With a new Chancellor of the Exchequer safely in place, Rishi Sunak’s Budget on March 11th promises to be the most important fiscal announcement in the United Kingdom (UK) since Chancellor Osborne’s politically astute, but economically and socially destructive austerity budget in June 2010.

The next Budget needs to provide clarity on two aspects of fiscal policy for the generation ahead: first, how will the UK navigate inevitable Brexit-related disruptions; second, what is the overall fiscal envelope available for necessary long-term investment and “levelling up” of the UK economy.

And these fiscal choices need to be taken against the global backdrop of central banks running short of policy space to offset disruptions—meaning the Bank of England (BoE) can play only a limited role of facilitating “structural” adjustment. Meanwhile, policy in the euroarea—our most important neighbour—continues to be woefully inadequate, with fiscal policy hideously suboptimal and European Central Bank (ECB) likely to continue asset purchases as far as the eye can see.

In short, fiscal policy is the only game in town. And the UK is now in a position to dextrously manage her own policy to take advantage of the fiscal failures in Europe while navigating Brexit and levelling up the economy. Chancellor Sunak faces a unique opportunity to offset the worst consequences of Brexit and build a brighter future for a generation.

Recall the issuance and absorption of United Kingdom government debt over the past few decades. Central government debt issuance peaked around 14½% of GDP late-2009; since then—accompanying the stabilization and recovery of the economy, as private spending picked up—debt issuance fell to about 8% of GDP in 2011 and has drifted towards 2% of GDP over the period since.

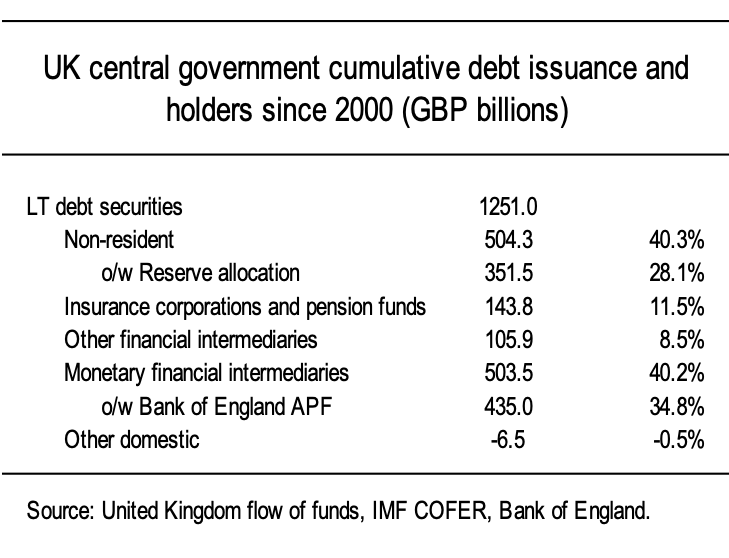

Issuance is largely of long-term securities of course. Of GBP1,345 billions of central government securities issued, GBP94 billion (7%) were short-term (< one year) and the remaining GBP1,251 billions long-term. And of this total issuance, about 41% was absorbed by non-residents.

To be precise, of GBP94 billions in short-term securities issuance, GBP46 billions (49%) have been absorbed by non-residents over the years; of the GBP1,251 billions long-term debt, GBP504 billion (40%).

The remaining part of central government debt is absorbed predominantly by domestic financial intermediaries—in particular, pension funds and insurance (11½%), other financial intermediaries (8½%) and monetary financial intermediaries (40%). The latter includes the BoE purchases under the Asset Purchase Facility initiated in 2009, of course. As of 2019Q2 they held about GBP435 billions under this scheme.

Meanwhile, the change in reserve manager GBP asset holding since 2000, according to the IMF COFER database, is about GBP350 billions. This is an overstatement of the flows in gilts since it: includes valuation adjustment (as change in stock); does not adjust for the change in allocated reserves over the period; and might include alternative sterling assets. Nevertheless, it seems safe to claim that over the past 2 decades more than 50% of central government debt issued by the United Kingdom has been absorbed by non-resident central banks together with the Bank of England—thus associated with base money or near-monetary liabilities of various central banks, and in some sense “money demand.” See table. This means UK government debt has something of a “special” character—it is demanded for its qualities beyond the yield it delivers. It is safer than other financial assets, and in short supply.

Alternatively, 75% of gilts issued since 2000 have been absorbed by non-residents and the BoE. Only about ¼ are therefore available for resident savings through domestic financial intermediaries—with about half this remaining amount being absorbed by domestic insurance corporations and pension funds.

