WHEN FRENCH POLICE searched the Paris home of then-International Monetary Fund (IMF) Managing Director Christine Lagarde in March 2013, an undated, handwritten pledge of allegiance from Lagarde to former President Nicolas Sarkozy was uncovered. Later leaked to the press, the letter—presumably written while he was still President—urged Sarkozy to “use me for as long as it suits you and suits your plans and casting call.”

The pretext for the raid on Lagarde’s home was, of course, the investigation into possible misuse of public funds—more than €400 million—in settling a claim on the state by Sarkozy-supporting, French businessman Bernard Tapie. Eventually, Lagarde was found “guilty of negligence in public office” for settling the case, but absent a sentence or formal criminal record from the finding by a special Paris court in December 2016, her position as IMF Managing Director was unthreatened.

When asked in court why she had not read detailed briefing that described the history of the Tapie case alongside a recommendation to rule out arbitration, Lagarde’s reply was that she “received between 8,000 to 9,000 notes per year.” In her overall defense, Lagarde implied she was not on top of her brief, was a mere pawn in the heady world of French politics, and was in any case happy to defer to her chief of staff on this decision—and likewise happy for him to take the blame in court.

What does this glimpse into the world of Madam Lagarde reveal about the person set to become the President of the European Central Bank (ECB)?

LAGARDE ARRIVED at the IMF in July 2011, about a year before the euroarea crisis peaked. Retrospectives on her contribution to the Fund will be cast in terms of charisma and statesmanship, as well as her contributions to the empowerment of women—it’s impossible to scan an IMF document today without stumbling upon measures to improve female labor force participation. However, an honest assessment of her tenure would recall those issues that most define her time at the Fund: austerity in the UK and Brexit; the Greek great depression; the Cyprus deposit insurance debacle; flawed euroarea oversight; and Argentina’s crisis renewed. There is a common denominator in all these cases—deeply flawed analysis driven by, or coupled with, politically-motivated decision-making. In all cases Lagarde was found out of her depth. In most cases, there appears to be a quid pro quo behind decisions. Her appointment to the ECB therefore represents a dangerous, perhaps seminal moment for the euroarea.

WHEN THE time came to nominate a new Managing Director in May 2011, it was not a euroarea member state making the case for Lagarde at the IMF. Rather, it was United Kingdom (UK) Chancellor of the Exchequer and austerity advocate George Osborne who formally nominated Lagarde in May 2011. And when Lagarde was up for a renewed term in 2016 it was Osborne again who quickly advanced re-nomination just months before the UK’s EU Referendum. Why was Lagarde’s candidacy so important to Osborne?

In 2010, as the coalition government in the UK had begun a policy of fiscal consolidation, the IMF under previous Managing Director Struss-Kahn had fallen under the austerity spell. The Fund produced saccharine analysis on the pros and cons of fiscal adjustment in that year’s Article IV consultation—the oversight of the UK economy conducted annually by the IMF. And the IMF was happy to conclude: “After weighing these different arguments [for and against austerity]… a significant fiscal tightening with frontloading in 2011/12 is appropriate to secure confidence in the UK’s debt sustainability” (Box 2, page 27.) This endorsement was exactly what Osborne needed; an IMF challenge to his strategy would be a tough pill to swallow. DSK’s unexpected departure could make the next annual health-check awkward, therefore—unless a suitable replacement could be found.

In throwing his weight behind Lagarde, Osborne was buying continued support for his policies—and would be able to call in any other favors along the way. Following her appointment as Managing Director, Madam Lagarde was duly on hand to add sparkle to the press conference at the end of the next Article IV visit in 2012, offering support to the “Chancellor, dear George.” The stomach turns.

The IMF’s endorsement of austerity in the UK thus continued despite hardships owing to the regressive nature of the adjustment including due to falling public investment—while continuing net inward migration diluted available public services. Moreover, as is now increasingly appreciated, austerity was not necessary at all—it was a political choice.

