The original Argentina-IMF program agreed in 2018 with the Macri administration is coming under growing scrutiny as a replacement arrangement is being negotiated once more. Last week, legislators sent a letter to IMF Managing Director Georgieva to complain about the Fund’s involvement with Argentina, apparently broken into 31 different points.

In particular, Senators are suggesting the Fund broke the Article VI of the IMF’s Articles of Agreement in the original program, under pressure from Macri via the Trump administration, and that as a result the Fund should accept responsibility for the failure—including by setting no conditionality in the program under negotiation.

As if to underline the case, local press claims that a senior IMF official visiting Buenos Aires was heard to agree that Article VI was indeed violated—that “(a) A member may not use the Fund’s general resources to meet a large or sustained outflow of capital…” The complaint surrounds USD6BN in IMF funds that were apparently ringfenced with a view to intervening in forex markets up to a value of USD250 million per day.

This refers to a provision introduced during the First Review in October 2018 when, following protracted pressure on ARS over the summer and general loss of confidence, the program was augmented in size to about USD56BN and made non-precautionary.

At that time, a non-sterilized intervention rule of USD150 million per day was announced. To wit: “the central bank is committed to undertaking no FX purchases or sales within a wide, ‘non-intervention zone’ (of AR$39 per US$ ± 15 percent). In the event the currency were to move outside of this zone, the BCRA would have the option (but not a commitment) to announce a competitive auction to either buy or sell up to US$150 million per day. The central bank is committed to ensuring that all FX purchases/sales are unsterilized, which would result in an expansion/contraction of base money.”

This was later adjusted, during the Fourth Review published July 2019, to USD250 million per day in conjunction with a floor on LELIQ interest rates of 62.5% as part of a base money stabilization rule. In particular, “If the exchange rate is above AR$51.5 per US$: the BCRA would be prepared to sell up to US$250 million (an increase from the previously announced US$150 daily limit) and may undertake additional interventions to counteract episodes of excessive volatility.”

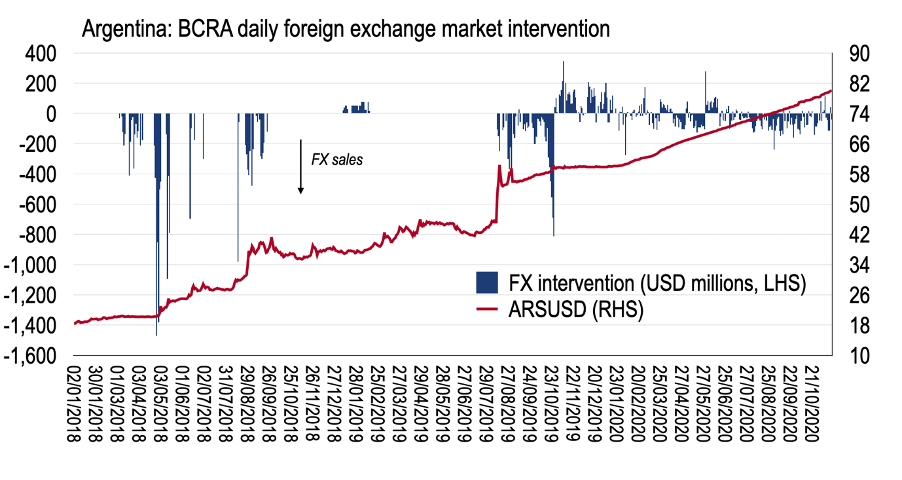

It’s reasonable to ask whether this intervention rule was indeed a substantial draw on scarce foreign exchange, therefore. The chart below shows daily intervention and spot ARS exchange rate. In fact, the period between October 2018 (when the USD150 million daily intervention was available) and July 2019 (when the USD250 million extension was agreed) there were no foreign exchange on-market sales.

Of course, from August 2019, following the PASO election result, ARS depreciated sharply and intervention began once more. However, intervention was initially rather modest—and in any case, after the program was considered off-track by the IMF in late August, any decision to support the currency in foreign exchange markets thereafter was a monetary decision by the authorities. Decisions taken while a program is officially off-track can hardly be considered the responsibility of the Fund—thus hardly abrogation of Article VI. Indeed, during September and October 2019, intervention amounted to USD5.4BN, or about USD120 million per day. The question then becomes about the counterfactual; absent such intervention, the currency would have weakened even further, inflation would have accelerated even more, damaging real incomes and creating greater monetary disturbance.

