AS NEW ECONOMIC Counsellor and Director of Research Department (RES), Gita Gopinath, settles into her new role at the IMF, what might her priorities be to make an imprint on the world’s premier monetary institution? Here’s a suggestion. She might begin by taking control of the IMF’s global forecasts—and do so with a view to rekindling the prospects for global macroeconomic policy coordination.

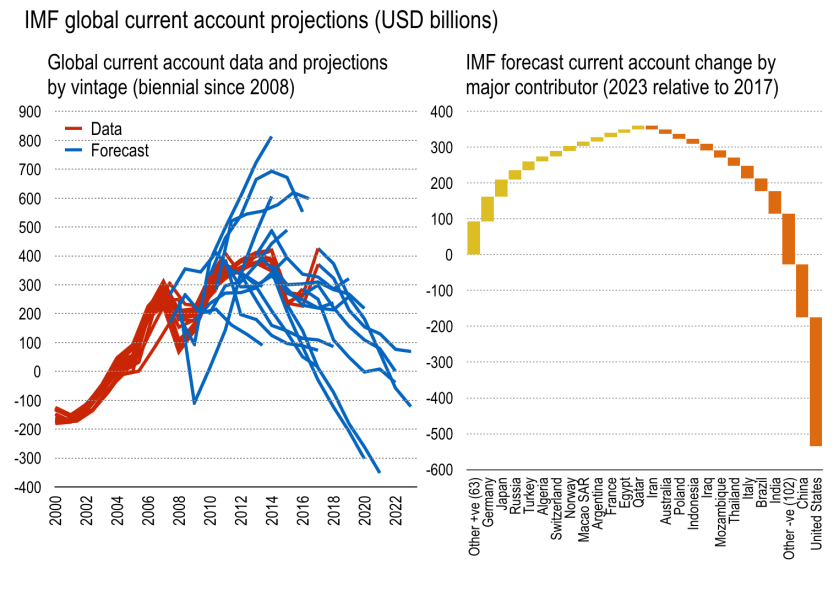

Let me explain. Already, RES is the conduit for the IMF’s macroeconomic forecasts—by collating and aggregating country-level forecasts produced by each team within the Fund, RES publishes at least twice a year through the World Economic Outlook (WEO) a forecast for the global economy. And while this process promises something of a consistency check on country-level forecasts, in truth this is little more than an aggregation exercise. This is witnessed in the left chart below, which shows the IMF’s forecast of the global current account (discrepancy) for different vintages of the WEO from 2008. The red lines are actual data, the blue lines the forecast for each vintage. Two things stand out. First, the world in the aggregate records a current account surplus of around USD400 billion. Historically, the world recorded deficits, mainly due to supposed under-reporting of investment income amongst advanced economies undertaking tax avoidance. But since the mid-2000s this global discrepancy has turned to a surplus. And this is now due to inconsistencies in the goods and service balance—advanced economies, like the UK and euroarea, both record bilateral service surpluses, for example. And it might be linked to growing world trade and emerging market predominance in the 2000s. But who knows?

Regardless, the second thing that stands out in the data is the IMF’s forecast of this discrepancy resemble the flailing legs of a wet spider crawling out of a swimming pool. Recall, this forecast is just the aggregate of individual country current accounts. Each mission chief undertakes to forecast, together with their team, macroeconomic variables for their assigned country, including the external current account. And RES, with a tweak here or there, aggregates these. As a result, the world might be seen to have an ever-larger current account surplus discrepancy as each country-team decides to forecast export-led recovery, as in 2008/09 when the discrepancy was expected to reach USD800 billion. Alternatively, and more often, IMF teams project domestic-demand led growth, with imports being absorbed and the global discrepancy shrinking—though the imports not being drawn from elsewhere, rather from thin air. The latest WEO, from October 2018, provides a good example of this. The global current account discrepancy was expected to shrink from a USD400 billion surplus in 2017 to a deficit of about USD100 billion by 2023. See right chart. Despite being joined at the hip, with near-mirror image current accounts, both the United States and China were expected to contribute, according to the Fund, by having a shrinking surplus (China) and increasing deficit (US). Meanwhile, Germany and Japan are expected to have widening surpluses, but nowhere near enough to match adjustments in China and the US. And so there is an asymmetry in numbers (>100 countries will contribute by moving towards larger deficits) and magnitudes, such that the world as a whole is seen to be moving towards restoring the aggregate deficit discrepancy by 2023. How can the US deficit be widening by USD300 billion over 6 years without other countries providing the imports for the US? Gibberish.

