PDF version with annex.

It’s fair to say that the macroeconomic stabilization of Argentina, first during the Macri administration, including on the IMF’s watch, and now under President Fernandez, has failed.

There have been many mistakes over many years on the way to this outcome—indeed, too many to recall here—as well as some bad luck. Rather than relive these mistakes, including the recent failure of the debt exchange to bring about macro-financial stabilization, we might ask instead what policy options are now available. What policies should the authorities and international community pursue to stabilize the Argentine economy in a time of COVID?

In short: it’s time for a “Hail Mary” pass. And four features of the macroeconomic situation provide necessary background to this unlikely intervention.

First, the fiscal position. The primary fiscal balance continues to print substantial deficit, mostly monetized under the authorities plans. For example, in negotiations with creditors the authorities suggested the primary balance would print 3.1% deficit in 2020, 1.0% in 2021, and 0.5% in 2022 before finally balancing in 2023. These were pre-COVID assumptions carried through the negotiations, a substantial and unnecessary favour to creditors. The financing for these primary deficits was expected to be entirely due to BCRA monetization, minimizing the interest bill in yet another favour as to creditors.

More recently, the 2021 budget has been submitted with a 3.5% of GDP primary deficit, substantial slippage from the recent negotiation, with 60% financed by monetization.

Quite what the primary balance outcome for 2020 will be is not yet clear. But BCRA’s latest daily monetary report (9th October version) puts “temporary” advances and profit transfers from BCRA to the government so far at ARS1,735BN (ARS1,202BN being profit transfers.) What will be 2020 GDP? Let’s say USD400BN at an average exchange rate of ARS70 per USD for the year. That gives NGDP at ARS28TN making BCRA transfers year to date 6.2% of GDP. Since we are only ¾ of the way through the year, we might assume total central bank financing of around 8% of GDP, a reasonable estimate of the primary deficit assuming the cost of interest is being paid by new net borrowing as implied in discussions with creditors. Interest payments for the year are still not clear since the debt restructuring. But USD10BN (2.5% of GDP) is a conservative estimate relative to that expected at the early-2020 meaning the total fiscal deficit for 2020 could exceed 10% of GDP.

Of course, during the difficult COVID situation there is no implied criticism of the government’s fiscal response here—as opposed to the debt negotiation. Rather, our purpose is to understand how the situation can be stabilized to contribute to alleviating the health situation.

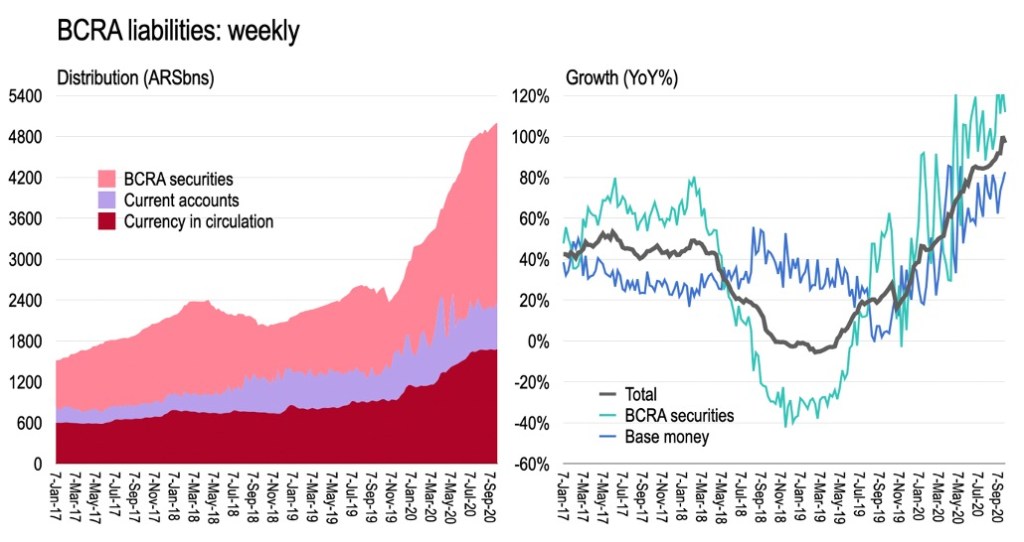

Second, BCRA’s monetary challenge. As noted on numerous occasions already (see here and here), as well as leaning on the central bank for budget financing, BCRA continues to issue sterilization instruments (LELIQs) at roughly 40% annualized interest.