Non-resident absorption of UK central government securities picked up sharply in the early-2000s, as visible in the chart above, such that by 2006 nearly all net issuance was taken by non-residents—predominantly, presumably, emerging market central banks. Following GFC, of course, domestics took a larger share of government debt issuance while EM central bank net accumulation likely fell towards zero. But in recent years, non-residents have been the predominant buyers of gilts again, as discussed below.

The next chart shows the stock of United Kingdom general government debt decomposed by non-resident and domestic holders. Bank of England holding here is proxied by their quarterly balance sheet net claims on government.

Debt-to-GDP, at around 84% of GDP, has been on a glacially declining path after peaking in 2014. Debt-to-GDP was about 41½% of GDP in December 2007, just before the Great Financial Crisis (GFC). Of this, about 28½% of GDP was held by residents (ex. BoE), 12% of GDP held by non-residents. Today, debt held by these same residents is no higher than pre-GFC. Of more than 40 percentage points of GDP increase in general government debt, 52% has been absorbed by non-residents and 48% by BoE. The resident private sector holds no greater claims on the government today as when Tony Blair was Prime Minister.

Any fiscal rule promulgated by the incoming Chancellor proposing a reduction in the stock of UK government debt-to-GDP from here will, other things equal, force resident financial intermediaries—including pension funds—out of government debt and into some unknown other financial instruments. Contrary to the idea that fiscal austerity makes pensions “safer,” it forces greater risk taking amongst domestic financial intermediaries which might instead put domestic pensions in jeopardy.

Since 2014, the United Kingdom has been the recipient of substantial portfolio inflows from the euroarea. The left side of the figure below shows ECB data (converted to GBP) on total euroarea portfolio debt accumulation since 2004, distributed into outflows to the UK and to the rest of the world (ROW). The euroarea current account is also shown. In recent years, portfolio asset accumulation by euroarea residents has mirrored the emerging current account surplus there, which is running around GBP300 billion per year—slightly lower than 2017-18 when Ireland-related distortions overstated the surplus.

Meanwhile, portfolio asset accumulation has itself been more recently distorted downward by US corporate tax changes. Once this washes out, portfolio outflows will likely return once more to about GBP300 billion per year. The right side of the chart combines balance of payments data from the UK and euroarea to decompose inflows to United Kingdom long-term portfolio debt securities between the euroarea and ROW. Sales of long-term UK portfolio debt emerged during the euroarea crisis as peripheral banks drew on liquidity abroad. But since 2014 inflows have re-emerged, especially since the ECB initiated the asset purchase program (APP) in early-2015 when these inflows for a period accounted for all non-resident inflows into UK long term securities.

In particular, since December 2014 there have been GBP329 billions of non-resident inflows into long-term portfolio debt securities in the United Kingdom (ONS data), of which about GBP206 billions (63%) emanated in the euroarea (ECB data).

We cannot further decompose by geography inflows into gilts precisely, but around the time of the ECB’s APP it is noteworthy that the interest rate on 10Y UK government securities was driven for the first time substantially below US Treasuries. Chart below.

Until 2012, long-term yields in Germany, UK, and US were reasonably congruent. Then, following euroarea crisis, when a growing current account surplus and tightening eurosystem liquidity upon repayment of VLTROs brought about euro appreciation and deflation risk, bund yields drifted lower—in anticipation of ECB moving to negative rates and APP. Then, from late-2014, gilt yields fell below their US equivalent. UK benefitted from accelerating euroarea inflows as the shortage of yielding assets there generated search for pick-up elsewhere. The 10Y gilt yield peaked about 150bps below US Treasuries mid-2018 and remains 120bps below still.

Such were the spillovers onto UK asset prices of recent flawed policies in the euroarea—in particular, fiscal policy being too tight, causing a globally substantial current account surplus to emerge; deflation risk and the need for unconventional monetary policy by the ECB. This constellation of policies, which looks set to continue, creates a shortage of euroarea safe assets and the continuous inflow of euroarea and other non-residents into UK portfolio assets, holding gilt yields ever lower. Even during the global acceleration in 2017, the 10Y gilt yield hardly increased above 150bps. Considering the UK economy has been growing at about 3.5% in nominal terms since 2010, this implies the nominal cost of borrowing substantially below the nominal growth rate even when the global economy is strong.

Consider finally the UK’s external current account—composition and financing. The UK current account is comprised of a substantial net surplus in services of about 5% of GDP, of which about ¾ is extra-EU and only ¼ with the EU. Against this there is a goods deficit of about 7% with about 65% due deficit with the EU. In addition, the UK runs a deficit on primary and secondary income of about 2½% of GDP with a little less than half the secondary income deficit due to net EU budget transfers.