Spin ahead a few years, and Osborne had a bigger favor to ask. The decision to hold an EU Referendum in June 2016 required “objective” analysis that would point towards the benefits of Remain—Osborne’s position. In a series of clearly political interventions, the Fund’s Article IVconcluding statement in May 2016 was timed to coincide with the final month of the campaign; Lagarde was again on hand to deliver a carefully scripted message that led some to claim the IMF was “bullying” voters; while the publication of the Article IV report itself, just one week before the referendum, was surely timed to grab headlines and impact the vote.

Even if the IMF should to have strong views on these matters—and they should—delivery ought not be staged-managed for political favors. And the analysis itself should not be driven by political considerations. In any case, after the IMF’s wrong-headed support of austerity in the UK, why should anyone believe their analysis? The marginal voter in the EU Referendum, we might speculate, was likely most negatively impacted by the very same austerity the IMF was previously happy to endorse on Osborne’s behalf. Once bitten, twice shy. And when a prominent Leave campaigner suggested the UK public had “had enough of experts,” one wonders if the IMF was one of the targets. Only a few months later, the IMF was said to be “left shamefaced” over their flawed forecasts leading up to the EU Referendum.

THE FAILURE in Greece was a scandal on a different level, of course. The IMF was hardly a deciding factor in the EU Referendum in the United Kingdom. But the Fund was certainly central to the Greek great depression. And the program’s failure was assured before the ink on the document was dry. In short, the May 2010 adjustment assumed with no justification that Greek exports of goods and serviceswouldexpand65% through 2015 (imports would growonly5%)so exports as a share of GDP wouldincrease from 17.8% to 27.7% in six years. This 65% increase in nominal Greek exports over six years, necessary to offset domestic demand compression and retain the illusion of “debt sustainability,”would be achieved through both real exports and the price of the Greek export basket. That is, 39 percentage points of growth was penciled indue to real export growth (Staff Report 10/110, p.10), the remainder due to price increases—roughly a 3% per year average increase in the export price deflator over the period, despite so-called “internal devaluation.”

Moreover, although general government interest expenditure, mainly due to external debt,was expected toincrease from 5% of GDP in 2009 to projected 8.1% in 2015 (10/110, p.13), net interest in the external current account did not involve an equivalent deterioration.

It was later revealed by veteran IMF-watcher Paul Blustein that a memo from the Research Department before the Greece program was finalized correctly warned that the “program could still go off track (even with full policy compliance)” absent “strong export rebound.” So, some staff warned about the egregious assumptions—beyond the control of the Greek authorities—upon which the program hinged. But the program went ahead regardless.

Yet, taken together, the GDP and external factor income assumptions at the time of the initial program impliedthat, to sustain domestic demandand repay debt, the people of Greece wouldgenerate external income of more than €30 billion per year by 2015, or roughly 13% of initial GDP. This was against a backdrop of substantial, coordinated fiscal tightening across Europe—and growing risk of euroarea disintegration.

To simply assume the Greeks could magic euros from thin air was ridiculous—a scandal seldom been before seen in the history of official action in international monetary affairs except, perhaps, the German reparations imposition. Moreover, the attitude of official creditors was like that of a loan shark—repayment terms were impossible to meet, but if the Greeks failed to deliver they would be punished by ever-greater bullying and onerous impositions.

All this was pre-Lagarde-as-MD, of course—though coincident with her time as French Finance Minister. Upon appointment at the Fund, Lagarde faced a choice. She could have asserted the independence of mind to rethink the Greek situation—and defend the Greeks as Managing Director of the multilateral body inaugurated after the Second World War to lend to countries“by making the general resources of the Fund temporarily available … without resorting to measures destructive of national or international prosperity.” Or she could side with euroarea creditors against the Greeks. And she very publicly chose the latter.

