What can we expect of Argentina’s 5th program review? We are told the IMF team arrived in Buenos Areas on Saturday. Presumably the objective is to complete this review by end-September—as this review will be judged against the end-June program targets, already passed. IMF funds can be released before the election, therefore. The implications of the election can be dealt with later. This is the right decision, in my view—despite the challenges facing Argentina. The global community owes Argentina some forbearance.

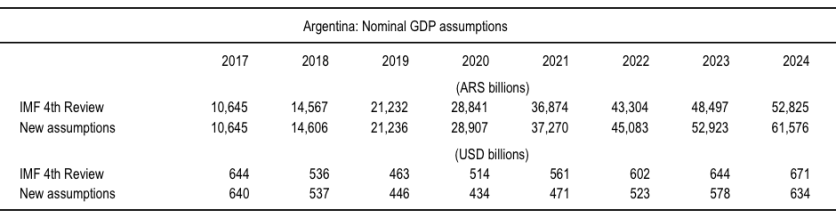

Still, what might be the new path for public debt-to-GDP in the 5thReview? This depends on the politics driving the optics of requiring debt-to-GDP at 60% by the end-forecast horizon. The table below summarizes assumptions that underpinned the 4thReview. The IMF already implicitly assumed ARS would reach 49.4 by year-end, so had factored in some depreciation. Then again, even at ARS55 we are 10% weaker still. The recent exchange rate move with large liability dollarization throws the previous DSA out the window. The Fund also assumed an increasing share of ARS denominated debt over the forecast horizon and low effective interest rates on Federal debt—with negative real yields driving down debt-to-GDP.

How might these assumptions change? Let’s knock out our own projections and see where this takes us. Let’s assume ARS sits at 55 through September, depreciates 2% a month through end-2020, 1% a month through 2022, and ½% a month thereafter. This gives us a new path for end-year ARS as shown in the table below. These new assumptions see ARS reach 99.8 by end-2024, compared with 79.5 implicit in the IMF’s 4thReview.

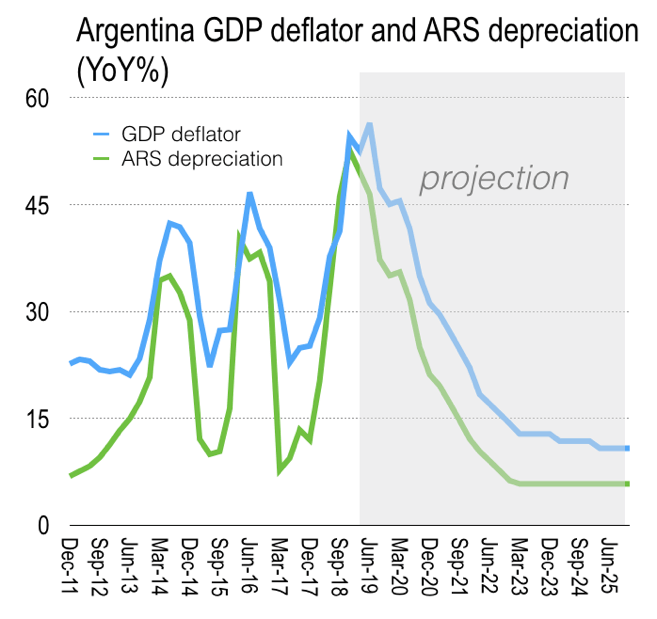

How might this translate into GDP deflator? The chart below demonstrates congruence between exchange rate depreciations in Argentina and changes in the GDP deflator—and the lag is slight. It also shows a projection for the GDP deflator which assumes a generous spread for the GDP deflator relative to ARS depreciation ahead.

This translates into a secular increase in the ratio of the GDP deflator-to-ARS, returning to levels seen in 2017 by 2025, as shown below—arguably a period of overvaluation, but let’s ignore that.

In addition, let’s assume 1% contraction in GDP for this quarter and the next, 0% growth each quarter next year, and 1% quarterly growth thereafter (more generous than the IMF’s 4thReview in later years, perhaps too generous compared to reality near-term).