In short, the UK’s overall current account deficit shadows our bilateral trade balance deficit with the EU—while the overall service surplus roughly offsets the deficit on non-EU goods plus primary and secondary income. Alternatively, the UK’s bilateral service surplus with the EU plus euroarea portfolio inflows in normal times nearly covers the UK’s bilateral trade balance deficit with the EU. In a sense, there is a reciprocal trade-and-financial relationship with Europe.

Turning more generally to financing, gross and net financial flows in the balance of payments can be large. But net financial inflows into GBP assets was persistent through both GFC and the Brexit referendum. Indeed, steady net inflows into government portfolio debt, noted above, has provided a substantial share of needed net external financing throughout—sometimes enough to finance the current account in full. More recently, the sharp fall in GBP following the Brexit referendum resulted in large net FDI inflows as non-residents saw a cheap opportunity to purchase UK-based companies. Indeed, net FDI inflows reached about 11% of GDP in the year through 2016Q4. Any further Brexit-related Sterling weakness will likely generate further “Fire Sale FDI” inflows. In combination, the continuous non-resident bid for gilts and net FDI inflows on GBP weakness make financing the current account unlikely to be a major concern—providing government policies do not turn substantially against business interests.

Why does this matter when contemplating policy in the United Kingdom today? Fiscal policy and rules are too often designed on the basis of some false notion of “sustainability” and flawed understanding of the needs of finance in mind. This is certainly true of the European Union’s fiscal rules, which are outdated and atavistic—and from which the UK is now free to deviate.

To be sure, there are occasions when sustainability concerns and the financial sector will force a sovereign to adjust—witness Argentina or Greece. But for the United Kingdom and a few other select economies with a floating currency and debt largely denominated in local currency—especially during a period of global stagnation—finance will itself adjust to the “needs” of fiscal policy and the overall external balance. This means there will indeed be fiscal space where rigid mindedness suggests none exists—but don’t tell George Osborne. And a more sensible view of UK fiscal policy today would exploit financing available—especially from non-residents during a period where safe assets are in short supply—to navigate Brexit and bring about a fairer and more balanced economy for the future.

Let’s also recall some truths that most macroeconomists don’t like to admit to those making policy. Indeed, standard analysis of public debt sustainability tells us two things that most people happily overlook out of a inherent conservatism.

First, public debt never needs to be repaid—only serviced. This means, when the interest rate paid on this debt is above the nominal growth rate of the economy, the net present value of primary surpluses needs to equal current debt-to-GDP to assure sustainability. But, unlike a household mortgage, the stock is never repaid, only serviced.

Second, when the nominal interest rate on public debt falls below the nominal growth rate of the economy, conventional theory tells us nothing about what the stock of debt ought to be. As such, obsessing over a particular debt-to-GDP metric—like 60%—is not only strange in “normal” times. But when the interest rate is substantially below the growth rate of the economy, worrying about the debt stock is like being unable to sleep for fear of ghosts.

What kind of fiscal policy and debt trajectory might this imply? Without dictating the detail of policy, imagine three scenarios for fiscal policy in the UK.

Scenario 1 assumes the primary fiscal balance remains at 0% of GDP, the overall current account deficit is unchanged, average interest paid on debt continues to decline, while net inflows by non-residents to gilts continues at 2% of GDP. In this case, the fiscal deficit continues to decline to about 1% of GDP over a 5-year horizon. Debt-to-GDP declines to 77% of GDP, but debt held by the domestic private sector falls to 21% of GDP from 28%, crowded out by foreign inflows. We assume here, as below, the EU “divorce bill” is paid and no tariffs are applied on exports or imports.