To begin with, when debt restructuring was finally broached in late-2011 and 2012, the IMF capitulated to official creditors and allowed the ECB and national central banks (NCBs) to swap their €56½ billion holdings of Greek government bonds into new titles so they could be exempted from restructuring. This increased possible private sector losses in the restructuring—and later, the quasi-fiscal, thus unseen, transfers from taxpayers through lower interest costs. Doing do, it also reduced the potency of Eurosystem purchases—prior or prospective—in other countries. It hinted at greater private sector losses in future if needed, perhaps contributing to financial instability. It thus later became necessary to clarify that official holdings would be treated the same as private investors later under the ECB’s Asset Purchase Program (APP), underlining the sensitivity of the matter for investors. But when it came to Greece, narrow political constraints overwhelmed decisions needed for system wide stability and recovery of a very depressed economy. Given IMF support was necessary for continued Northern European involvement in the program, there was plenty of leverage to force a better deal for the Greeks.

The problem was, the Fund under Lagarde had chosen to demonize the Greeks rather than rethink the flawed macroeconomic logic that underpinned the so-called adjustment program. Indeed, even after the PSI operation, an investor visiting Athens in summer 2012 was not encouraged to be met by the IMF’s then-Resident Representative—and person responsible as desk economist for the original, incoherent program—explaining that “as long as this place is not burning to the ground, we’ll keep turning the screw,” a sentiment accompanied by a hand gesture to emphasize the point. This would hardly catalyze private investment! This was hardly the spirit of Fund lending without recourse to measures destructive of prosperity!

But the remark made perfect sense in the context of comments only a few months before, shortly after the flawed debt restructuring, when Lagarde herself explained to the Guardian that “she has more sympathy for children deprived of decent schooling in sub-Saharan Africa than for many of those facing poverty in Athens.” This attitude demonstrated a willingness to overlook entirely those analytical flaws in the original Greece program, as well as the IMF’s Purposes, to instead push a message from political masters in Europe. Indeed, this mirrored exactly the attitude later recalled by former Treasury Secretary Timothy Geithner, that the Europeans’ in early-2010 “we’re going to teach the Greeks a lesson.”

A braver, intellectually independent Managing Director would have noted the impossible assumptions upon which the original Greek program was based—and asserted the primacy of the IMF’s own mandate over that of European institutions. A more thoughtful leader would have taken a stand against the Northern European bullying and argued for stronger and more immediate debt relief.

WHEN GREEK debt restructuring finally arrived in 2012, several Cypriot banks were left overexposed, undercapitalized, and essentially bankrupt. By early-2013, a newly elected center-right President Nicos Anastasiades paved the way for a Troika program to restore financial stability after vacillating by his predecessor. By this time, however, the IMF’s involvement in euroarea lending programs had become increasingly controversial amongst non-EU members of the Executive Board. Moreover, unlike in the case of Ireland, there was now pressure from Core euroarea countries to bail-in the private sector to cover banking sector losses. Perhaps most important, Germany did not want to be seen to use taxpayer money to “bailout rich Russian depositors” as veteran IMF reporter Paul Blustein has explained. Indeed, as Blustein continued, German Finance Minister Wolfgang “Schauble insisted on limiting the size of the loan package to €10 billion; the remaining €7 billion [of financing] needed for the banks would have to come from their depositors and other Cypriot sources.” This is even though debt sustainability would have seen Cypriot public debt on a substantially more favorable trajectory than many other euroarea program countries. Crucially, Lagarde aligned once more with European creditors.

Regardless of the merits of the choice between bail-in and bail-out—and there is a case to be made that bail-in should not have been countenanced for financial stability reasons given public debt sustainability was not a major concern, — once that decision was taken what happened next should neverhave been allowed to happen. In short, the IMF’s initial proposal to bring sustainability to Cyprus involved losses for bondholders and large depositors—which would be transferred along with troubled assets to a “bad bank” and face losses of perhaps 40%. But the EU Commission was worried about the spillovers due to such large losses while the Cypriot authorities thought it might undermine their role as offshore financial center. Thus, the Commission, in the form of Olli Rehn, proposed a series of taxes on large-, medium-, and small deposits to fill the gap. The problem being, small deposits included those subject to deposit insurance.