The chart above shows the structure of key BRCA liabilities through end-September. Total liabilities defined as BCRA securities plus base money reached an important milestone on September 23rd when year-on-year growth touched 100%. Such liabilities are currently ARS5TN (perhaps 18% of GDP before being eroded by inflation) while more than half, or about ARS2.6TN, are one- and two-week liquidity absorbing LELIQs paying around 40% annualized return. A back of the envelope estimate based on the weekly outstanding stock of LELIQs so far this year suggests an interest bill of about ARS0.8TN for 2020 (nearly 3% of GDP.) And this doesn’t count the cost of overnight absorption.

Overall, the “true” consolidated government deficit could be 13% of GDP, plus or minus a few percentage points.

Since BCRA has no resources to pay for the cost of such monetary policy sterilization operations, they are ultimately forced to monetize this interest bill on top of the direct financing of the government. Hence the rapid expansion of overall liabilities and continuing pressure on the exchange rate to adjust further.

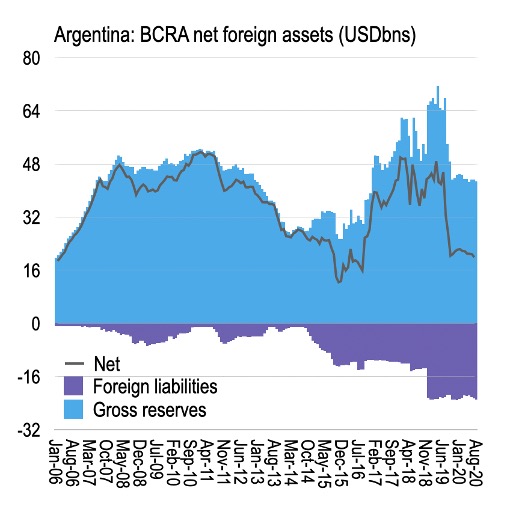

Of course, the asset side BCRA suffers from only a slender net external asset position, with gross international reserves around USD42BN, but foreign liabilities of about USD22BN, mainly due to PBOC swap lines. Indeed, using the BCRA monthly balance sheet, we can get a measure of net international reserves which are now around USD20BN. And while domestic currency liabilities continue to grow at a rapid clip, net foreign assets can only increase through exchange rate depreciation and upward valuation adjustment when measured in local currency.

Third, planned engagement with the IMF. The authorities’ plans during recent debt negotiations implicitly relied on new IMF purchases, within the program envelope, to capitalize interest and charges on Fund borrowing and push back eventual repurchases until perhaps 2027. This is not necessarily consistent with the lending arrangements available to the Fund. But that’s what they seem to have been relying on. For example, the authorities currently owe roughly USD44BN to the Fund repaid between 2021 and 2024. Interest and charges on this over the period will be, say, USD5BN. But if this were rolled over with interest added to the stock until 2027 then Argentina would cumulate about USD54BN in purchases from the Fund, within the USD57BN envelope previously promised to the Macri administration. This, at least, is what I understood to be the authorities position during recent negotiations. So, as well as delaying coupon payments to private external creditors until later this decade, the authorities would likewise need no new external resources to service the Fund until 2027.