Regardless, the second thing that stands out in the data is the IMF’s forecast of this discrepancy resemble the flailing legs of a wet spider crawling out of a swimming pool. Recall, this forecast is just the aggregate of individual country current accounts. Each mission chief undertakes to forecast, together with their team, macroeconomic variables for their assigned country, including the external current account. And RES, with a tweak here or there, aggregates these. As a result, the world might be seen to have an ever-larger current account surplus discrepancy as each country-team decides to forecast export-led recovery, as in 2008/09 when the discrepancy was expected to reach USD800 billion. Alternatively, and more often, IMF teams project domestic-demand led growth, with imports being absorbed and the global discrepancy shrinking—though the imports not being drawn from elsewhere, rather from thin air. The latest WEO, from October 2018, provides a good example of this. The global current account discrepancy was expected to shrink from a USD400 billion surplus in 2017 to a deficit of about USD100 billion by 2023. See right chart. Despite being joined at the hip, with near-mirror image current accounts, both the United States and China were expected to contribute, according to the Fund, by having a shrinking surplus (China) and increasing deficit (US). Meanwhile, Germany and Japan are expected to have widening surpluses, but nowhere near enough to match adjustments in China and the US. And so there is an asymmetry in numbers (>100 countries will contribute by moving towards larger deficits) and magnitudes, such that the world as a whole is seen to be moving towards restoring the aggregate deficit discrepancy by 2023. How can the US deficit be widening by USD300 billion over 6 years without other countries providing the imports for the US? Gibberish.

The problem with this is obvious. If the global discrepancy cannot be explained, it would be best to hold it constant in any global forecast—or if it does adjust, to have a very clear explanation for why it is adjusting, something the IMF does not have. But this also reveals that each country-team within the Fund is acting with little constraint on their forecasts, meaning they bring “country-level” knowledge in their forecasting without any “global consistency” to their analysis. In an increasingly integrated global economy, the failure to contemplate global consistency is a huge blind spot which cannot be compensated for by any amount of country-specific, institutional knowledge.

A household would not budget without making sure income and spending match over time. Yet the IMF does not care for such nuance at the global level.

Global inconsistency is politically convenient, of course. It allows each mission chief to verify, or deviate minimally from, the official forecasts provided by their country authorities. But it also makes a mockery of the notion that the IMF is the institution uniquely tasked with steering the global economy and helping coordinate policies to sustain global aggregate demand. If each country’s policies are evaluated in isolation, and the global forecast merely a simple aggregation exercise, there can be no prospect for policy coordination. The IMF cannot act as guardian of the global economy if she has no clue where the global economy is headed. And the principle of effective demand, the starting point for macroeconomics as a science, is rendered irrelevant if output is simply expected to fall like manna from heaven—and not be the product of spending by someone, somewhere, at some point.

Such is the case today, however. It has been clear for some time that China has become the key driver of global aggregate demand, the investor of last resort. And it has also been clear that China cannot, and should not be expected to, sustain a credit bubble to drive global growth. Rebalancing growth is both a China problem (lowering domestic saving) and a global challenge. Yet global forecasts ignore the need for monetary-fiscal-financial balance sheets to expand in a sustainable manner to deliver reasonable growth. These forecasts do not provide any meaningful guide to future developments. And so China has been expected, and is still expected, to punch above her weight in driving global growth, while Germany continues to abrogate her responsibilities agreed at Bretton Woods. And the IMF is rendered almost irrelevant, except at the margin, in delivering balanced and stable global growth.

So there is indeed a great deal indeed Ms. Gopinath can do to improve the IMF’s work, if she is willing to challenge the stale thinking and vested interests inside the institution. Otherwise, as with her predecessor-but-one, Mr. Blanchard, she can instead expect events to catch her off guard. Indeed, in this respect we ought recall the crucial role of a “kid” in prompting the IMF’s work refuting austerity—the greatest policy mistake in a generation or more—as told by Mr. Blanchard himself:

“The honest truth is, I had not focused on the assumptions which were made in the programs [in the euroarea] … or the forecasts we were making for other countries. And then at some point in 2010 and 2011 all these economies did much worse than forecast… And so I did, as the Head of Research, what anybody should have done, [and asked] where did these forecast errors come from? …

And then at a meeting, a kid, I mean just an intern, drew a graph of fiscal consolidation… and the forecast errors for output… and there was an amazing relation between the two. And so I realised… fiscal consolidation was much worse in terms of its effect on output than had been assumed in our projections and by the Europeans. And I thought it was an important result, but I didn’t realize how important it was.”

One thought on “On the prospects for global macroeconomic policy coordination”