Now, deposit insurance has been sacrosanct for financial stability since the Great Depression in the United States, when the Federal Deposit Insurance Corporation (FDIC) was inaugurated to stop bank runs and stabilize the banking system. Most countries developed their own deposit insurance schemes since, including across the euroarea where deposits under €100,000 were supposed to be insured. But in Brussels, as negotiations over Cyprus continued throughout the night—at the first key meeting chaired by recently appointed Eurogroup President, Jeromin Dijsselbloem—there was no-one apparently willing to speak up against breaking the deposit insurance taboo and associated implications for the rest of the euroarea. By the end of the night, under the strain of deadline, an agreement was reached which would tax deposits below €100,000 at 6.75%. The read-across to the rest of the euroarea was clear—all deposits were fair game to restore sustainability to the fiscal-financial sector. The risk of deposit flight was immediately elevated.

Fortunately, the Cypriot legislature refused to vote through the deal, and the damage was quickly undone. But this was a truly breathtaking failure of global macroeconomic policymaking. Blustein described it thus: “It was one of the starkest examples in financial-crisis history of how highly intelligent people can make decisions under pressure in the middle of the night that look appallingly unwise in the light of day.”

Put another way, it’s an example of how the blinkered objectives of interlocutors—each with their own narrow negotiating brief—can result in a dangerously suboptimal compromise with global implications. In this case, the IMF was more concerned about dotting the i’s and crossing the t’s in a pro formadebt sustainability exercise—which happened to justify the German need for a private bail-in—while reducing the IMF’s reputational risk by putting a lower proportion of the bail-out money forward. In the scrum to achieve these narrow negotiating objectives to please different constituencies, Lagarde took her eye off the big picture.

Any IMF Managing Director who allowed this to pass ought to have been sacked the next morning. But Lagarde could always blame the Europeans—or her staff; the Europeans could always blame the Cypriots; the Cypriots could blame the Greeks; the Greeks could blame financial market ebullience—and before you know it, no one is to blame.

Of course, this was not the first time Lagarde had been close to decisions that jolted financial markets over the course of the euroarea crisis. It is not clear what role Lagarde played in the background to the Deauville declaration in October 2010, while French Finance Minister. But it was in Deauville that Chancellor Merkel and President Sarkozy bilaterally agreed—that is, without consultation with other member states—that future bailouts would involve private sector haircuts, contributing to the intensification of the euroarea crisis. It’s difficult to imagine the two Finance Ministries were not involved.

THERE WERE in fact two periods of coordinated monetary-fiscal tightening in the euroarea over the period 2010-14, which left an imprint globally via the value of the euro. The first was intended, the second due to a bug in emergency monetary measures.

In 2011, under President Trichet, the ECB began tightening monetary policy, raising the main policy rate from 1% to 1.25% in April, and a further 0.25% to 1.5% in August—despite ongoing coordinated fiscal consolidation. And IMF staff were on hand in July, shortly after Lagarde’s arrival at the Fund, to support this egregious policy tightening. “The outlook calls for a gradual withdrawal of monetary stimulus,” the surveillance report insisted.

Within months, of course, this premature policy tightening was withdrawn by incoming President Draghi—while a series of Very Long Term Repo Operations (VLTROs) were implemented in December 2011 and March 2012. Under the pre-text of heading off a bank funding hump, these VLTROs bought some crucial time for euroarea peripheral governments—by loosening the balance of payments contraint temporarily. But it would eventually take Draghi’s “whatever it takes” moment in the summer of 2012 to reserve capital flight related to fears that the euroarea would indeed dissolve.