How does this convert into a revised path for nominal GDP? This is shown in the table below. Two things are worth emphasizing. First, nominal GDP in ARS is barely changed in 2020 despite the additional ARS depreciation here. This is because the IMF are far too generous in their GDP deflator assumptions—driving down debt-to-GDP. This alternative GDP is roughly unchanged relative to the 4thReview for 2020 despite sharper ARS depreciation. That said, in later years GDP in local currency increases above the 4threview assumptions—though not in USD. According to this new projection, USD value of GDP fails to surpass 2017 levels by 2024.

This takes us some way to generating a revised debt path. We need to address the issues of interest and the primary balance.

On the interest bill, it’s anyone’s guess at this point. For example, between the 3rd and 4th Review, the expected interest bill for the first 6 months of 2019 in the fiscal financing tables was substantially reduced. At the time of the 3rdReview, the 2019H1 interest bill was projected at USD10bn. By the 4thReview this had been reduced to USD7.3bn, with the financial and nonfinancial public sector contributing 90% of this lower interest burden. At the same time, there was an increase in projected amortization over the same period of USD1.6bn—of which public sector amortisation contributed 84% of this increase. It’s as if public sector bodies had been asked to reduce recorded interest paid by the Federal government and roll this into amortization—certainly this is how the BCRA “profit transfer” of end-May was treated. This presumably allows the Federal government to show a lower fiscal deficit for the year due to a lower interest bill, contributing to favourable debt dynamics. Note also, the 4thReview effective interest paid in 2019 was expected to be 5.5%—ridiculously low for one of the world’s least creditworthy governments—increasing to only 10.9% by 2022.

If the authorities, with IMF consent, are willing to play such games with the fiscal numbers, it’s difficult to pre-empt what they might cook up for optical purposes. Instead, let’s call bullshit and simply add 200bps to the 4thReview interest rate assumptions throughout—this being still incredibly generous in my view given ongoing institutional malaise and necessary monetisation. There is a case to increase the interest bill further, but let’s overlook this.

As to the primary balance, let’s assume a deficit this year of 1%, 0% next year, and 1% surplus thereafter. Perhaps.

Anyway, the final assumption necessary is the currency composition of debt. Let’s assume local currency debt stays constant in % of GDP, with FX issuances making up the rest.

With these assumptions—not, admittedly, a true bottom up DSA, rather top-down—where do we end up? The chart below contrasts the 4thReview with these revised assumptions. While the 4thReview could show a monotonic reduction in the debt-to-GDP from 2018, our alternative sees debt increase near-term, beyond which it falls. But debt-to-GDP still sits above 75% by 2024.

The key reasons for the less favourable debt dynamics are the less ebullient GDP deflator, the higher interest rate, and the larger share of fx denominated debt. It’s worth emphasizing again this is more back-of-the-envelope than bottom up analysis. But sometimes simplicity delivers clarity.

The key reasons for the less favourable debt dynamics are the less ebullient GDP deflator, the higher interest rate, and the larger share of fx denominated debt. It’s worth emphasizing again this is more back-of-the-envelope than bottom up analysis. But sometimes simplicity delivers clarity.

That said, I would expect the IMF to continue to use the GDP deflator and interest rate assumptions to deliver a more favourable debt path to the above—coming in closer to 70% of GDP by 2024, perhaps.

Regardless, none of this addresses the need for BCRA recapitalization. Absent this institutional imperative there will be continued monetary instability. This will be addressed after the election, should the program continue. And it will add materially to the ratio of public debt-to-GDP. Given the implied interest on BCRA liabilities of more than 2% of GDP currently, once this is dealt with public debt will look even less favourable, and the prospects for sustainability eroded further—sensible restructuring will have to factor this in.

Finally, this does not factor in the challenge of rebuilding international reserves. Sustainability for Argentina should consolidate the Federal government with BCRA, not only to deliver sustainable monetary policy, but as corollary to uncover a path for balance of payments that might—at last—bring about fiscal-financial stability. This ought to be an explicit concern in program design, but remains elusive. This underscores the inadequacy of the IMF’s debt sustainability framework, and the risks investors in Argentina continue to take.

But even the above would allow the IMF to continue to engage with Argentina until the election is over.

END.