IT’S PERHAPS the greatest irony of all: just as euro area crisis appears consigned to history, should the European Central Bank (ECB) meet its 2 percent inflation target peripheral stress could return!

How so? In short: rapid unwinding of the ECB’s Asset Purchase Program (APP) due to building inflation pressure would rekindle balance of payments pressures in TARGET2 (T2) debit countries—triggering a rise in yields, slowdown in growth, and fears once more for debt sustainability.

Here we briefly explore this scenario by highlighting the exceptional risks associated with unwinding the ECB’s balance sheet—a challenge not faced by other major central banks.

To be sure, it remains too soon for the ECB to “taper” the APP. But the ongoing euro area recovery suggests Eurosystem balance sheet growth—mainly through purchase of mainly government securities—could slow or stop in 2018. At that point, absent a negative turn in the macroeconomic conjuncture, attention will turn to the timing and modalities of balance sheet reduction. How will this happen in the euro area given the uneven distribution of high-powered money?

In any case, Governor Mario Draghi’s term ends October 2019—and a replacement will be sought next year. Seldom has one person been so crucial to a region’s monetary-macro-financial stability. When institutions are frail, personalities matter.

Draghi’s heir-apparent, the Bundesbank’s Jens Weidmann, will not only have some considerable boots to fill, but will also carry the weight German expectations—including the narrative that low interest rates are an unnecessary drag on savers, while T2 credits represent the risk of impending inflation.

During any balance sheet normalization in the euro area, policy missteps or a misreading of the financial super-structure could prove disastrous.

A T2 snapshot

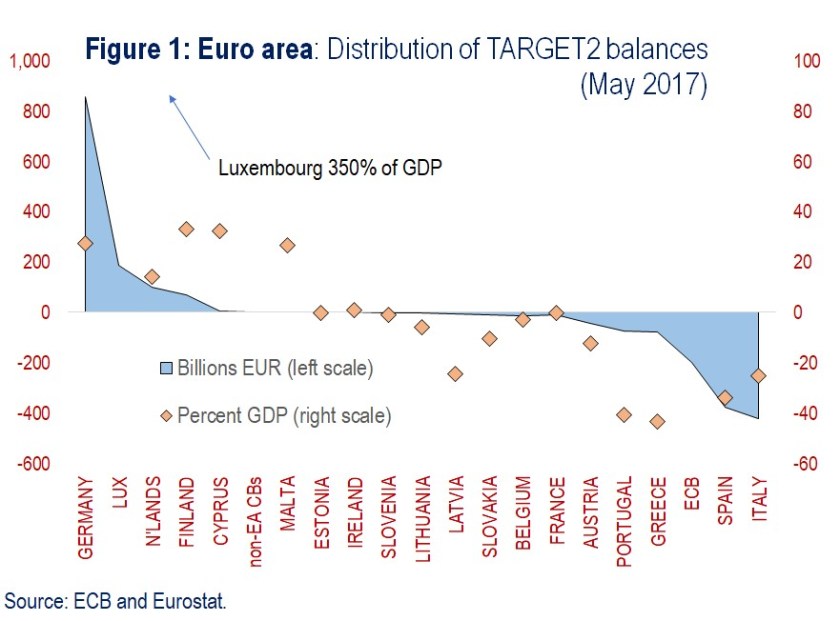

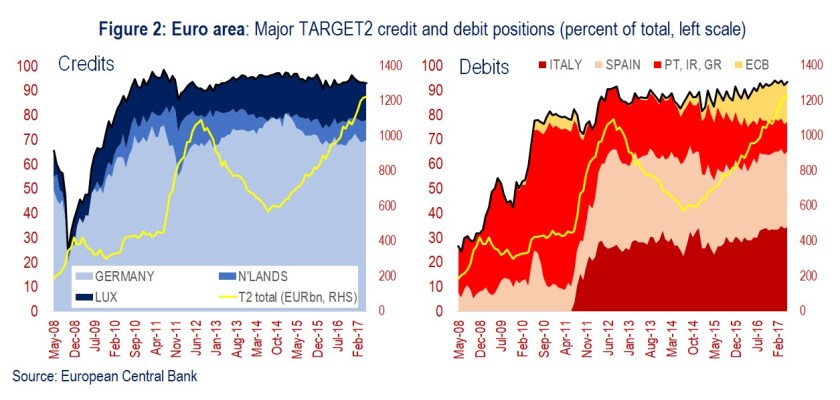

Figure 1 shows the distribution of T2 balances, credits and debits, as of end-May 2017—in billions of euro (left scale) and percent of GDP (right). Figure 2 shows the distribution through time of total T2 credit and debits of major countries.