As capital inflows resumed to the periphery in the second half of 2012, banks were once again able to access private funding. And a key problem with VLTROs was that they allowed early, voluntary repayment. They were not “outside money” to the financial system, as with standard Quantitative Easing, but were “inside money”—simultaneously both an asset and liability of the banking system. So, with enhanced liquidity, euroarea banks—perhaps to signal their access to private funding—began repaying these borrowed reserves. This brought about the endogenous tightening of monetary conditions—as base money and excess liquidity contracted, EONIA increased and the euro appreciated. This monetary tightening was entirely preventable. But it took the associated euro appreciation and disinflation pressure for the ECB to act through a series of exceptional measures in 2014 and 2015—from negative interest rates to APP.

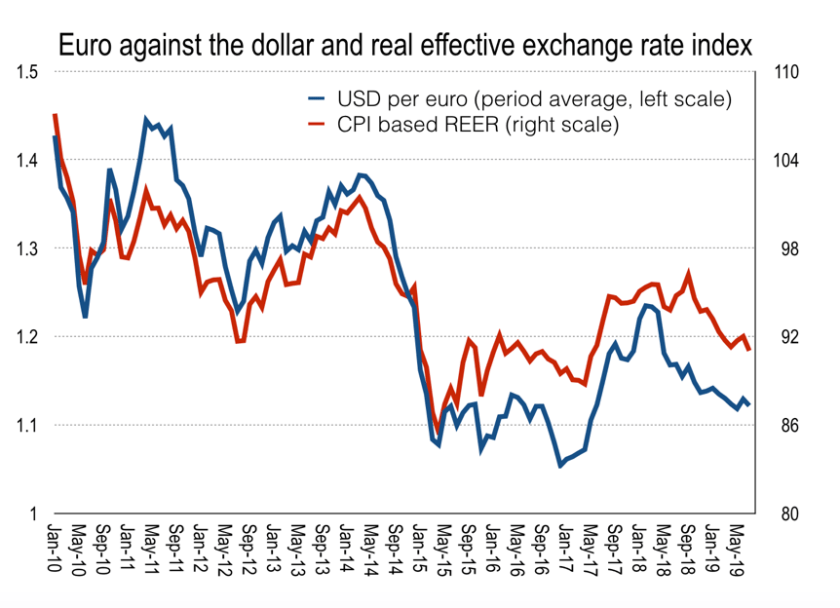

The result of this monetary loosening and endogenous tightening was that the euro depreciated nearly 15% against the dollar between end-2010 and mid-2012 as fears about the euro area emerged. It then appreciated on endogenous tightening through early-2014. This was followed by a sharp depreciation as deflation risk emerged and investors began to factor in exceptional policy support. The euroweaked 15% in real effective terms and 21½% against the dollar since end-2010.

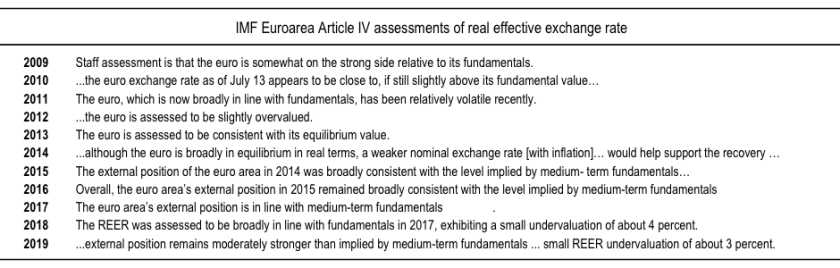

The Fund was largely a champion of fiscal consolidation throughout this period, only in recent years encouraging fiscal expansion. Still, the impact on the euro of the monetary reaction falls squarely within the IMF’s mandate. How has the Fund throughout Lagarde’s term assessed the euro exchange rate? The table below summarizes the conclusions on the external value of the euro since 2009, taken from the euroarea surveillance report each year, as the euroarea current account went from near balance to about 3% of GDP on peripheral depression and flawed fiscal response.

