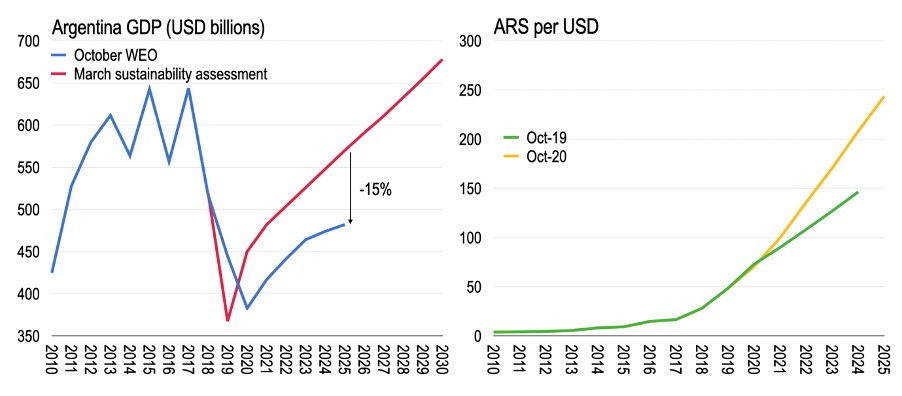

Second, what’s new? Well, the Fund has changed tack substantially since the March “technical assistance” sustainability document when the path of nominal GDP in dollar terms was expected to make a heady recovery. Indeed, then the USD value of GDP was expected to return quickly to levels achieved at after the recent overvaluation. But GDP in USD terms by 2025 is now about 15% below the level expected then, USD482BN being much closer to the authorities’ projection during the debt negotiation of USD488BN. Or, previous dollar GDP ebullience has given way to something more measured after undermining the authorities’ negotiating position.

At the same time, the Fund’s implicit year-average nominal exchange rate suggests a loss of monetary control greater than previously imagined, whereby the year average exchange rate is now expected to reach nearly ARSUSD250 by 2025. Whereas nominal depreciation of 67% between 2019 and 2024 was expected a year ago, now 77% is expected. This doesn’t sound much, but in terms of the number of Pesos that can be purchased per dollar in 2024 this is a substantial gap on the projection only a year ago.

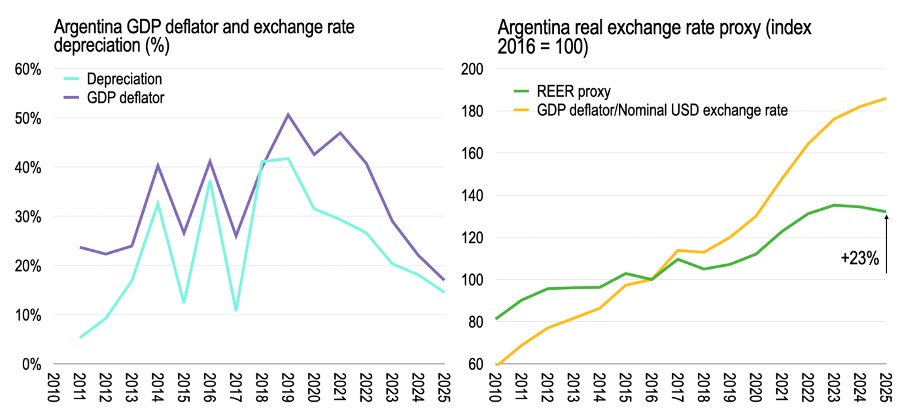

Third, and more worrying, what stinks? Well, wouldn’t the above nominal exchange rate path be associated with substantial inflation. Indeed. The chart below shows the rate of depreciation (year average) against the percent change in the GDP deflator. And what we see is a large gap opening up in terms of the rate of growth of the GDP deflator in coming years—which is normally only slightly above the and the rate of depreciation of the exchange rate. Now, I have no idea what the inflation rate of Argentina’s trading partners is for the purposes is calculating the real exchange rate. But below we assume the real exchange rate is a geometric weighted average of the GDP deflator in Brazil and 4% inflation rate for other trading partners with a weight of 50% each. As a rule of thumb, this is probably not too far off. I hope.

Anyway, while only a naïve proxy, the acceleration of domestic inflation ahead of the rate of depreciation of the exchange rate suggests an excess reliance on unlikely GDP deflator inflation to generate debt sustainability—not for the first time. Were this thought of in terms of the real exchange rate, then the relative price of domestic non-traded goods would reach an all-time high, in the next few years—while the current account surplus, which reaches +1.2% of GDP in 2021 falls off only to +0.6% in 2025.

This is a useful hook for blagging debt sustainability, of course. So long as projected domestic prices race ahead of the rate of exchange rate depreciation (increasing the value of predominantly dollar denominated debt) there is a chance of projecting “sustainability.” But only on paper, of course. Hence the Argentina team has revealed their hand into the program negotiation in November. But any serious analysis will dismiss this as no better than the gobshite that we have been expected to swallow for the past 3 years already.

Let’s be absolutely honest about this. The IMF can’t be bothered checking whether their work makes sense. They are taking the piss.

Hence nothing has changed. Meet the new boss, the same as the old boss.

END.

One thought on “Argentina in the WEO: Hold your nose and look away. Again.”