The three largest creditors in absolute terms—Germany, €857bn; Luxembourg, €188bn; and the Netherlands, €98bn—total €1143bn or 93 percent of €1228bn total TARGET2 credits in May. Against this, the largest three debtors to the Eurosystem expressed through TARGET2 represent €995bn or 81% of the total—being Italy, €422bn; Spain, €375bn; and the ECB, €198bn.

Curiously, total T2 credit/debit position now exceeds that recorded at the height of the euro area crisis.

The previous local peak, of €1,093, was August 2012—just one month after Draghi’s “whatever it takes” speech. At that time, Germany’s T2 credit reached €751 billion. Since December 2016 the total T2 credits has exceeded the 2012 peak, and is currently 12 percent larger than at that time (Germany’s 14 percent larger). In addition, Italy’s imbalance is now larger than Spain’s.

Moreover, on current trends, Germany’s T2 credit will likely reach €940 billion by end-2017 and, depending on the details of APP tapering, could touch €1 trillion by end-2018. As a rule-of-thumb, for every €1 created by the Bundesbank in the purchase of government securities, Germany’s T2 credit increases by €0.9—meaning Germany’s base money—roughly the sum of the two—is increasing at about double the pace of local APP purchases.

Finally, since the euro area crisis began, the Netherlands, Luxembourg, and Germany have continually accounted for roughly 90 percent of all T2 credits. Early in the decade, Greece, Ireland, and Portugal were the major T2 debit countries; today Italy, Spain, and the ECB dominate.

The official narrative

The National Central Banks (NCBs) of the Eurosystem, alongside the ECB, have undertaken to explain their expanding TARGET2 balances since the inception of APP. (See, for example, ECB, Banka d’Italia, Bundesbank, and De Nederlandsche Bank as well as Draghi’s recent letter to MEPs.)

In general, these narratives correctly note that the recent build of “imbalances” should be distinguished from that which occurred during the euro area crisis—then it was banks’ access to ECB liquidity when faced with funding stress that pulled money from the periphery; now it is the push of the APP driving funds abroad (more below).

Moreover, today’s imbalances represent technical factors. Since T2 is a settlement system for the Eurosystem, and since “settlement services are concentrated in some financial centres” this has contributed to the build-up of T2 credits at some NCBs. For example, Draghi’s letter emphasizes how:

Almost 80% of bonds purchased by national central banks under the APP were sold by counterparties that are not resident in the same country as the purchasing national central bank, and roughly half of the purchases were from counterparties located outside the euro area, most of which mainly access the TARGET2 payments system via the Deutsche Bundesbank.

Draghi also notes how some sellers of government bonds to NCBs then

…rebalance their portfolios. [And] As the sellers also make other forms of investment or purchase other securities, including non-domestic securities, additional liquidity flows occur, which contribute to keeping TARGET2 balances elevated.

Or, to put less prosaically, in Germany many APP purchases are from non-euro area holders of Bunds who happen to access T2 system through the Bundesbank—and so, as with Vegas, base money created in Germany stays in Germany. And these are added to by resident sellers of claims on government bonds in the periphery, who then use these funds to purchase securities abroad. Overall, APP proceeds therefore tend to coagulate in Frankfurt, Luxembourg, and the Netherlands.

Even liquidity created by the ECB’s own bond purchases need not travel far, as the Bundesbank emphasizes:

The ECB counterparties’ accounts to which the liquidity is credited are maintained by NCBs. Hence, each purchase of a security by the ECB automatically results in a “cross-border” [comment inserted: or “cross-town”] transaction, thus increasing the ECB’s TARGET2 liabilities.

Notwithstanding the common understanding of the functioning of the T2 system, there remains a difference in tone.

For example, Banka d’Italia (a debtor) emphasizes resident rebalancing of portfolios but claims T2 “developments do not seem to be attributable to a preference for financial assets perceived as safer given the uncertainty surrounding the Italian economy.”

But for De Nederlandsche Bank (a creditor), while T2 “imbalances are no longer an indicator for rising market tensions… they do signal that risk perceptions within the euro area have not normalized either.”