What is most striking is how difficult it has been for Fund staff to provide a proper assessment of the euro exchange rate. Even in 2015 and 2016, with sharp depreciation as monetary policy strained to offset the distortions imparted by flawed fiscal policies, staff considered the euro as “broadly consistent with medium-term fundamentals.” This policy action impacted the rest of the world largely through the weak euro, of course. And one of the IMF’s core functions under the Second Amendment to the Articles of Agreement is the assessment of policies as they impact others through the exchange rate. This is not to claim that exceptionally loose monetary policy was inappropriate, only that a more thoughtful assessment of deflationary global spillovers through the currency would have helped underline the true cause of this problem in fiscal policy.

MOST RECENT has been the IMF’s intervention in Argentina. Unlike Greece, this is entirely on Lagarde’s watch. But like Greece, it is defined by the primacy of politics over analysis in program design.

For several years prior to the IMF’s latest involvement in Argentina, the government leaned on the central bank (BCRA) to finance growing fiscal deficits. For example, as well as purchasing government debt directly, BCRA was transferring profits to the government throughout. However, the central bank had negative net income throughout. How was BCRA making profits then? Due to Peso depreciation which created paper gains on foreign exchange reserves. And so, as the currency depreciated, BCRA would make paper gains that would serve as the basis for cash transfers to the government. Since 2011, BCRA transferred ARS375 billion in profit to the government, averaging 0.9% of GDP per year all the while BCRA capital was shrinking from 1.4% of GDP in 2011 to 0.7% of GDP in 2017.

In fact, BCRA did not even have income to pay for administration costs and the printing of paper currency, so would create base money for this purpose as well. Overall, to prevent the impact on base money from this and other transfers to the government, BCRA would issue interest bearing securities. But absent the real resources to finance these sterilization operations, the central bank had to resort to either printing more money to pay the interest on these or issue ever greater securities in a monetary policy Ponzi scheme.

The overall fiscal and quasi-fiscal position was much worse than the IMF acknowledged at program outset, therefore. The interest bill on BCRA securities more than 2% of GDP, a hidden fiscal deficit. But the program proceeded as if this was of no importance when assessing fiscal sustainability. The recapitalization of BCRA—a known and possibly substantial fiscal cost—was acknowledged, but was only to be completed by end-2019. Moreover, monetary policy proceeded by increasing interest rates without recognizing that this would either bring future monetization and exchange rate risk, or an additional impact on fiscal sustainability to be later realized. Investors meanwhile proceeded as if these quasi-fiscal risks did not exist.

These challenges were known in advance—or could have been known with the forensic analysis of monetary-fiscal interactions. And addressing them early as prior actions when building the program would have triggered early either debt reprofiling or restructuring. Instead, the Argentine authorities leaned on the Trump administration; the US Treasury leaned on the Fund; Lagarde waved through largest program in IMF history—potentially USD57 billion, of which about USD44 billion has been disbursed—based on a monetary policy Ponzi scheme.

WHAT DO these serious cases have in common? They are all characterized by deeply flawed macroeconomics and political influence on decision-making—and there is typically a quid pro quo involved. For Osborne, Lagarde delivered on austerity and Brexit analysis in the joint pursuit of his political goals and her career ambitions. In Greece and Cyprus, Lagarde sided with Germany throughout—allowing deeply flawed analysis to pass her desk to keep the Greeks under the European thumb and impose costs on the Cypriot taxpayer. In exchange, it was widely rumored Lagarde was under consideration for a European Commission role in 2014—but was ultimately still needed in DC. When it came to analysis of the euroarea, the IMF has been incapable of balanced assessment of fiscal-monetary policies; the assessment of the euro has been stale and thoughtless throughout. But this was necessary so that German fiscal policy would not be under scrutiny, ingratiating herself with Chancellor Merkel. In the case of Argentina, despite being castigated for being under political influence throughout the euroarea crisis, Lagarde was found under the influence of the US Treasury in signing off on a program that hinged on a continuing monetary policy Ponzi scheme.