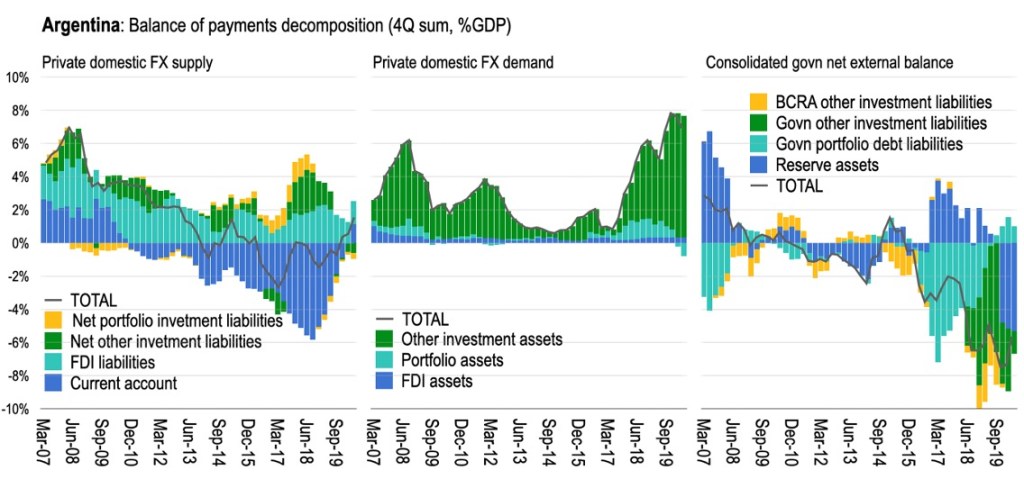

Fourth, the balance of payments. Most interesting, as so often the case, are the balance of payments flows. There are numerous ways to slice and dice the BOP, but one way is to think of the available supply of external (foreign exchange) assets relative to the private flow demand. The chart below decomposes the BOP accordingly. The left side is the private foreign exchange “supply”—or the sum of the current account plus private financial account inflows (liabilities.) The middle chart is the private domestic demand for foreign assets through the balance of payments. As of 2020Q2 the private sector in Argentina generated an external supply of foreign exchange for the first time since late-2014 as the current account turned to surplus (on a 4Q trailing sum basis) and there were modest FDI inflows. Foreign exchange available through this source was less than 2% of GDP. In terms of private demand for foreign exchange, however, this touched 8% of GDP in 2019 and was only slightly below this during the 12 months through June 2020.

The difference between private external asset demand and supply has to be provided by the consolidated government, of course—either by borrowing from abroad or by running down international reserve assets. This is what is shown in the right chart. The consolidated government has accessed foreign exchange in four waves since 2014 to support, first, the growing current account deficit and, more recently, private external asset demand. Initially this meant BRCA other investment liabilities, including swaps; next the government’s portfolio issuance binge; then IMF borrowing (government other investment liabilities) and more BCRA swap lines; and finally, most recently, the use of international reserves. The government has been accessing net external borrowing of about 6% of GDP since late-2017.

The difference between the private supply (2% of GDP) and demand (8%) for external assets is met by the consolidated government’s call on external resources, of course (6%). But since such external resources have nearly expired, something has to give.