What’s really happening?

It’s easiest to visualize T2 flows through the balance of payments of the major T2 counter-parties—Germany, Italy, and Spain (Figure 3.)

T2 flows are recorded in the balance of payments as other investment assets (credits) or liabilities (debits) in the financial account of each country. We can therefore strip these out and decompose T2 flows as being due to three factors: (i) the current account (plus capital account net of errors and omissions, which are small); as well as private flows of (ii) resident net claims on non-residents; and (iii) liabilities to nonresidents. Three observations:

First, glance back to 2011-12. At the height of the euro area crisis, the increase in T2 liabilities in Italy and Spain was driven by reduced non-resident claims on these economies. It had very little to do with the funding current account deficits, as some scaremongers claimed at the time. If anything, it allowed non-residents to convert a risky claim on the periphery into a less-risky claim on the T2 system—making it more like a form of insurance for the periphery’s creditors.

Moreover, the reduction in financial liabilities in Italy and Spain was met by an increase in financial liabilities in Germany. This is important. The simplistic narrative whereby German current account surpluses had directly funded the periphery in prior years would have presumably seen reductions in peripheral liabilities coincide with a symmetric decrease in German assets abroad. Instead, a decrease in peripheral liabilities translated almost one-for-one into an increase in German liabilities. In other words, third parties converted claims on the periphery into claims on Germany. At best Germany’s funding was indirect, via third parties.

Second, recent developments in the periphery confirm growing T2 liabilities now represent resident accumulation of assets abroad. In other words, purchases of bonds from locals under APP triggers a chain of financial transactions at the end of which residents take a claim on a financial asset abroad. There is a slight difference between Italy and Spain, however—Italy is seeing some non-resident outflows as the counterpart to APP, Spain’s flow of foreign liabilities remains largely unchanged.

Third, Germany’s T2 asset flows are now only partly driven by increasing foreign liabilities. Rather, Germany’s T2 asset accumulation reflects her large current account surplus. Put another way, holding financial flows constant, if Germany ran a smaller current account surplus her T2 asset accumulation would be more moderate.

How can we reconcile the above observations? Let’s first recognize that the bilateral current and financial flows between the countries under focus are relatively small. And all three run current account surpluses, so providing net financing to the rest of the world.

A caricature would run as follows: through APP residents of the periphery are being provided with euro area high powered money with a negative return (the ECB’s deposit rate is currently minus 40bps). They prefer to convert this negative-yielding claim into a higher-yielding (riskier) asset abroad. The euro thus created flows elsewhere to bring down global interest rates, allowing financing to be intermediated towards individuals, sectors, or countries content to spend more than they are currently earning—thus funding current account deficits at the level of other country units.

In turn, this new spending on currently produced goods and services eventually winds up as an export of goods from Germany to some other region of the world. And so, the continued growth of Germany’s T2 claims is a function of the global intermediation of APP funds and Germany’s saving surplus—or spending dearth.

But why should the chain of transactions end there? It need not. Indeed, in Figure 3 private residents of Germany could choose to further recycle this inflow and increase financial claims abroad—rather than through the T2 system. But the APP so alters asset prices and the constellation of interest rates globally that the marginal investor or intermediary—given their existing portfolio and regulatory constraints—no longer sees value in continuing the chain of transactions unleashed by the APP. They would rather sit on an asset yielding minus 40 basis points than take further risk given the constellation of yields they face.