BEFORE LAGARDE at the IMF there was Dominique Strauss-Kahn (DSK) of course. And DSK perfectly set the tone for Lagarde’s time at the Fund.

Strauss-Kahn was commonly expected to use his time at the Fund as a springboard to the French Presidency, dethroning Sarkozy. Indeed, during his successful bid to become Managing Director in 2008, Strauss-Kahn employed Paris-based public relations firm Euro RSCG (as then called) to manage his image. Then, upon DSK taking the job, the IMF immediately “hired two big-name PR agencies to help spread the Fund’s message” as Reuters explained in August 2008. These two contracts were said to be worth between $1.5 million and $2.0 million—an unusual expenditure at exactly the time the Fund was trying to cut costs by $100 million per year. Though everyone turned a blind eye, one of the firms chosen was the very same Euro RSCG—the company that supported DSK’s campaign, a firm run by friends of Strauss-Kahn, the same friends who were amongst the first to visit him when on bail following allegations of sexual assault.

The awarding of such large contracts strongly hinted at DSK’s desire to use his position at the IMF to forge his image and further his political ambitions in France—a stealth campaign from the relative distance of DC. But it also smelt strongly like misuse of public funds.

How would Sarkozy respond to this growing threat from across the Atlantic? According to the retelling of the circumstances surrounding DSK’s arrest in New York City in May 2011, there are secret recordings of Strauss-Kahn discussing his candidacy with friends just days before his arrest. DSK was perhaps being monitored by the French secret service, his actions potentially relayed directly back to Sarkozy. Moreover, it is possible that DSK’s criminal actions that day were orchestrated at Sarkozy’s request to explicitly disqualify Strauss-Kahn from the French Presidential race—if true, a remarkable intervention in global governance, at a pivotal moment in the euroarea crisis, for purely domestic political reasons by a European sovereign.

Put another way, DSK’s tenure underscored how European politicians have never been interested with what they can do for the IMF, only what the IMF can do for them.

Following in DSK’s footsteps, Lagarde has levered her time at the Fund to promote her career within European institutions. Being asked to replace Draghi as President of the ECB would appear to reward fealty, sycophantism, and analytical incompetence. These are not qualities that the most senior monetary policy position in the euroarea requires.

There are three arguments surrounding Lagarde’s ECB appointment that we might dismiss based on her track record.

First, Lagarde is a continuation of the status quo—and therefore a dovish replacement for the current President. Honestly, this we do not know. She was as supportive of Trichet’s failed policies as she was of Draghi’s enlightened interventions. She has no track record in monetary decision-making, and has shown no command over the intricacies of central bank balance sheet interactions and financial superstructures. And those decisions she has been involved in during the euroarea crisis were often destabilizing.

Second, Lagarde will be able to bring her political gifts to command greater monetary-fiscal coordination. In fact, her record in terms of holding euroarea creditors to account demonstrates nothing but fiscal conservatism. Moreover, her written answers responding to the European Parliament questions before her formal appointment exhibits no appetite to challenge the deflationary fiscal bias in the euroarea—beyond supporting a future centralized fiscal resource.

Third, technical staff will keep Lagarde on the straight and narrow. More likely, she will promote those staff who provide the analysis needed to advance her own personal objectives or help deliver on some political side-deal or other.

Overall, the biggest risk to the euroarea today is the unknown—and unknowable—quid pro quo that might underpin the decision to appoint Lagarde to replace Draghi or might emerge in the future as the new President plans her own future. If Lagarde sees her tenure at the ECB as a stepping stone to something more—she will be in her early-70s by the end of her term, meaning there is still time to become, perhaps, the first euroarea Finance Minister or take another elder statesperson role—then monetary policy over the next 8 years can easily come under political influence. And the assumption that Lagarde is a like-for-like replacement of Draghi is a huge misreading of her track-record.

END.

4 thoughts on “Goodbye IMF, hello ECB. But what’s the quid pro quo?”