Of course, there are many ways to lampoon the IMF’s work in Argentina, and they should indeed accept a large part of the blame for the mess in the Southern Cone. But the argument about Article VI is an odd way to approach this. And the fact that a senior member of the current IMF team has apparently endorsed this view just reflects the ongoing incompetence of senior staff at the Fund—which doesn’t bode well for potential solutions in the period ahead.

An alternative approach to unpicking the IMF’s work in Argentina is to recall the assumptions that underpinned the original program from June 2018—the basis on which the program failed and today’s uncomfortable embrace is based.

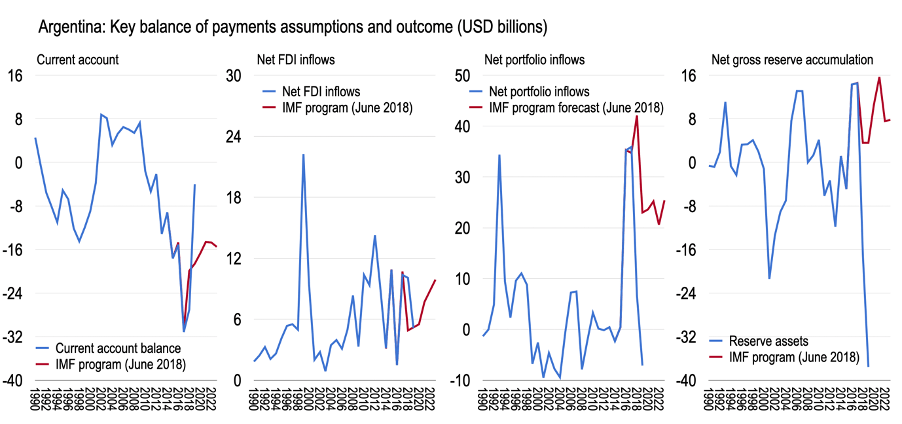

The simplest way to do this is to look at the balance of payments flows that were expected to stabilize the economy. At that time, the cumulative current account over the 6 years from 2018-23 inclusive was projected to be exactly USD100BN deficit, due mainly to a USD60.7BN service deficit and USD56.5BN primary income deficit (i.e., net interest payments on external debt.) In addition, BCRA reserve assets were expected to increase USD48.9BN while there would be net other investment outflows (ex. official IMF flows) of USD54bn, concentrated mainly in 2018 and 2019 as previously accumulated non-resident LEBAC claims on the central bank were rolled off.

Adding up these three external financing requirements, therefore, we get a USD203BN financing need. Meanwhile, the IMF program was at that time only precautionary and was being repaid in full—thus there was no net external support from the IMF cumulated between 2018 and 2023. So, the assumed net USD203BN supportive external financing flows over 6 years was entirely due to private inflows.

Put another way, Argentina would be doing well if GDP was about USD500BN at this time, so there was assumed about 40% of GDP in cumulative net external financing inflows between 2018 and 2023 to finance absorption, non-resident deposit outflows, and BCRA reserve asset accumulation. What were these flows? Well, net FDI inflows of USD42BN was projected along with USD160BN in net portfolio inflows.

A counterpart to the net portfolio inflows over the projection horizon, of course, is growing external debt. Hence, total external debt was expected to increase from USD236BN as of end 2017 to USD362BN by 2023; of this, official external debt was expected to rise from USD164BN to USD265BN over the same period.

So, program design hinged on the flimsy adjustment agreed at that time catalysing non-resident portfolio inflows on a large scale. To put this in context, the chart below shows non-resident portfolio outcomes in 2018 and 2019 (annual data) against the initial program projections. The massive draw on reserve assets even surpasses the 2000-01 experience while net portfolio debt inflows failed to materialize on any reasonable scale. In fact, while the IMF program, agreed mid-2018, had net portfolio inflows of USD42BN in 2018 and USD23BN in 2019. Instead there was a net inflow of only USD6.7BN in 2018 and an outflow of USD7.1BN in 2019. Of course, the program was ramped up in the meantime. But rather than continued private sector inflows, there was a sudden financing stop in terms of portfolio flows. And rather than the current account deficit stabilizing, it sharply contracted and is today in surplus.

So, there are many reasons to complain about the IMF’s involvement in Argentina—a program that had no chance of success from the start. But it’s important to focus on the real failures of the Fund—rather than some nonsense claims about Article VI.

END.