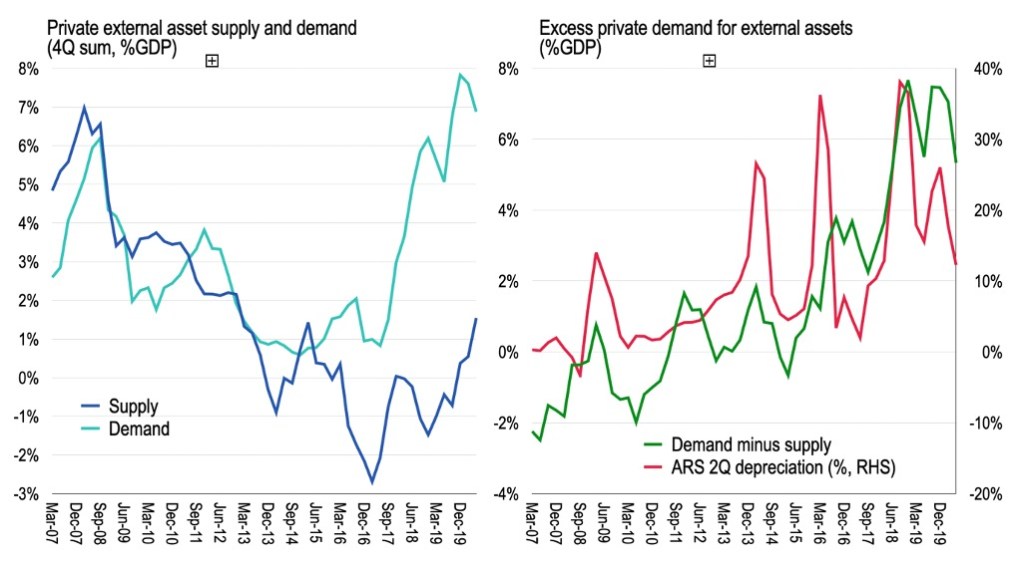

Indeed, this private supply and demand framework provides a useful way to frame pressure on ARS exchange rate. Each wave of excess private demand for foreign exchange, drawing on consolidated government external resources, is associated with a bout of exchange rate weakness (followed later by inflation, and an erosion of purchasing power.) The chart on the right above shows how the excess of demand over supply remains elevated. Meanwhile, though exchange rate depreciation appears to have moderated, the black-market exchange rate has gapped ever higher above the official rate reported here and is probably a truer reflection of asset flows.

So, what’s the “Hail Mary” pass?

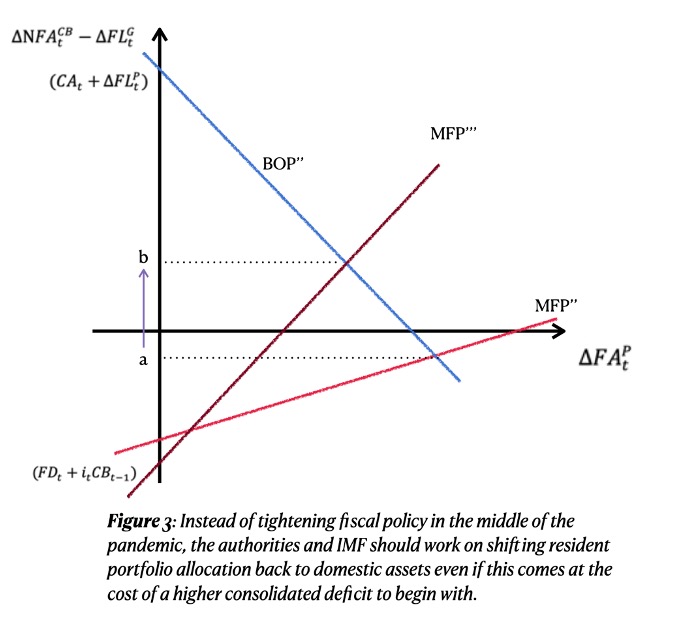

This leads us to the “Hail Mary” pass which the Argentine authorities, with support of the IMF, should implement. The technical annex attached provides a simple accounting framework for thinking through Argentina’s challenge, and a toy model based on one parameter—the portfolio allocation of the private saving-investment balance between domestic and external assets. The point is illustrated in Figure 3 in the annex, reproduced below. BOP’’ is the balance of payments relation, or the locus of points distributing the supply of foreign exchange due to the current account and private capital inflows between the consolidated government (y-axis) and private external asset accumulation (x-axis). This is the external constraint.

Meanwhile, MFP’’ is the locus of points along which the domestic monetary-fiscal-financial program is consistent with private portfolio asset accumulation. As drawn, the intersection of BOP’’ and MFP’’ below the x-axis implies a draw on consolidated government external resources to fulfil private portfolio demand for external assets given the domestic policy constellation. Note, the interest cost of central bank sterilization operations is included in the definition of government deficit here, meaning ignoring the quasi-fiscal cost of monetary actions is sterile. Figure 3 is simply an analytical representation of what is seen in the actual balance of payments data discussed above.

Now, the challenge facing Argentina is how to stem the domestic private demand for external assets given domestic policy settings. And this framework makes clear that the balance of payments challenge, and continued exchange rate weakness, is intimately linked to domestic monetary-fiscal policies. Indeed, they cannot be viewed in isolation as during the assessment of debt sustainability by each of the IMF, Argentine authorities, and private creditors.