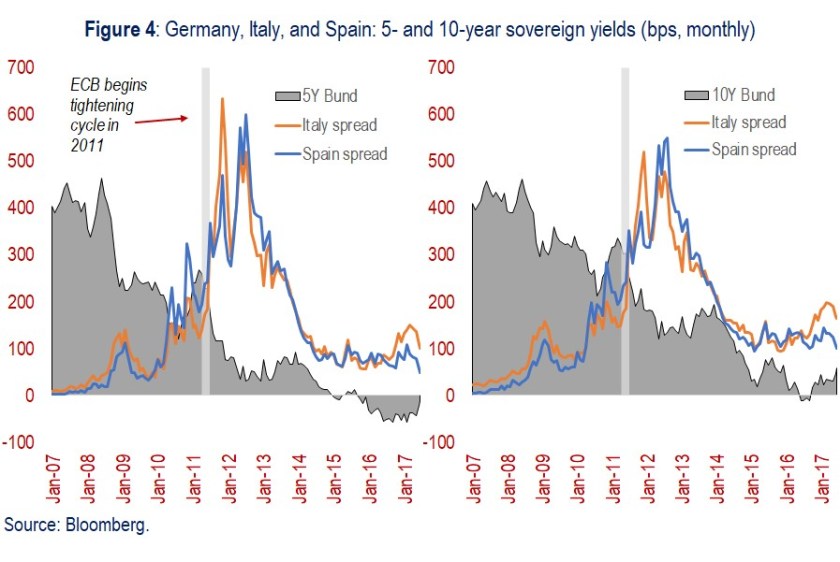

Indeed, Figure 4 shows the 5- and 10-year Bund yield as well as the Italian and Spanish government bond spreads over the Bund at these maturities. Bund yields were pushed to near zero in early 2015 on interest rate reductions and in anticipation by investors of APP. At the same time, Spanish and Italian spreads to Bunds at these maturities were reduced from nearly 300 basis points in 2013 to as low as 100 basis points. Were German investors content to further increase their exposure to the periphery at these spreads, then the T2 balance would have remained contained. Instead, the chain of transactions stops once the relative risk-reward is exhausted.

What happens next?

The above only serves prologue, of course, to the ECB’s future TARGET2 dilemma. As developed-market central banks contemplate “tapering” or the proactive unwinding of post-Crisis balance sheet expansion, consider then the unique circumstances of the euro area.

Lack of risk sharing amongst euro area sovereigns alongside the balance of payments constraint in an incomplete monetary union means any balance sheet reduction takes on a geographical dimension.

Further witness the impact of APP in the periphery, as in Figure 5—the share of government debt held by non-residents and the national central banks of Germany, Italy, and Spain. The total in Germany in Spain is nearly 60 percent, in Italy just shy of 50 percent. For Italy and Spain, the impact of non-resident sales during the euro area crisis is evident. More recently, after inflows re-emerged, Spanish non-resident holding of government debt remains broadly unchanged, meaning APP crowded-out residents—facilitating their accumulation of foreign assets. Italian non-resident holdings have fallen somewhat, but total NCB and non-resident holdings have risen. German non-resident sales met APP purchases nearly one-for-one. These observations are consistent with the balance of payments flows in Figure 3.

Finally, another visualization, in Figure 6, is the consolidated public sector net International Investment Position data of Italy and Spain. The net IIP of the fiscal and monetary authorities combined shows the deteriorating official external balance. It is clear that both consolidated governments are experiencing a continued decline in their external position—despite their economies running current account surpluses. Of course, the resident private sectors in each case are increasing their net financial claims on the rest of the world. But they are at growing risk from external conditions.

What’s important here is that APP purchases in Italy and Spain have resulted in balance of payments outflows through the financial account; they are equivalent to non-resident holdings of government debt when the time comes to unwind APP. As a result, de facto, if and when APP is unwound, it will create a financing requirement in the balance of payments for Italy and Spain. The above compression of yields will be unwound in order to encourage non-residents to increase claims on the periphery and/or residents to repatriate funds.

To be sure, there remains a crucial difference to crisis period. Today, both Italy and Spain generate a current account surplus, so need not rely on net foreign financing to sustain domestic demand. But if domestic demand and inflation were to pick up in, say, Germany, and the ECB felt obliged to normalize rates and reduce its balance sheet, then the above-described financial flows and asset price impacts would go into reverse. Absent risk-sharing, should the 10-year Bund reach 150bps and Italian and Spanish spreads touch 250bps to attract capital inflows—given current primary surpluses in the periphery—a slowdown in growth and concerns about debt sustainability in the periphery could follow. In short, the ECB could provoke a return of the peripheral crisis in pursuit of its mandated price stability market if APP were too rapidly unwound.

It would be better for all if the ECB instead turned a blind eye to inflation for some time. Let Germany run hot, allow her current account surplus to adjust down, facilitating larger surpluses in the periphery (or smaller deficits elsewhere) and so easing the external constraint in southern Europe.

But this is an extremely delicate balancing act—an economic and political one. Whoever replaced Draghi better understand these constraints—otherwise the euro area could once again become a major object of concern for global investors.

Pdf version of this blog: The ECB_s TARGET2 challenge_FINAL

Chart pack: T2 challenge_chartpack

4 thoughts on “The ECB’s TARGET2 challenge”