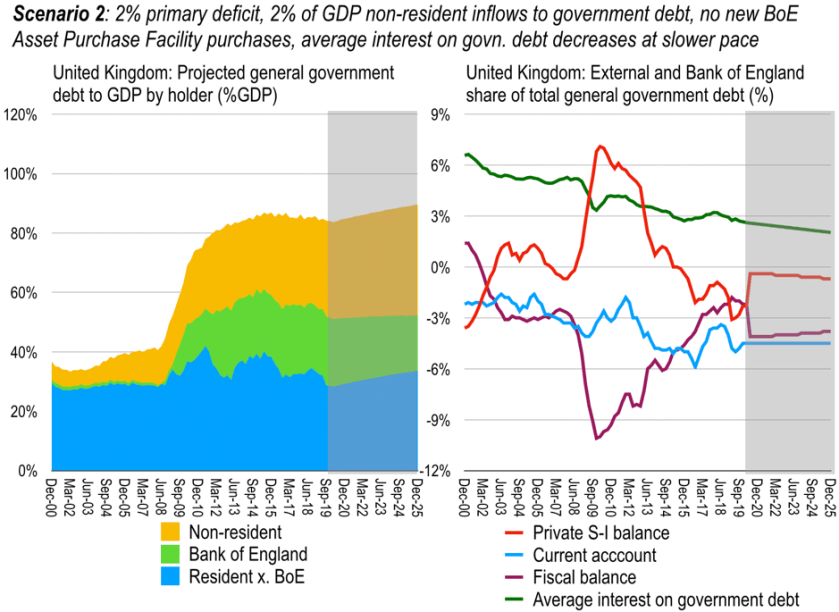

Scenario 2 alternatively imagines a 2% primary deficit throughout, while all other assumptions are unchanged except the interest rate declines at a slower pace as the cost of borrowing is slightly higher throughout. Here debt-to-GDP increases to 90% of GDP by end-2025, domestic private claims on the government increases from 28% of GDP t0 34%. This means debt-t0-GDP increases to about 3 percentage points above that attained in 2024. That said, debt in domestic private hands remains lower than at that time due to persistent non-resident inflows.

Scenario 2 alternatively imagines a 2% primary deficit throughout, while all other assumptions are unchanged except the interest rate declines at a slower pace as the cost of borrowing is slightly higher throughout. Here debt-to-GDP increases to 90% of GDP by end-2025, domestic private claims on the government increases from 28% of GDP t0 34%. This means debt-t0-GDP increases to about 3 percentage points above that attained in 2024. That said, debt in domestic private hands remains lower than at that time due to persistent non-resident inflows.

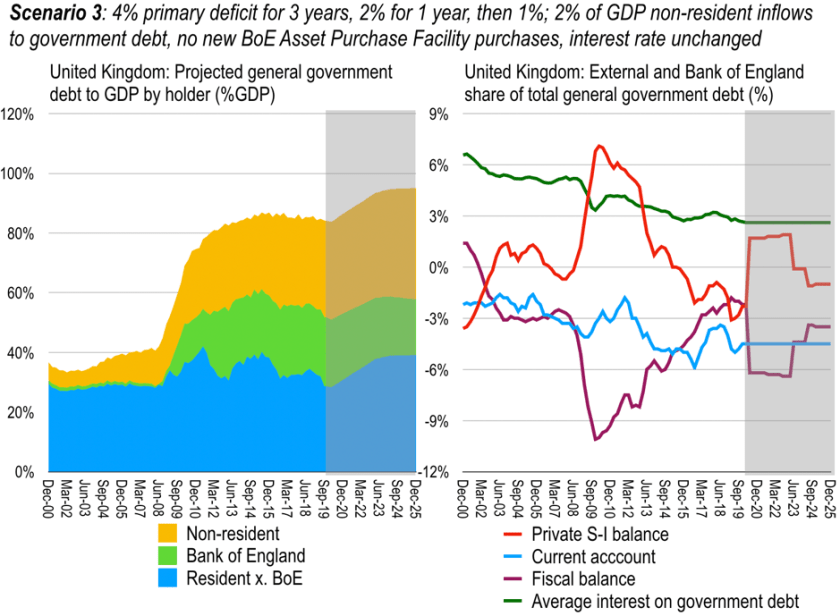

Scenario 3 is more ambitious, allowing for a more aggressive fiscal expansion to level up the economy. A 4% of GDP primary deficit for 3 years moderates to 2% for 1 year and 1% of GDP thereafter; the average interest on debt is assumed unchanged. Debt-to-GDP increases to 95% of GDP at the end of the period, with about GBP400 billion of new net primary spending over the period—or about 16% of average GDP over the period (about 2½% of GDP per year) available for investment in schools, hospitals, transport and improved technology to advance productivity in the provision of public services across the country. Meanwhile, the domestic private sector enjoys higher savings in the aggregate, alongside improved skills and public services.

Yet even such an aggressive acceleration in public spending would likely leave the UK with lower public debt-to-GDP than France, Italy, Japan, the United States, and possibly Spain by the end of the period. Meanwhile, we would retain our independent monetary and fiscal policies and the flexibility afforded by the pound to navigate shocks. As such, fiscal spending and continued external deficit will continue to be easily financed given persistently low interest rates and non-resident inflows.

If the euroarea is unable to deliver on sensible fiscal policy, creating a current account surplus and flow of saving into foreign assets, then it is reasonable for UK fiscal policy to take advantage of these failings by running a deficit at negative real interest rates.

What if the euroarea delivers a different policy mix through fiscal expansion and a lower current account surplus? Happy days! Then the UK economy can take advantage of the new sources of demand to improve the current account deficit and rebalance the economy towards exports. But if these policy failings persist, euroarea fiscal flaws are a reasonable source of strength for the UK in navigating Brexit.

END.