For example, the consolidated government deficit is running currently at, say, 10% of GDP annualized (a conservative estimate). But domestic demand for external assets is about 8% of GDP, of which 2% is provided externally (generous, and let’s take this to be the sequential current account surplus). So, the private saving-investment balance is 12% of GDP (10% consolidated government deficit plus 2% of GDP current account surplus). Then there is roughly net 6% of GDP demand for external assets, which is 50% of the private saving-investment balance. So private sector allocates roughly 50% of their saving-investment balance in favour of external assets—which is anything other than the typical home bias in portfolio holdings, resulting from years of monetary madness in the Pampas.

One natural way to deal with this is to reduce the private saving-investment surplus by tightening fiscal policy. But in the middle of a pandemic this is not only irresponsible, it is also unnecessary. For what the chart above shows is that an alternative to tightening fiscal policy is to affect a change in private portfolio allocation away from external and towards domestic assets—that is, rotating MFP’’ anti-clockwise to MFP’’’ to stem the drain on official net external assets resulting from necessary fiscal largesse and allow for reserve accumulation. As drawn, this can be achieved while the consolidated government in fact runs a larger deficit (shifting down the intersection with the y-axis) due to an increase in the average interest paid on domestic liabilities.

In other words, Argentina can continue to run a consolidated government deficit commensurate with the health emergency. But she can only do so without precipitating a balance of payments crisis by changing resident portfolio asset allocation behaviour.

How can this be achieved? One way is through capital controls and moral suasion and the like, as currently deployed. The problem with this is that this will likely result in a negative real return given the policy framework and continued risk of exchange rate depreciation and inflation. So, it distorts market forces while failing to deliver.

A “Hail Mary” pass involves dealing with this problem directly and increasing the real return on domestic assets. Indeed, there are four legs to this policy wildcard.

- First, the government should pay the full cost of domestic monetary policy actions, including the cost of sterilization. To do this, recapitalizing BCRA with a domestic currency bond of about 10% of GDP with a 30% coupon would provide a strong signal. The face value of this instrument should increase in line with CPI for the next 10 years, so the real value of the interest income will not be lost to inflation and the commitment to monetary stability absolute.

- Second, in addition the government should make BCRA truly independent of fiscal encroachment by appointing a technocratic central bank governor for an 8-year term. The Governor should be appointment by a independent committee with some external representation and be entrusted to increase the stock of net international reserves from about 5% of GDP today to 15% of GDP over the next 8 years while bringing inflation sustainably below 10%.

- Third, the government finance the fiscal deficit without any reliance on monetary financing. In other words, the Federal government should rely on debt management that builds a yield curve with a positive real return for domestic investors through higher coupons, preferably in local currency but if necessary in foreign currency.

- Fourth, the authorities should request that the IMF augment the current program to total USD60BN, providing USD16BN in net funding over the next 18 months to support the fiscal deficit at a time of pandemic while helping stabilize the exchange rate.

While the government’s plan has apparently been to request the IMF provide financing needed to capitalize the interest on the program funds, this alternative approach would bring forward new funding to make net foreign exchange available to offset domestic external outflows.

Let’s try to put this in context. If the primary fiscal deficit in 2021 is indeed 3.5% of GDP, and the fiscal interest bill (post-BCRA recap) 4.5%, then the fiscal deficit in 2021 will be 8% of GDP. If the IMF provides USD16BN in new net funds through end-2021, that’s about 4% of GDP. So, the Fund would be providing funding for about half the deficit if needed. Of course, it might not be needed. With the authorities offering more generous real returns on domestic assets alongside a truly independent central bank dedicated to monetary stability, domestic financing should be plentiful given the structural current account surplus. Indeed, including expected lower coupons on foreign debt, external financing should now plentiful except in the case of a loss of resident confidence in domestic assets. If confidence can be restored, then the current account surplus—perhaps USD5BN per year or more—can be channelled into reserve accumulation and exchange rate stabilization.

Of course, this is truly a “Hail Mary” pass which is not guaranteed to succeed.

If it indeed fails, by late-2021 it will become clear that an additional external debt operation will be necessary which the IMF should fully support in the context of program negotiations to refinance outstanding Fund purchases. Until then, the IMF ought to support any serious effort to restore macro-financial sustainability during a global pandemic—especially given their past enthusiastic support for a Ponzi Program in Argentina that has become predictably unstuck.

END.